Report type: Weekly Strategy

“Leaps in the Year of the Rabbit” From Long-Term Interest Rates to Japanese Stocks ~ The Undervalued Nikkei Average

Happy New Year! The stock market proverb associated with the Chinese zodiac states that the year of the “dragon is the ceiling, the horse’s tail drops (declines), the sheep endures (plateaus and adjusts), the monkey makes a ruckus (large fluctuations), the dog smiles (increases), the pig huddles together (small range fluctuations), the rat prospers (increases), the ox stumbles (adjustments), the tiger moves swiftly (large increases) and the rabbit leaps (big jumps)”. At least, based on the prediction towards revised monetary easing by the Bank of Japan, “leaps in the long-term interest rate” have begun incorporating in the market as well. In contrast to signs of a recession indicated by the “inverse yield curve” where the long-term interest rates fall below the short-term in major markets in Europe and the U.S., an increase in the “normal yield curve”, where the long-term exceeds the short-term, mostly benefits the economy due to a vitalization of fund management and capital investment from financing in low interest rates and the yield which exceeds it. It looks like there may be a possibility of “leaps” in the Japanese stock market which contrasts with Europe and the U.S. In fact, several major ASEAN nations that have eased or abolished cross-border movement half a year earlier than Japan have had a positive annual percentage change in last year’s main stock indices. In China as well, Hong Kong’s Hang Seng Index had a sharp rise of approx. 44% from end October last year to the closing price on the 5th, indicating a contrasting aspect between Asia versus Europe and the U.S.

On the other hand, it has relieved the position of following the U.S. stock market on the premise of large-scale monetary easing by the Bank of Japan Governor Kuroda and the longstanding “Abenomics” economic policy, and it appears that there may be accompanying adjustments in price or time involving the switch in direction from taking the increase in the long and short-term normal yield curve as an investment opportunity. In fact, the Nikkei average has become prominently undervalued as seen from corporate performance, such as its closing price on the 5th where the P/E ratio (price-earnings ratio) based on a weighted average via market capitalization, etc. was 12.02 times and the P/B ratio (price-to-book ratio) was 1.09 times, which matches last year’s lowest level. In the supply and demand aspect as well, technical indicators, such as the up/down ratio, short selling ratio and 14-day moving average RSI (relative strength index), have fallen to the most oversold levels since last year. Perhaps we could view this to be the arrival of the year’s first investment opportunity.

On the 4th, Prime Minister Kishida touched on the possibility of the number of births in 2022 falling below 800,000 for the first time and brought up “countermeasures for the unprecedented declining birthrate” as a priority issue for this year. It 3 main pillars are ① reinforcing economic support, such as child allowance, ② reinforcing support, such as after-school childcare and sick childcare, and ③ reinforcing the childcare leave system, etc. Together with the policy laid out by Koike, the Governor of Tokyo, on paying out 5,000 yen a month to children until they are 18 years old without setting income limitations, towards the inauguration of the “Children and Families Agency” in April this year, we can expect a lookout for stocks related to childcare.

With travel recovering worldwide and China also in the process of lifting measures involving their COVID-19 regulations, it has shed light on the aircraft shortage. There have been movements of major global aviation companies placing aircraft orders in several hundred units with the American Boeing and the European Airbus, and an acceleration in the increase of order backlog. Aircraft component manufacturers in particular are expected to reap mid and long-term benefits.

In the 10/1 issue, we will be covering JP-Holdings (2749), Digital Media Professionals (3652), Nikkiso (6376) and Hitachi Zosen (7004).

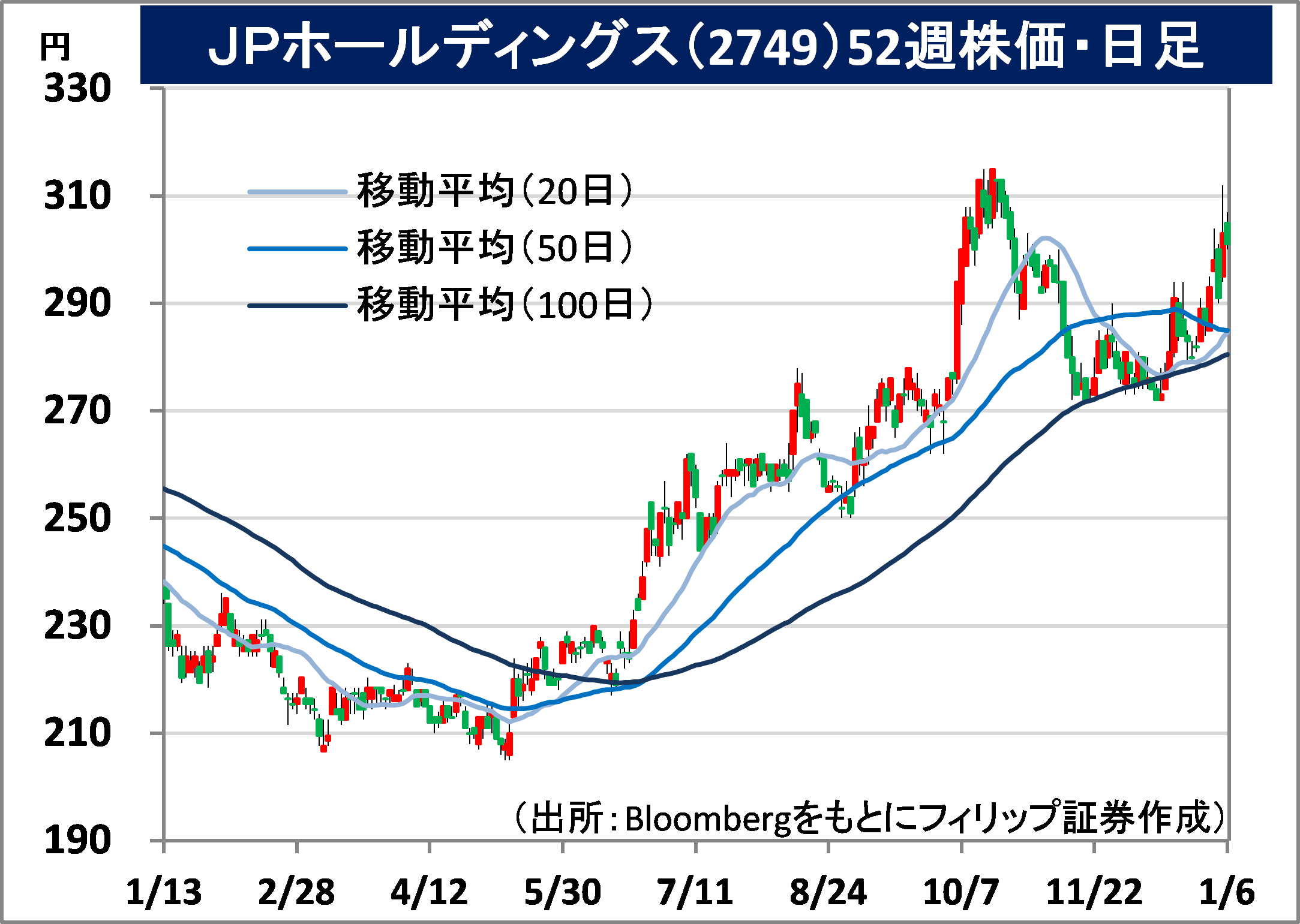

JP-Holdings, Inc. (2749) 301 yen (6/1 closing price)

・Established in Nagoya City in 1993. Conducts a childcare support business that operates childcare centres, after-school day care, children’s centres and private after-school day care approved and authorised by municipalities. Their top shareholder is Gakken Holdings (9470) which owns 30%.

・For 1H (Apr-Sep) results of FY2022/3 announced on 10/11, net sales increased by 2.3% to 17.207 billion yen compared to the same period the previous year and operating income increased by 37.2% to 1.502 billion yen. For new establishments, there were 2 childcare centres and 12 after-school day care and children’s centres, and total childcare support facilities as of end September was 308 which increased by 5 facilities compared to end March. Selling, general and administrative ratio improved by 1.2 points compared to the same period the previous year.

・Company revised its full year plan upwards. Although net sales is expected to increase by 3.7% to 35.64 billion yen compared to the previous year and annual dividend to remain unchanged to have a 1.50 yen dividend increase to 6.00 yen, operating income is to increase by 8.6% to 3.633 billion yen (original plan 3.56 billion yen). In addition to personnel reallocation, revisions to operations and their ordering system are also expected to contribute to an improved profit margin. On the 4th, Prime Minister Kishida announced “countermeasures for the unprecedented declining birthrate” in addition to Governor Koike’s announcement of a countermeasure unique to Tokyo. They are expected to benefit its business performance.

Digital Media Professionals Inc. (3652) 2,584 yen (6/1 closing price) *TSE Growth Stock

・Established in 2002. Conducts the manufacturing and retail of LSI products in addition to providing semiconductor and end-product manufacturers semiconductor IP cores incorporated with gaming devices, automobile and mobile communication devices, etc. by developing graphics IP cores.

・For 1H (Apr-Sep) results of FY2023/3 announced on 10/11, net sales increased by 34.0% to 925 million yen compared to the same period the previous year and operating income saw a reduction in the range of deficit from (109) million yen the same period the previous year to (102) million yen. For net sales by field, although there was a 71% decrease to 31 million yen in robotics, there was growth in safe driving support which increased by 9% to 49 million yen and in amusement which increased by 58% to 789 million yen.

・For its full year plan, net sales is expected to increase by 42.1% to 2.37 billion yen compared to the previous year and operating income to return to profit from (126) million yen the same period the previous year to 25 million yen. Continued mass production shipments are predicted in amusement for the next-gen image processing semiconductor “RS1”. Retail units of gaming machines equipped with an image processing process which was joint developed by Bandai Namco Sevens exceeded 100,000 units in December. Benefits can be expected from the Smart Pachislot which had its ban lifted in November and the Smart Pachinko which has its ban scheduled to be lifted in March.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: