Report type: Weekly Strategy

”Is It the Time to Estimate the Point Where the Correction Phase Ends?”

We are beginning to see signs of a process of economic expansion from the resumption of economic activities. On 30/7, as a COVID-19 prevention measure, Tokyo announced the call again to shorten the operation hours of karaoke and F&B outlets serving alcohol across all areas in Tokyo in the period between 3/8 to 31/8. It appeared as if the hands of the clock had gone back to the time after the consecutive holidays involving the Spring Equinox Day in March this year where the conference was held on self-restraint from going outdoors unnecessarily. Also, in the stock market, Japan Airlines (9201) fell below 1,700 points during trading hours on 31/7, which came close to their year’s lowest of 1,656 points recorded on 6/4 this year. ANA Holdings (9202) also fell to 2,120 points during the trading hours of 31/7, which came close to their year’s lowest of 2,060 points recorded on 6/4. Being led by the fall in airline stocks whose business performance are easily affected by the flow of people following the resumption of economic activities, could the entire Japanese stock market be headed for a second low as well?

On the other hand, according to movements involving the COVID-19 infection released by Tokyo, as of 30/7, with 1,154 people hospitalised (2,800 beds secured) and of which 22 people are in intensive care (100 beds secured), the healthcare system is still able to manage, and it is thought that the situation differs from that in Spring. Also, in response to the call again to implement 70% of telecommuting in the financial world by Nishimura, the minister in charge of economic revitalisation, major Japanese corporate groups such as NTT (9432) are starting to take action towards the shift to an economy and businesses with telecommuting as a premise. The construction of a telecommuting society is seen as something that will become a major pillar for the Japanese economy.

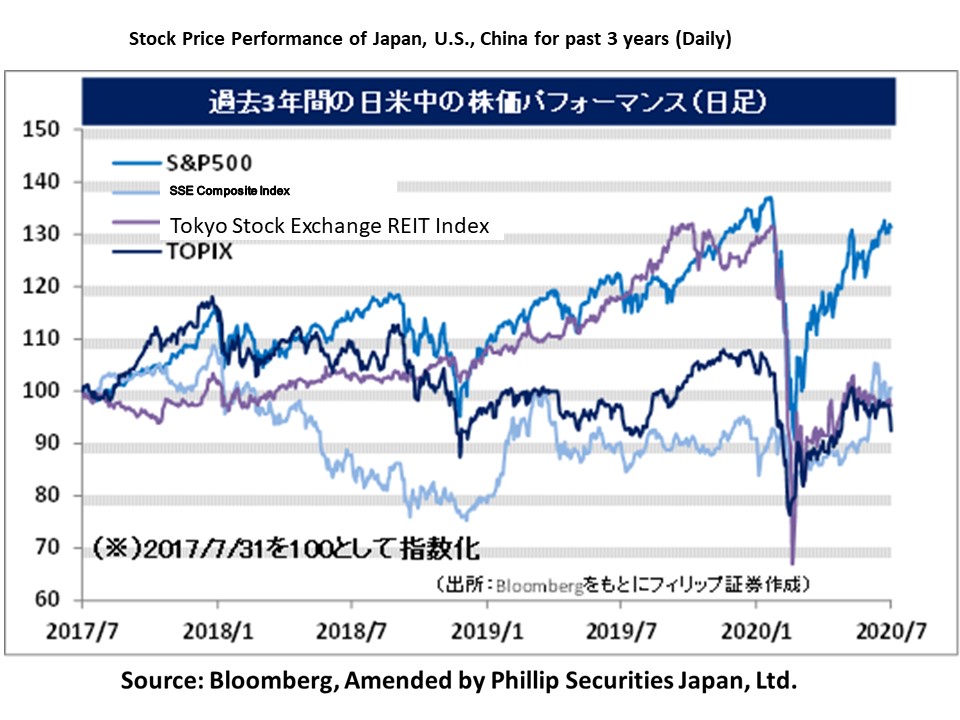

Looking back at the Nikkei average, there are 43 business days between the year’s high of 24,115 points recorded on 17/1 and the year’s low of 16,358 points recorded on 19/3, and 22/5, which is the 42nd business day counted from 19/3, is the starting point of the accelerated rise in the Nikkei average until the high of 23,185 points recorded on 9/6 since March. Considering the cyclic nature of these price movements, since the 42nd business day will be 6/8 and the 43rd business day will be 7/8 when counted from 9/6, we can also infer that there is a possibility that the correction phase following the fall in the Nikkei average from around 15/7 will continue. Since the weighted average P/B ratio (price-to-book ratio) of the Nikkei average’s closing price on 30/7 is 1.06 times, calculating the Nikkei average equivalent to a weighted average P/B ratio of 1.0 times would give 21,074 points. With the number of new unemployment insurance claims announced in the U.S. every week increasing compared to the previous week for 2 weeks straight, etc., recovery in employment is starting to show signs of a limit. 7/8 is also a date where the U.S. employment statistics will be announced, and could also be an important turning point from the viewpoint of fundamentals.

Apart from the COVID-19 catastrophe, there is a demand for urgent response to natural disasters such as river floods following torrential rain. Whereas in overseas, there has been a large outbreak of dengue fever in Singapore. Attention would also likely be on which Japanese company will contribute to the resolution of these issues.

In the 3/8 issue, we will be covering Tama Home (1419), Achilles (5142), Giken (6289), and Stanley Electric (6923).

・A built-to-order detached home housing construction company established in 1998. Manages the housing business, the real estate business, the financial business, the energy business and other businesses. Expands the management policy of “offering high quality housing at low prices” nationwide.

・For FY2020/5 results announced on 13/7, net sales increased by 12.0% to 209.207 billion yen compared to the previous year and operating income increased by 34.0% to 9.873 billion yen. For their mainstay housing business, net sales increased by 10.2% and operating income increased by 4.7 times. The increase in the number of business offices (7.5% increase compared to the previous year) and the region-limited products performing strongly, in addition to improvements in profit margin, etc. have been successful.

・For FY2021/5 plan, net sales is expected to decrease by 6.8% to 195 billion yen compared to the previous year and operating income to decrease by 24.0% to 7.5 billion yen. With the increase in movements involving the purchase of detached housing due to preparations for telecommuting under the spread of COVID-19 and the increase in time spent with the family, the company being in a relatively low price range for built-to-order housing is likely to appeal to the younger generation who are used to telecommuting. There is also a need to note that the company’s predicted dividend per share is 60 yen.

・Established in 1947. Their main businesses are the manufacture and retail of industrial material products, plastic products and shoe products. Since their success in the development and commercialization of Japan’s first soft vinyl chloride sheet in 1948, they have been offering diverse range of film products.

・For FY2020/3 results announced on 29/5, net sales decreased by 6.4% to 80.225 billion yen compared to the previous year and operating income increased by 14.3% to 1.602 billion yen. Despite a reduction in operating deficit and the decrease in revenue in the shoes business as well as a decrease in operating profit and revenue in the plastics business, for the industrial materials business, industrial materials for the semiconductor field overseas and medical equipment in Japan performed well, which led to an operating profit.

・Their FY2021/3 plan is undecided due to the unclear impact of the COVID-19 catastrophe. Although the shoes business, which accounts for 15% of sales revenue, is predicted to have a revenue decrease due to the decrease in people going outdoors following the COVID-19 catastrophe, the films in the plastics business (sales distribution ratio of 47%) is predicted to increase in demand for infection prevention gowns and respiratory droplet infection prevention sheets, etc. It was said that the orders for vinyl chloride sheets across 3 days in April was the amount of orders for a month.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: