|

Report type: Weekly Strategy |

■Japanese Stocks, the US Market and the Chinese Economy – Future Japanese Stock Focus

On 5/5, PM Kishida stated in the City of London financial center that “in June, we will ease restrictions on immigration to the same level as other developed countries”, and he also pledged 150 trillion yen in new investments related to decarbonization through public-private partnership over the next 10 years. The Japanese stock market was expected to respond favorably to these announcements, along with the continuing net buying of Japanese stocks by foreign investors since April. However, the Nikkei Average was dragged down by the US market and the Chinese economy, and trended lower during the week from the 9/5 to 12/5. Blue-chip high-tech stocks with high index contributions have been affected by the US market, while economically-sensitive stocks and China-dependent stocks appear to be under downward pressure from the Chinese economy.

Since the Federal Open Market Committee (FOMC) meeting on 3-4/5, the US stock market failed to halt the market decline as, although the average hourly wage in the April employment report released on 6/5, the consumer price index for April released on 11/5, and the wholesale price index for April released on 12/5 all showed signs of slowing growth, they were still higher than market expectations. On the other hand, the Chinese economy showed a sharp slowdown in export growth in the April trade statistics released on 9/5, indicating the significant impact of the Chinese government’s “zero-Covid” regulations.

In spite of this, the Nikkei Average rebounded sharply on 13/5 on the back of buybacks as, regarding the Chinese economy, companies are increasingly confident about the prospects for demand recovery after the lifting of restrictions related to Covid-19, and the market is beginning to see that concerns about prolonged inflation and tighter monetary policy in the US are facilitating a shift of funds from US stocks to Japanese stocks, backed by aggressive monetary easing by the BOJ.

The first priority for Japanese equities going forward will be “energy” related, with infrastructure development for the spread of renewable energy, the restart of nuclear power plants, and liquefied natural gas (LNG) plant-related projects. Secondly, food manufacturers will likely benefit from price hikes, as the BOJ also noted in its April “Outlook for Economic Activity and Prices” released on 2/5 that food prices tend to accelerate once price hikes begin. Sushiro, a conveyor-belt sushi restaurant, announced that it will raise the price of some of its menu items by 10-30 yen starting in October, and Calbee (2229) announced that it will raise the price of “Kappa Ebisen” and other products starting in June. Thirdly, spotlight will be on companies that are quick to respond to “revenge consumption” related to travel and leisure activities that had been severely curtailed till now, or on those companies that are quick to respond to structural changes in consumption and lifestyles brought about by the Covid-19 pandemic.

Recently, as in the case of Japan Steel Works (5631), there have been incidents where the market has overreacted to bad news, resulting in extreme short-term overselling. Other stocks worth picking up carefully include over-sold stocks with credit multiples below 1.0x due to the continued decline in stock prices despite their being undervalued.

In the 16/5 issue, we will be covering Kitoku Shinryo (2700), NGK Insulators (5333), Yokogawa Electric (6841) and AOKI Holdings (8214).

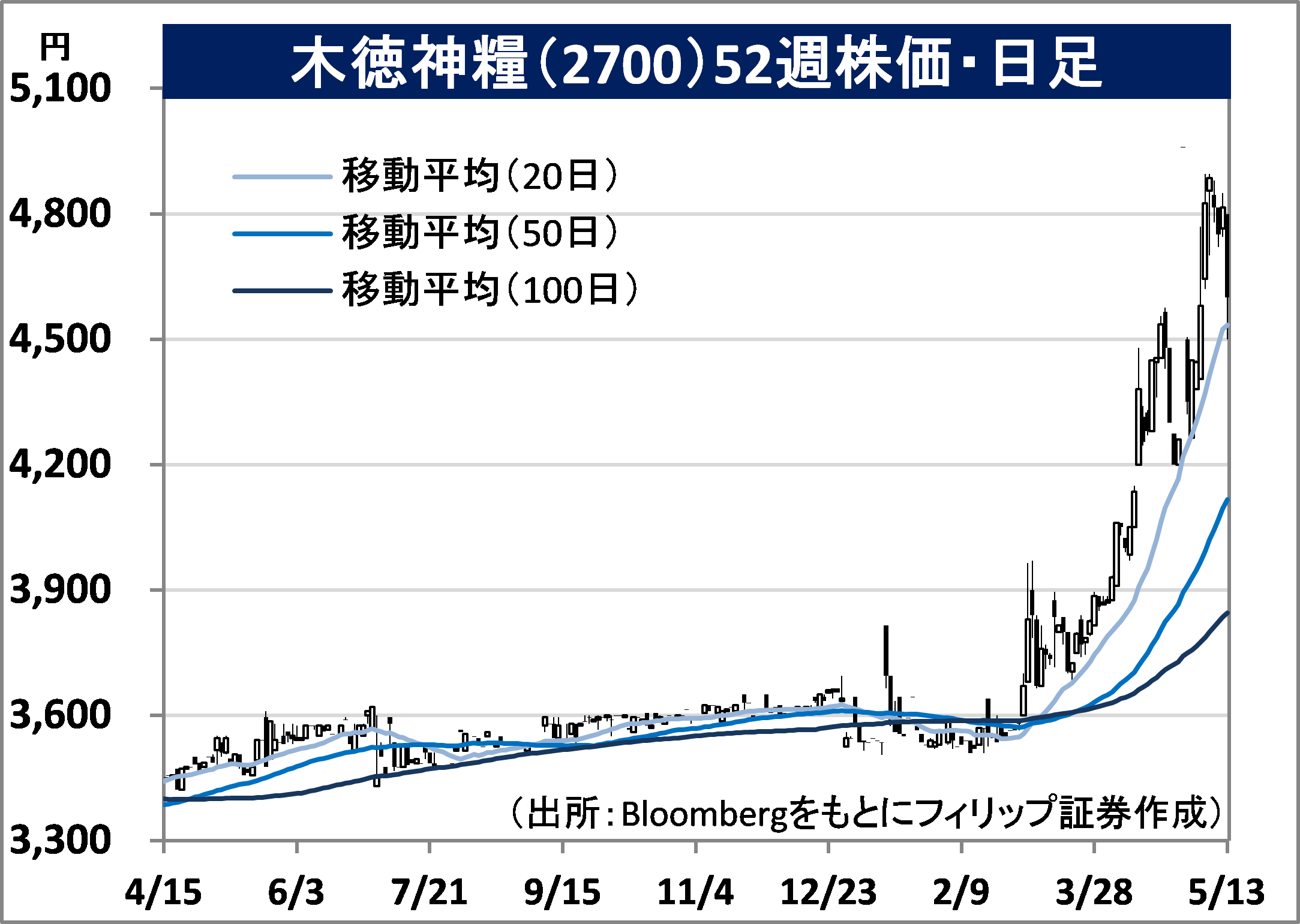

Kitoku Shinryo Co., Ltd (2700) 4,600 yen (13/5 closing price)

・Opened in 1882 in Kabuto-cho, Nihonbashi, as Kimura Tokubei Shoten, a rice dealer. Operates four businesses, namely, rice business, which makes and sells milled rice and brown rice, feed business, egg business, and food business, which manufactures and sells rice flour, processed foods, and other products.

・For 1Q (Jan-Mar) results of FY2022/12 announced on 12/5, net sales decreased by 4.0% to 26.092 billion yen compared to the same period the previous year, and operating income increased by 90.1% to 450 million yen. In the rice business, in addition to a decline in domestic rice transaction prices, demand from restaurants remained sluggish and sales at mass retailers for home use were weak. Improvements in inventory and purchasing as well as reductions in SG&A expenses contributed to profits.

・Company has revised its full year plan upwards. Net sales is expected to decrease by 4.5% to 103.0 billion yen (original plan 97.5.0 billion yen) compared to the previous period, operating income to increase by 90.0% to 1.0 billion yen (original plan 480 million yen), and annual dividend to increase by 10 yen to 60 yen (original plan 50 yen). In addition to the contribution to sales from higher unit sales prices of minimum access rice (the minimum amount of foreign rice that should be imported) and other products due to the weak yen, purchasing in response to the supply-demand environment and the establishment of multiple purchasing routes are expected to continue to contribute to profits.

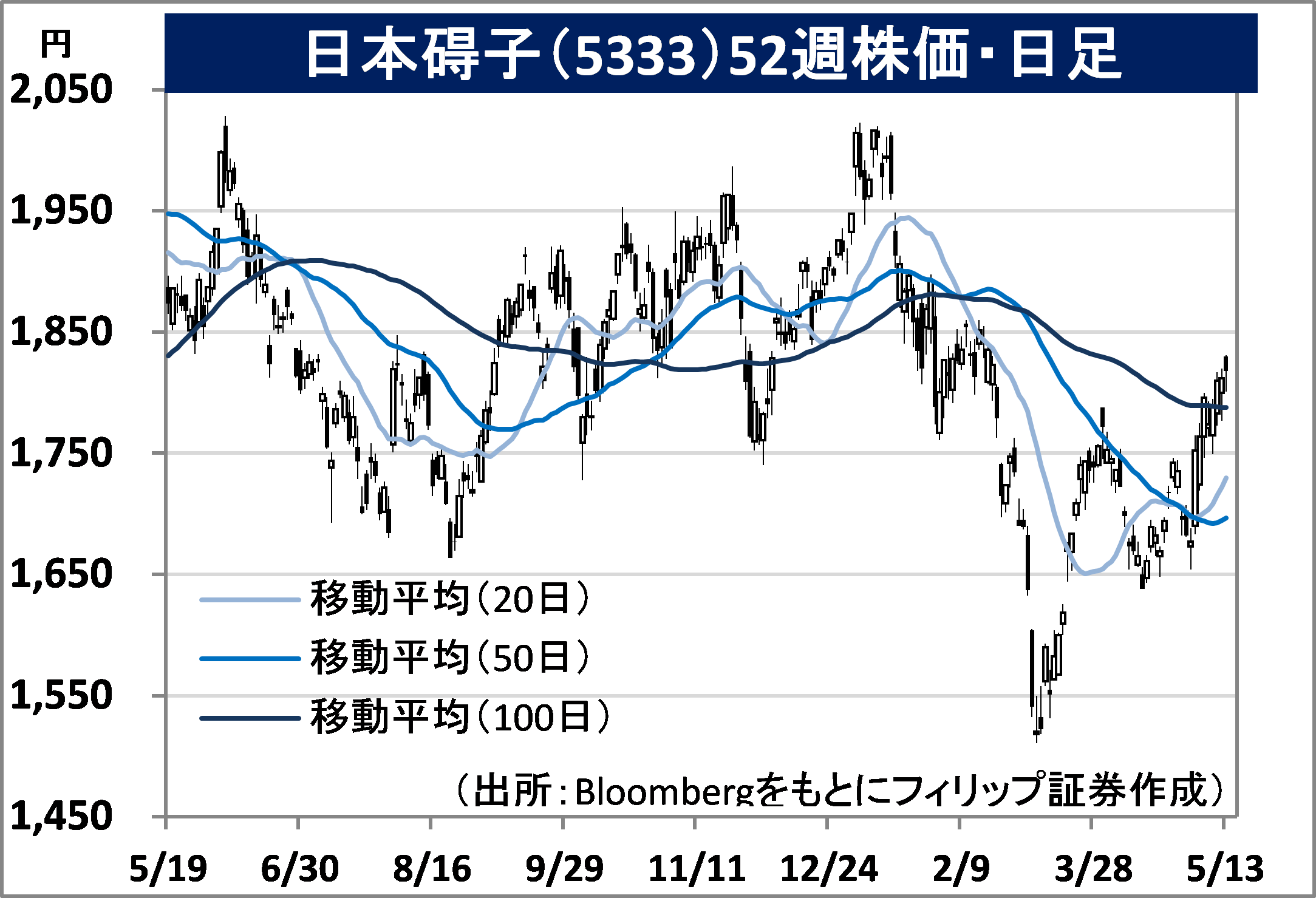

NGK Insulators, Ltd (5333) 1,818 yen (13/5 closing price)

・The insulator division was spun off from what is now Noritake Co., Ltd (5331) in 1919. Top player in the world for insulators. Operates four businesses, namely, Energy Infrastructure, Ceramic Products, Electronics, and Process Technology.

・For FY2022/3 results announced on 28/4, net sales increased by 12.9% to 510.4 billion yen compared to the previous year, and operating income increased by 64.3% to 83.5 billion yen. Although sales in the Energy Infrastructure business, which handles insulators and NAS batteries, declined 3.2% YoY, sales in the Process Technology business, which is related to semiconductor production equipment, and the Ceramics Products business were solid, rising 16% YoY, and 18% YoY respectively.

・For FY2023/3 plan, net sales is expected to increase by 13.6% to 580.0 billion yen compared to the previous year, operating income to increase by 7.7% to 90.0 billion yen, and annual dividend to increase by 3 yen to 66 yen. Company’s NAS battery developed through its R&D using sodium (Na) and sulfur (S) is an electric power storage system with large capacity, high energy density and long life. It is likely to increase in importance as an electric power infrastructure to equalize the daily supply-demand of solar power generation as part of the government’s goal of promoting renewable energy.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: