Report type: Weekly Strategy

“Is This the First Time to Wait for the Japanese Economy Since the Collapse of the Heisei Bubble?”

The Nikkei average marked 29,650 points right after opening on 12/2, renewing its high since early August 1990. How should investors or consumers react to this news? It seems that there are also views that this is merely a product of excessive liquidity that deviates from the real economy where expectations have been overly weaved into the market on the normalisation of economic activities after the widespread popularisation of vaccine inoculations, and instead, to be wary about a significant fall after the bubble bursts. However, as the saying goes, “to analyse the stock market itself rather than looking to elsewhere”, as investors confronting the stock market, perhaps there is a need for an attitude that pays homage to foresight on stock prices and an attempt to analyse the world that is to come.

Based on this viewpoint, the Japanese economy is presented with the hypothesis that it is facing a situation it has never experienced since the collapse of the Heisei bubble. In the years around 2001-07 where there was an overlap of a continuous decline in the U.S. Dollar Index, a sharp rise in commodity prices, such as crude oil, and emerging markets thriving, such as China, although there was an overheating of the economy and a rise in interest rates in terms of the global economy’s economic cycle, under the Koizumi and Takenaka structural reform, along with an acceleration in globalisation centred on regulatory easing, in the Japanese economy, there was a continuous decline in prices and wages. As also seen from the interest rates, such the 10-year government bonds changing towards a continuous decline after rising to peak at around the 1.9% level in July 2007, it appeared as if the situation involving the rise in prices and interest rates following an overheating of the economy in the 2000s did not present itself in Japan like how it did in various other countries. It was common sense that prices and interest rates did not rise, and it is thought that that came to be the major factor for the growing trend in the same situation persisting in the future.

Also, for mortgage loan interest rates, although previously there was a tendency to consider the change to fixed interest

rates for mortgage loans due to concerns on the rise in interest rates resulting from future inflation, with the prolongment in zero interest rates and negative interest rates, it appears that there is an inclination towards prioritising the alleviation of burden involving immediate interest rate payments due to floating interest rates. From the perspective of consumers, perhaps it may not necessarily be wrong to take the current rise in stock prices to be a warning that there will be a great change in the logical perspective regarding these kinds of interest rates and prices.

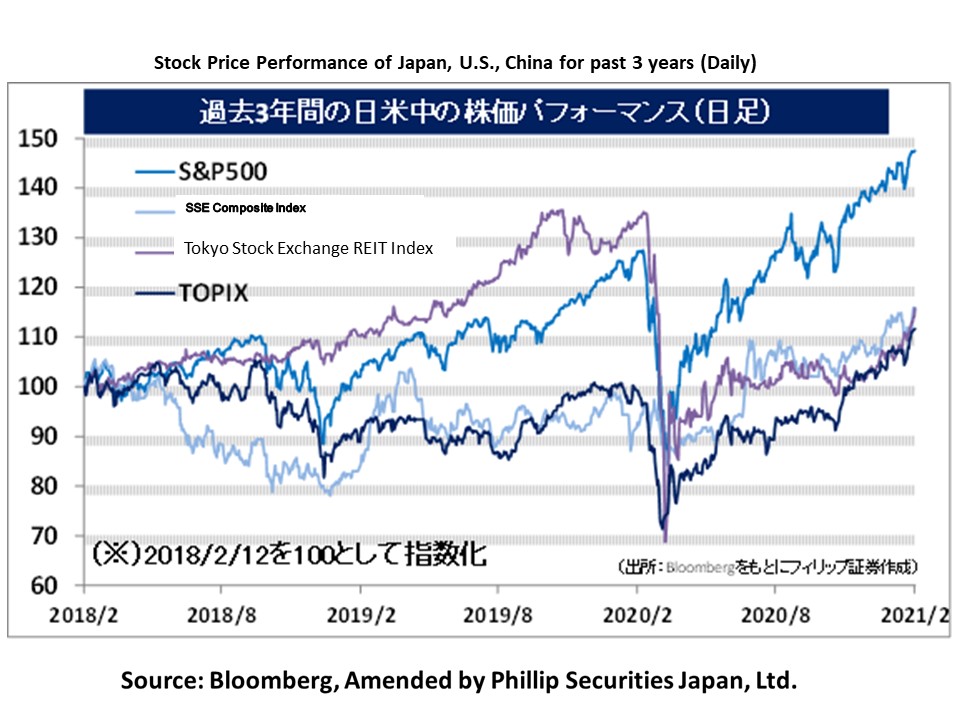

As seen from the “Comparison with Rises in the Stock Market in the Past” on Page 2, the rise in stock prices since 19/3 last year has reached a speed of approx. 2.5 times the rate of increase between October 1987 to the end of 1989. On the other hand, the speed of the rise from before the U.S. presidential election in November last year up to the present is slower than the rise in the period from before the dissolution of Japan’s House of Representatives in November 2012 up to the inauguration of the 2nd Abe administration and the Bank of Japan’s Governor Kuroda’s unprecedented monetary easing. We recall that it was a year where buying the dips and the adjustment in February due to the season did not apply.

In the 15/2 issue, we will be covering DeNA (2432), TOWA (6315), Mitsubishi Heavy Industries (7011), and Kintetsu World Express (9375).

・Established in March 1999. Provides internet services for mobile and PC. Expands 5 business segments, which are the game business, sports business, live streaming business, healthcare business and new/other businesses.

・For 9M (Apr to Dec) results of FY2021/3 announced on 9/2, sales revenue increased by 12.9% to 102.924 billion yen compared to the same period the previous year and operating income returned to profit from (44.161) billion yen the same period the previous year to 25.32 billion yen. For segment profits, although the sports business fell into deficit, their mainstay game business increased by 63.5% and the live streaming business returned to profit.

・Their full year forecast is undisclosed due to difficulties in reasonably calculating figures. For the game business, those related to “Slam Dunk”, where its copyrights are owned by Toei Animation (4816), contributed to earnings due to a popularisation in Korea and Greater China. A new and well-known title is also planned for release soon in 2021. Following the game business, where both its sales and profits benefitted from consumption from staying at home, in the live streaming business, which has become their pillar, we can expect new expansion, such as into live commerce, etc.

・Established in 1979. Expands 3 businesses, which are the “semiconductor equipment business”, which handles semiconductor equipment and precision metal moulds for manufacturing semiconductors, the “moulded fine plastic products business” such as medical equipment, and the “laser processed devices business”.

・For 9M (Apr-Dec) results of FY2021/3 announced on 5/2, net sales increased by 10.2% to 20.715 billion yen compared to the same period the previous year and operating income increased by 12.0 times to 2.327 billion yen. China, which is promoting next-gen infrastructure investment and in-house semiconductor production, and Taiwan, which is continuing proactive investment by benefitting from the rise in demand for a wide range of products, have contributed to the increase in income and profit in their mainstay semiconductor equipment business.

・Company revised their full year plan upwards. Net sales is expected to increase by 14.8% to 29 billion yen compared to the previous year (original plan 26.77 billion yen) and operating income to increase by 4.1 times to 3.3 billion yen (original plan 2.31 billion yen). There is a predicted increase in production capability in respective semiconductor manufacturers and an increase in sales for high value-added products, such as those related to 5G. Also, regarding the “post-process” of semiconductors, which is the main area of competition for the company’s products, it was reported that the Taiwanese TSMC, the world’s top in receiving production consignments, will set up a development base in Japan with an investment sum of 20 billion yen.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: