|

Report type: Weekly Strategy |

“Lifting of ‘quasi-emergency’ measures and the Upper House election; US interest rate hike and the USD-Yen exchange rate”

On 17/3, the government officially decided to lift all Covid-19 related “quasi-emergency” measures currently effective in 18 prefectures by the deadline of 21/3. The Tokyo Metropolitan Government and other local governments are expected to end shortened operating hours and alcoholic beverage restrictions for restaurants in conjunction with the lifting of these restrictions. Furthermore, at the LDP convention on 13/3, Secretary General Motegi stated that the summer Upper House election would be announced on 22/6 and the election would be held on 10/7. PM Kishida is also likely aiming for his administration to promote the early resumption of the “Go To Travel” tourism support program, which was suspended due to the spread of Covid-19, as an achievement for the summer Upper House election. Therefore, going forward, investments in travel, leisure, and restaurant-related businesses should continue to benefit from anticipated sharp recovery in these sectors. Among them, companies that have adopted a contrarian approach by expanding stores while holding down opening costs during the Covid-19 pandemic, or those that have turned their attention to overseas expansion, are the most promising.

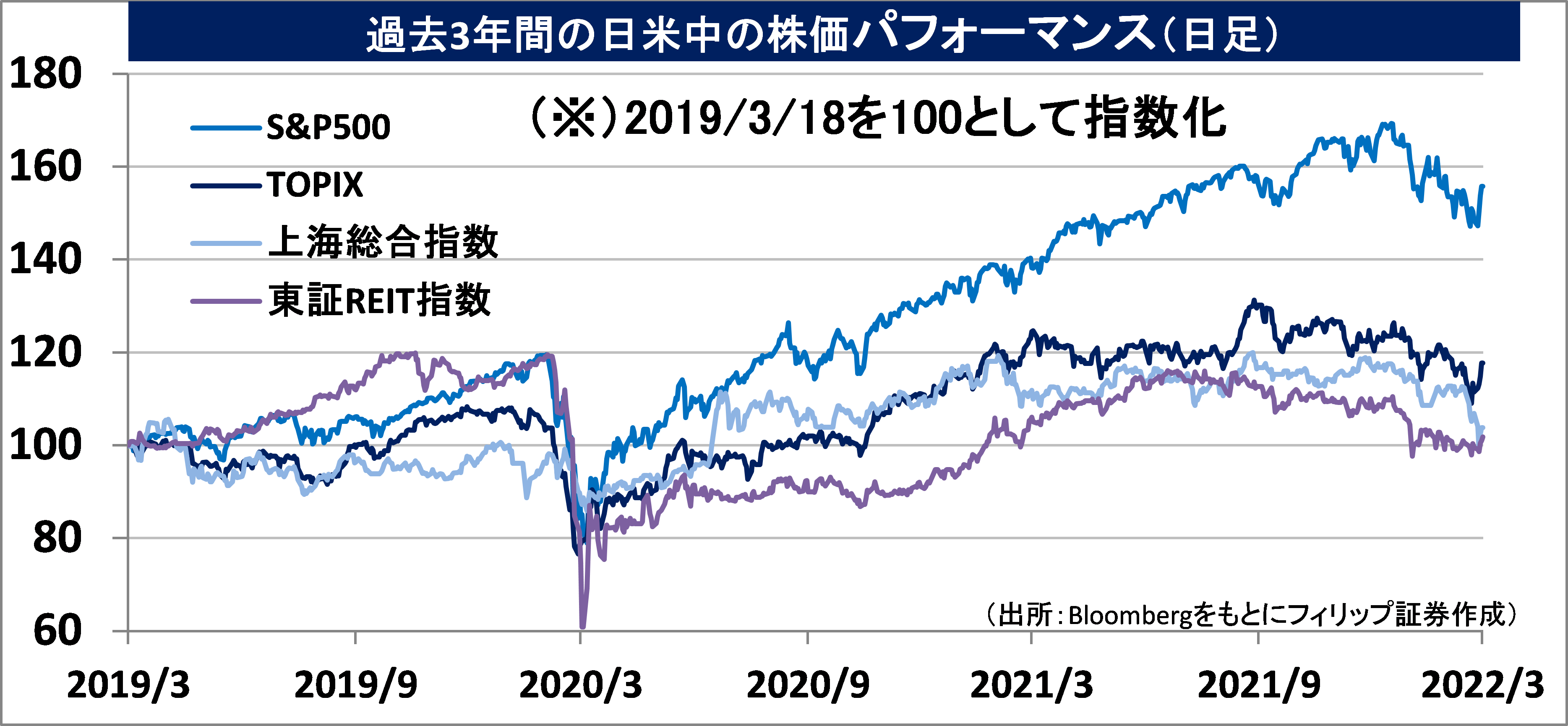

On 16/3 the US FOMC (Federal Open Market Committee) raised the policy rate guidance target by 25 basis points. The participants’ outlook for the policy rate indicated that it will be raised around 11 times by next year, eventually rising to 2.75%. The focus will be on its effect on the USD-Yen exchange rate. During the last interest rate hike, with nine rate hikes in three years from Dec 2015 to Dec 2018, the USD strengthened against the yen to the 125-yen level in June 2015, perhaps because the USD-Yen exchange rate had already factored in the rate hikes. After the USD weakened to below ¥100 in Aug 2016 during the subsequent risk-off phase, it again appreciated to the ¥118 level in Jan 2017 after factoring in the US presidential election and Trump administration tax cuts. Since then, the USD has been slowly weakening against the yen despite intermittent rate hikes since the third hike in Mar 2017.

During the previous 17 US interest rate hikes from July 2004 to June 2006, totaling 4.25 points, the USD-Yen exchange rate went through a full-fledged USD appreciation-Yen depreciation in the latter half of the interest rate hike, unlike the situation in the last rate hike. However, the USD weakened against the yen until the fifth interest rate hike in Jan 2005.

The major difference between this current rate hike and the previous two is that the total balance sheet of the US central bank, the Fed, has expanded to around $9 trillion, with long-term US interest rates being kept artificially low, and the CPI rate of increase has already reached the highest level in 40 years. Nevertheless, as in 2015, the USD is likely to appreciate against the yen, if a hawkish interest rate hike phase has been factored in in advance. However, the reverse could also happen with the USD weakening against the yen if the US economy is shown to be slowing down due to higher interest rates and energy prices.

In the 22/3 issue, we will be covering Koshidaka Holdings (2157), Ise Chemicals (4107), OBIC Business Consultants (4733)and NEC (6701).

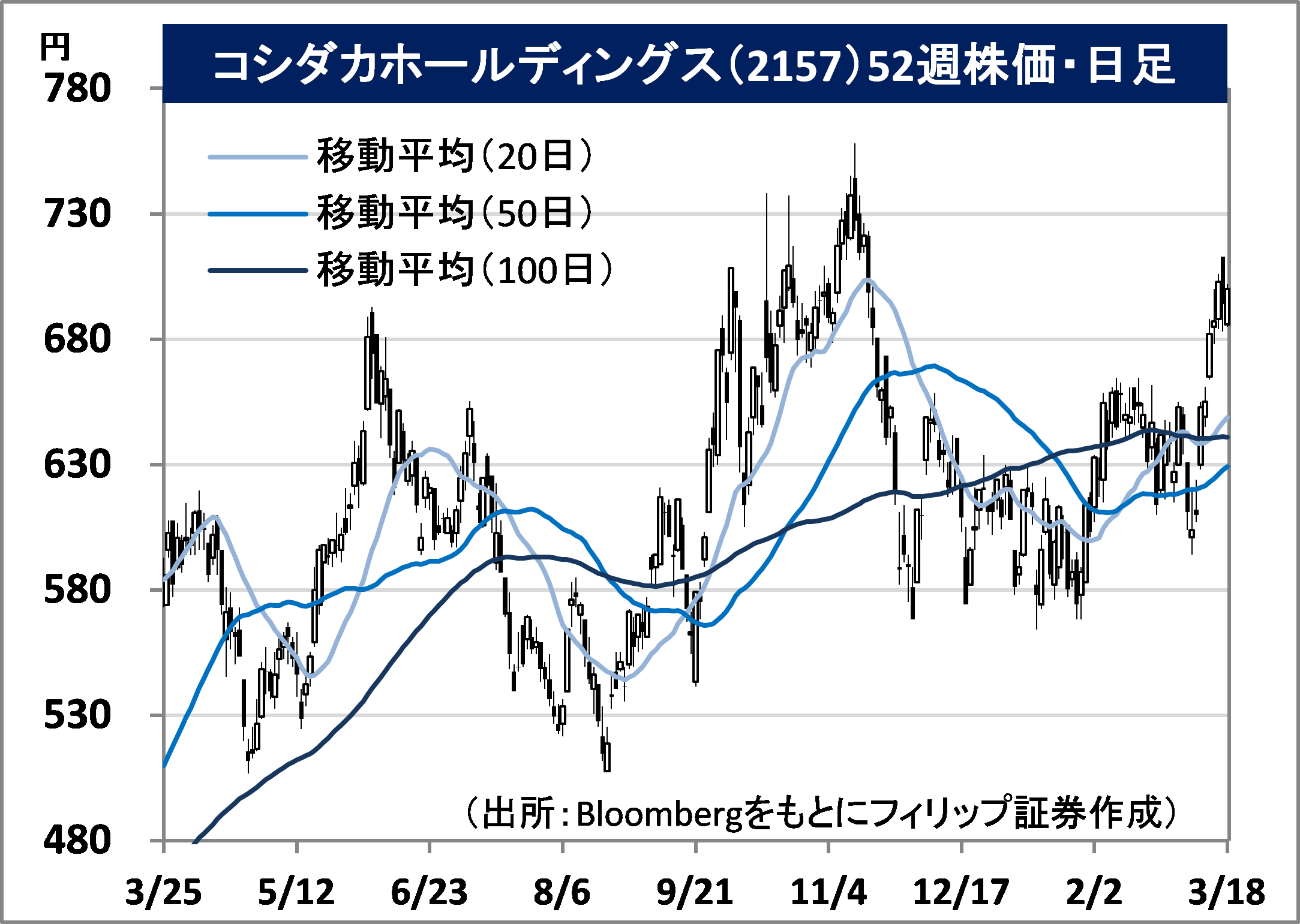

・Founded in 1967 as a Chinese restaurant (Shinseiken) in Maebashi, Gunma Prefecture. Has three main businesses, namely Karaoke Business operating “Karaoke Manekineko” and “One Kara”, Bath House Business operating “Maneki no Yu” and “Rampu no Yu”, and Real Estate Management business.

・For 1Q (Sept-Nov) results of FY2022/8 announced on 13/1, net sales decreased by 2.7% to 6.371 billion yen compared to the same period the previous year, and operating loss increased from minus 983 million yen to minus 1.13 billion yen. The closure of most stores under the state of emergency declared last September had a massive impact. Ordinary income narrowed from minus 795 million yen to minus 196 million yen owing to grants to alleviate shorter operating hours.

・For its full year plan, net sales is expected to increase by 92.8% to 40.093 billion yen compared to the previous year, and operating income is expected to return to the black from minus 7.628 billion yen in the previous year to 2.701 billion yen. The government has decided to lift Covid-19 related quasi-emergency measures in all regions by the deadline of 21/3. Expanding stores with a distinctive business model, including the acquisition of the karaoke business (43 stores) of izakaya (Japanese-style bar) giant Daisho in March last year and subsequently using the low-cost, fully-furnished properties. Aggressively pursuing overseas expansion including Asean countries and Korea.

・Founded in 1927 in Ise City, Mie Prefecture. A consolidated subsidiary of AGC (5201) that manufactures and sells iodine and natural gas, as well as metal compounds (cobalt, nickel, etc for rechargeable batteries). One of the top iodine producers both in Japan and in the world.

・For FY2021/12 results announced on 3/2, net sales increased by 20.7% to 20.354 billion yen compared to the previous year, and operating income increased by 24.0% to 2.709 billion yen. In the iodine and natural gas business, the international market for iodine had remained firm and product sales volume had recovered. The metal compounds business had benefited from higher nickel chloride sales volume as well as rising metal market prices.

・For FY2022/12 plan, net sales is expected to increase by 3.2% to 210.0 billion yen compared to the previous year, and operating income to decrease by 11.4% to 2.4 billion yen. Includes assumption of higher depreciation costs due to new well development as well as maintenance and renewal investments, and higher raw fuel and material prices. Japan and Chile account for more than 90% of the world’s iodine production, with Japan accounting for about 30%. In addition, stable iodine in non-radioactive drugs is believed to have a prophylactic effect against radiation exposure, and is likely to attract more attention if geopolitical risks increase

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: