Report type: Weekly Strategy

Is a New Common Sense Forming in Japanese Stock Investment?

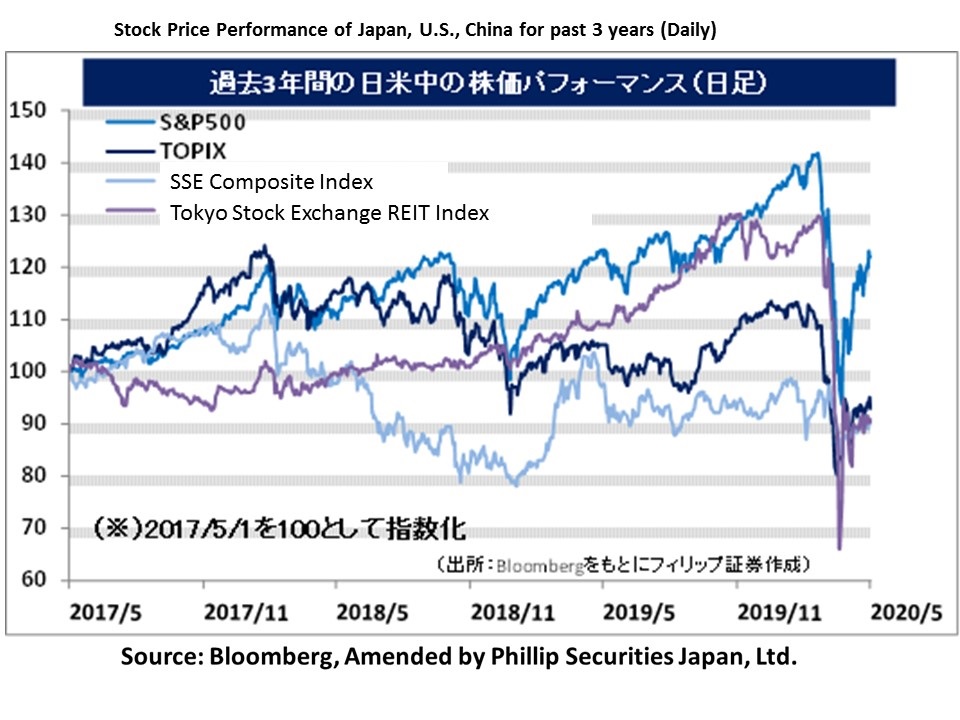

With the decreasing trend in the number of new COVID-19 infections in Tokyo with 47 infections on 29/4 and 46 infections on 30/4, the government embarked on adjustments to extend the declaration of a state of emergency to end May, which was due to end on 6/5. If we recall last year during the 10-day holiday following the change in the Japanese era name from Heisei to Reiwa, after the Nikkei average rose to the 22,300 point level in mid-April as a result of buybacks of credit sales positions prior to the holidays, the declining trend grew stronger after the holidays, which saw it fall to the 20,200 point level in mid-June, hence, the market tends to be strong in April and weak in May. Also, for this year, currently in U.S. stocks, the Jan-Mar term financial results of Alphabet (GOOGL), Microsoft (MSFT), Facebook (FB), Apple (APPL) and Amazon.com (AMZN) were announced between 28/4 to 30/4, and we are seeing a situation where it is easy to be aware of a sense of an exhaustion of source material influencing the market. Just at that moment, the Nikkei average rose to 20,365 points on 30/4, which has achieved a return to the half price of the range of decline from the high price of 24,115 points since 17/1 last year and the low price of 16,358 points since 19/3 last year. This can be said to be a state where there is a pause in the rise.

With regard to the Japanese stock market forecast in the future, it is believed that the response of stock prices to the dollar/yen exchange rate will play a vital role. After the global stock market plunge due to COVID-19 effects and since the sharp rise in demand for dollar funds, which is a key currency, the “risk off dollar appreciation and risk on dollar depreciation” is starting to stabilise. The common sense in Japanese stock investments thus far of “the yen appreciating against the dollar being a source of material for selling Japanese stocks” is starting to lose its credibility. The reason for this is the shift in funds to risk funds simultaneously brought about by the depreciation of the dollar that was induced by vigorous monetary easing policies by the U.S. Federal Reserve Board (FRB). In the future, we could see a rise in situations where market participants would be stumped at the increase in Japanese stocks following a progression of the yen appreciation.

In addition, benefits in the cost aspect involving cheaper crude oil are likely to significantly influence the Japanese economy. Furthermore, with the effects of COVID-19 raging throughout the world, the English BBC broadcast released a special feature on “the healthiest countries to live in”, where Japan was listed as the top. It praises the high standard of lifestyle and culture where “a health-conscious culture limits the impact of COVID-19 risks to a minimum”. In the future, when there is an easing of restrictions on the movement of people across borders, there is a chance that foreigners will come to see Japan as an even more attractive country, which could be a good opportunity to trade against the trend for inbound travel-related stocks. Through this COVID-19 pandemic experience, perhaps we will see a new emphasis where the health and hygiene aspect would serve as the basis for the selection of targets to invest global money in. Either way, we may come to require a completely new form of common sense in the investment world.

In the 7/5 issue, we will be covering Takeei (2151), Sumitomo Chemical (4005), Mercari (4385), and Tsuzuki Denki (8157).

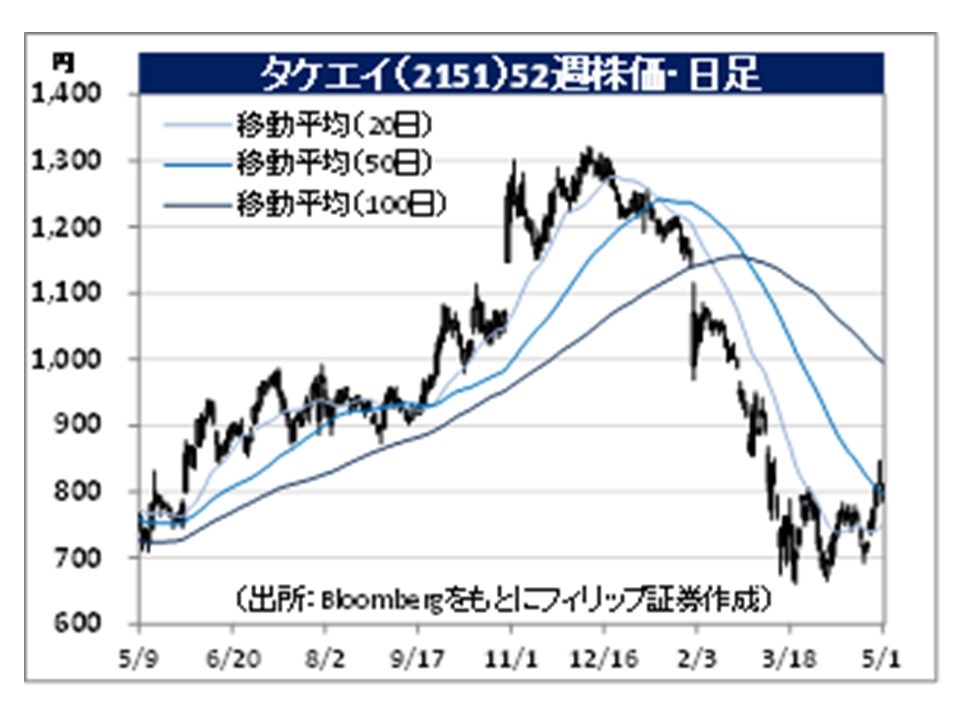

・Established in 1977. Their main business is the waste processing and recycling business. Aiming for a comprehensive environmental business, their accompanying businesses are the renewable energy business, the environmental engineering business and the environmental consulting business.

・For 3Q (Apr-Dec) results of FY2020/3 announced on 30/1, net sales increased by 17.2% to 27.29 billion yen compared to the same period the previous year and operating income increased by 55.2% to 2.223 billion yen. Their mainstay waste processing and recycling businesses was strong due to an increase in the processing of disaster waste from natural disasters with net sales increasing by 10.1% to 19.368 billion yen and operating income increasing by 70.0% to 1.868 billion yen.

・For its full year plan, net sales is expected to increase by 13.4% to 36.6 billion yen compared to the previous year and operating income to increase by 45.8% to 3.1 billion yen. On 23/4, company announced that they would inherit the biomass power generation business for 4.3 billion yen that was withdrawn by Mitsui E&S Holdings (7003) to improve finances. Green Power Ichihara, which supports the business, is the metropolis’ largest scale woody biomass power generation business operator, and we can expect an expansion of the renewable energy business from the acquisition of a large-scale power station.

・Founded in 1913 in Niihama, Ehime Prefecture. Offers products supporting the lifestyles of people and a wide range of industries globally across 5 business fields, which is petrochemistry, energy and functional materials, information electron chemistry, the health and agriculture-related and pharmaceuticals.

・For 3Q (Apr-Dec) results of FY2020/3 announced on 31/1, sales revenue decreased by 3.7% to 1.6507 billion yen compared to the same period the previous year and core operating profit which indicates recurring profitability decreased by 25.0% to 116.271 billion yen. Despite an increase in revenue and an increase in core operating profit in pharmaceuticals, in their mainstay petrochemical business, net sales decreased by 10.2% and core operating profit decreased by 47.1%.

・For its full year plan, sales revenue is expected to increase by 0.5% to 2.33 trillion yen compared to the previous year and core operating profit to decrease by 21.7% to 160 billion yen. The company possesses listed subsidiaries such as Sumitomo Dainippon Pharma (4506) and Koei Chemical (4367), and we can expect a focus and selection of corporate groups that have gone through a resolution of parent-subsidiary listing. Also, if low crude oil prices persist, global competitiveness of petrochemical complexes will increase and we can expect this to benefit their petrochemical business.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: