Report type: Weekly Strategy

“Is the Inauguration of the New President a Watershed for ‘Expectations’ and ‘Reality’?”

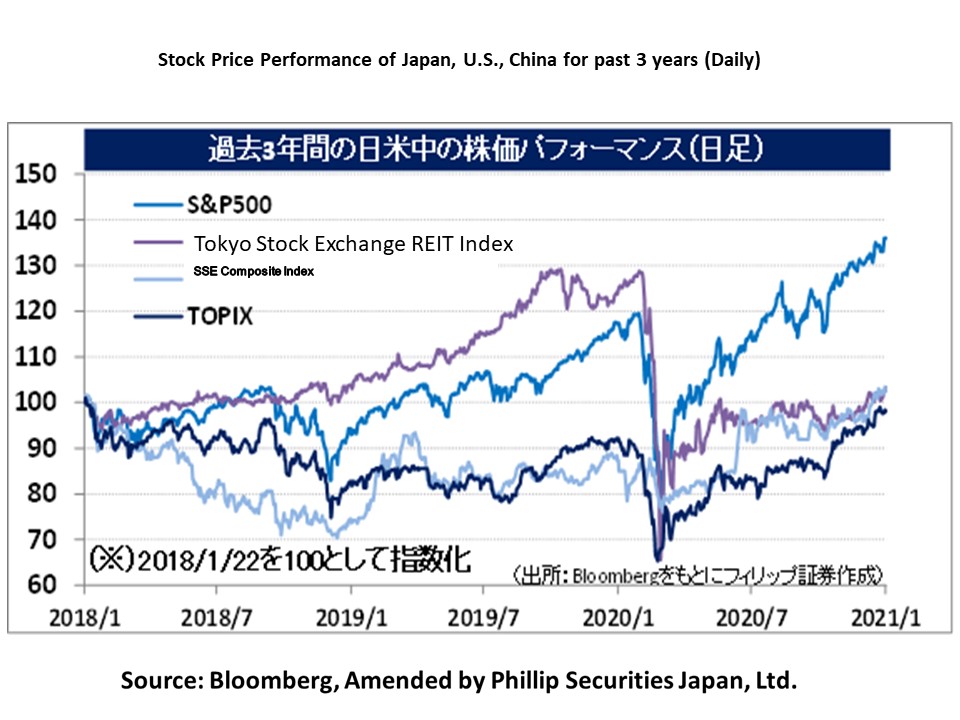

On 20/1, Biden from the Democratic Party was safely and officially inaugurated as the 46th President of the United States. Alas, this will be the start of a new era under the “blue wave”, where the White House, Senate and House of Representatives are governed by the Democratic Party. As a result of the stabilisation of the U.S. dollar from reinforced monetary easing by the FRB under the policy that prioritises international cooperation, it is thought that there will be a major change in the flow of global money from an appreciation of the U.S. dollar and an overconcentration in major U.S. high-tech corporations following an influx to the U.S. due to the previous Trump administration’s “America First” towards an influx of investment funds to emerging countries and countries rich in resources. There has already been a rise in commodity prices, such as silver, which is used in photovoltaic panels, since some time last summer when it was said that Biden was leading Trump in a public opinion poll. Also, from last fall onwards, there was a rise in the price of nonferrous metals, such as copper, nickel and aluminium, etc. as a result of developed nations coming up with ambitious policies one after another to reduce greenhouse gas emissions as a focus on the policy to promote electric cars (EV). In the stock market as well, trends of honouring environmental-related stocks, such as hydrogen and EV, etc., as “Bidenomics stocks”, saw an increase in activity along with expectations of the Biden administration.

On 21/1 when the inauguration of U.S. President Biden ended, the media completely changed from a welcoming mood from the expectations thus far and began debating on the tough reality in U.S. politics and society. For example, in “Deep Insight” on Page 7 of The Nikkei’s morning edition, the company’s commentator’s opinion in the heading, “The ‘Semi Civil War’ in the U.S. Threatens the World” was placed side by side with Ian Bremmer’s opinion in the heading, “The Beginning of the ‘President With Remarks’ Era”, etc. Even if there is no change to the mid and long-term policies on the reduction of greenhouse gas emissions, currently, we are beginning to see an emergence of a situation where there is concern on the sustainability of the businesses of new power companies which do not have their own power source, such as from the violent fluctuation of spot prices within a high price range in the Japan Electric Power Exchange (JEPX), against the backdrop of an insufficiency of liquefied natural gases (LNG) in the power market, etc. Perhaps it has begun to shift towards a state where there is a balance of expectations and reality regarding the stock prices of environmental-related stocks.

However, there is a possibility that the issue of greenhouse gases will bring about serious societal problems in the near future. The U.S. futures exchange, CME, expressed their view on “two-thirds of the world’s population facing a water shortage due to global warming and an increase in population”. According to the Food and Agriculture Organisation of the United Nations, the livestock industry accounts for about 15% of man-made greenhouse gas emissions. Furthermore, it is generally said that approx. 20,000 litres of water is required to produce 1kg of beef, approx. 6,000 litres for 1kg of pork, and approx. 4,500 litres for 1kg of chicken. Under these circumstances, there has been a concentration of investment funding in “food tech” that creates meat from plants. There will likely be an increase in demand for substitute foodstuffs that pose a low burden on the environment.

In the 25/1 issue, we will be covering JGC Holdings (1963), Fuji Oil Holdings (2607), Weathernews (4825), and Ferrotec Holdings (6890).

Japan_Weekly_Strategy_Report3 PDF

・Established in 1928 as Japan Gasoline Co., Ltd. In addition to a comprehensive engineering business, which manages the design, procurement and construction, etc. of various plants and facilities, the company expands the functional materials manufacturing business, which carries out the manufacture and retail of catalysts and fine products, etc.

・For 1H (Apr-Sep) results of FY2021/3 announced on 10/11, net sales decreased by 8.7% to 199.4 billion yen compared to the same period the previous year and operating income increased by 59.8% to 11.508 billion yen. While stagnant crude oil prices and the global economic depression due to the COVID-19 catastrophe had affected, on the other hand, the upturn in profit margin due to improvements in profitability in their comprehensive engineering business contributed to an increase in operating income.

・For its full year plan, net sales is expected to decrease by 0.2% to 480 billion yen compared to the previous year and operating income to decrease by 1.2% to 20 billion yen. In comparison to this year’s target order of 670 billion yen, they secured a 500 billion yen order due to the contribution of the Refinery Upgrading Project in Iraq. In addition to the tense power supply and demand becoming a social problem due to the insufficiency of liquefied natural gases (LNG), which are used in power generation fuel, there is a strong prediction that natural gases will become a mainstay for hydrogen manufacturing materials, hence, the demand for LNG plant construction is likely to rise.

・Established in 1950 via investment by Itochu (8001). Mainly carries out the manufacture and retail of oil and fat products, products involving confectionery and bread-making materials, and soy-based products. Company is recognised for its unique technology, such as the development of chocolate that does not become sticky when touched.

・For 1H (Apr-Sep) results of FY2021/3 announced on 6/11, net sales decreased by 9.9% to 172.589 billion yen compared to the same period the previous year and operating income decreased by 19.6% to 7.388 billion yen. Due to the impact from the COVID-19 catastrophe in both Japan and overseas, there was a decrease in revenue across all businesses, which are the soy-based processed materials, emulsification and fermentation materials, industrial-use chocolate and vegetable oil and fat. There was a decrease in profit for the 3 businesses except for industrial-use chocolate.

・Company revised their full year plan downwards on 6/11. Based on the viewpoint that the impact of the COVID-19 catastrophe will extend to the end of the current year, net sales is expected to decrease by 6.2% to 360 billion yen (original plan 370 billion yen) compared to the previous year (results after adjustment) and operating income to decrease by 23.1% to 16.5 billion yen (original plan 19.3 billion yen). The launch of the deli, “UPGRADE”, where its menu is comprised of hamburger steaks and karaage, etc. using soy-based meat and new soymilk materials via a patented manufacturing method (USS manufacturing method), is likely to raise the company’s brand value in the substitute foodstuffs market.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: