Report type: Weekly Strategy

“Is the Materials Sector the Main Player in the Post “Pro-Buyback” Market?

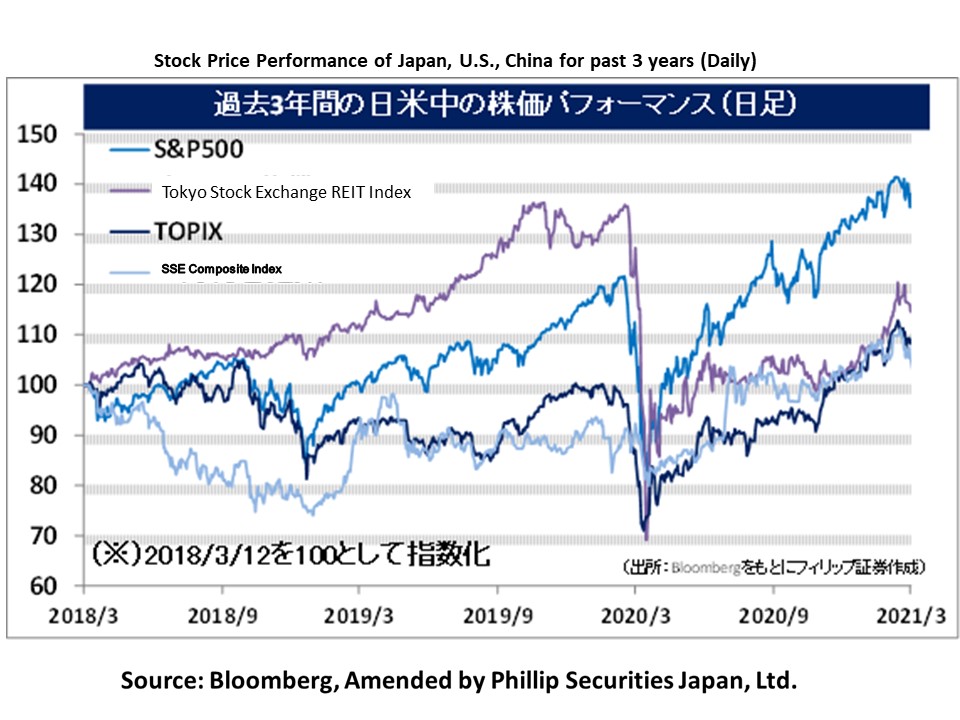

At the spot positions based on 5/3 of the Nikkei average’s spot and futures arbitrage transactions, the excessive state of the unsettled selling balance (forward buying and spot selling) was resolved by a significant increase in the unsettled buying balance (forward selling and spot buying). The excess unsettled selling balance was last resolved about 1 year and 2 months ago in the last week of December 2019. Originally, with the unsettled buying balance exceeding the unsettled selling balance forming the usual structure of the Japanese stock market, due to a rise in concerns on a worsening of the U.S.-China trade and economic friction between September to December 2019 and concerns on the impact of the spread of COVID-19 from January 2020 onwards, a selling lead where the total unsettled selling balance exceeding the total unsettled buying balance had dominated the Japanese stock market. In addition, with concerns in the lead followed by expectations and hopes towards an improvement in the situation, we can perceive that the rise in the stock market was due to an encouragement of buybacks of short positions.

What will be the force that drives an increase in the stock market after the pro-buyback bull market? With the conclusion of an additional large-scale economic measure bill of about 1.9 trillion dollars by the Biden administration in the U.S. on 11/3, concerns of an increase in interest rates and prices along with economic expansion and the increasing shift worldwide from high P/E ratio growth stocks to economic cycle value stocks, there has been a growing sense of the stock market peaking on the whole. In contrast, there have been indications of a stance in absorbing the negative impact following the increase in U.S. government spending, such as the ECB (European Central Board) deciding to speed up the pace of bond purchases under the Pandemic Emergency Purchase Program (PEPP) in order to put a stop to the increase in Euro government bonds. There is attention on whether the Bank of Japan will also follow the ECB at the Bank of Japan’s Monetary Policy Meeting scheduled for 18-19/3.

Under a state of a dollar depreciation, in the period where a prominent “emerging country shift” and “commodity shift” were observed in the years between 2000-07, even in the TOPIX 33 Sector Indices, “Iron and Steel” and “Marine Transportation” had better performance than others. In the U.S. S&P 500 Industrials Sector Index as well, “Materials” in addition to “Energy” and “Financials” are performing strongly. Those leading “Materials” are the copper and molybdenum production giant Freeport-McMoRan (FCX), the world’s largest gold mining company Newmont (NEM), the steel manufacturer Nucor (NUE) and the chemicals giant Dow Inc (DOW). Perhaps there is room to also look out for Japanese corporations competing worldwide with them, such as Sumitomo Metal Mining (5713), Nippon Steel (5401), Sumitomo Chemical (4005) and Mitsubishi Chemical Holdings (4188), etc. Also, in the Corporate Goods Price Index released by the Bank of Japan on 11/3, there is attention on the 16.5% increase in metals and copper products and the 4.2% increase in chemical products compared to the same month year-over-year, which exceed other industries.

In the 15/3 issue, we will be covering ITOCHU Advance Logistics Investment Corporation (3493), Iseki & Co. (6310), ASICS (7936), and Nippon Television Holdings (9404).

・Established in 5/2018. Company is a logistics facility REIT sponsored by ITOCHU (8001) with strengths in businesses related to lifestyle consumption that have high affinity with logistics. Their flagship property is “i Missions Park Inzai” in Chiba Prefecture.

・For FY2020/7 (Feb-Jul) results announced on 14/9, operating revenue increased by 36.4% to 2.399 billion yen compared to the previous period (FY2020/1), operating income increased by 42.2% to 1.193 billion yen and distribution per unit increased by 1.3% to 2,425 yen. Due to benefits from an expansion in e-commerce and their cooperation with ITOCHU Group, occupancy rate of overall assets owned at the end of the period hit 99.9%.

・For its FY2021/1 plan, operating revenue is expected to increase by 2.4% to 2.456 billion yen compared to the previous period (FY2020/7), operating income to decrease by 0.2% to 1.19 billion yen and distribution per share to increase by 3.6% to 2,508 yen. Company forecasted dividend yield up to FY2021/7 at the closing price on 11/3 is 3.89% and NAV (net asset value) ratio is 1.07 times. For logistics facilities, due to relatively highly stable earnings from the conclusion of long-term fixed rental fee contracts with tenants, the dips could be an opportunity.

・Company is a manufacturer specialising in agricultural machinery which established in 1926. Their main business content involves the development, manufacture and retail of agricultural machines related to rice and vegetable farming, etc, and comprises the “development and manufacturing division”, “retail division” and “others division”. Company is 3rd in Japan for agricultural machines.

・For FY2020/12 results announced on 15/2, net sales decreased by 0.4% to 149.304 billion yen compared to the same period previous year and operating income decreased by 24.1% to 2.084 billion yen. Due to the record of the provision for doubtful receivables, an evaluation loss involving affiliated company stocks and impairment losses involving assets for domestic businesses and domestically-owned real estate, net income fell into deficit from 723 million yen the previous year to (5.641) billion yen.

・For its FY2021/12 plan, net sales is expected to increase by 2.8% to 153.5 billion yen compared to the previous year and operating income to increase by 72.7% to 3.6 billion yen. Under structural changes in the agriculture industry that make it difficult to secure a foreign workforce worldwide following restrictions in movement, it is predicted that components and repair revenue along with large-scale machines and smart agricultural machines, etc. will perform strongly. Also, the record of the large sum of impairment loss last year is likely to be regarded positively in the aspects for improving the balance sheet, such as the depreciation of fixed assets and inventory reduction, etc.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: