|

Report type: Weekly Strategy |

■ Increase in the Bank of Japan’s Price Outlook, Europe Risks and the Long-Term EV Outlook

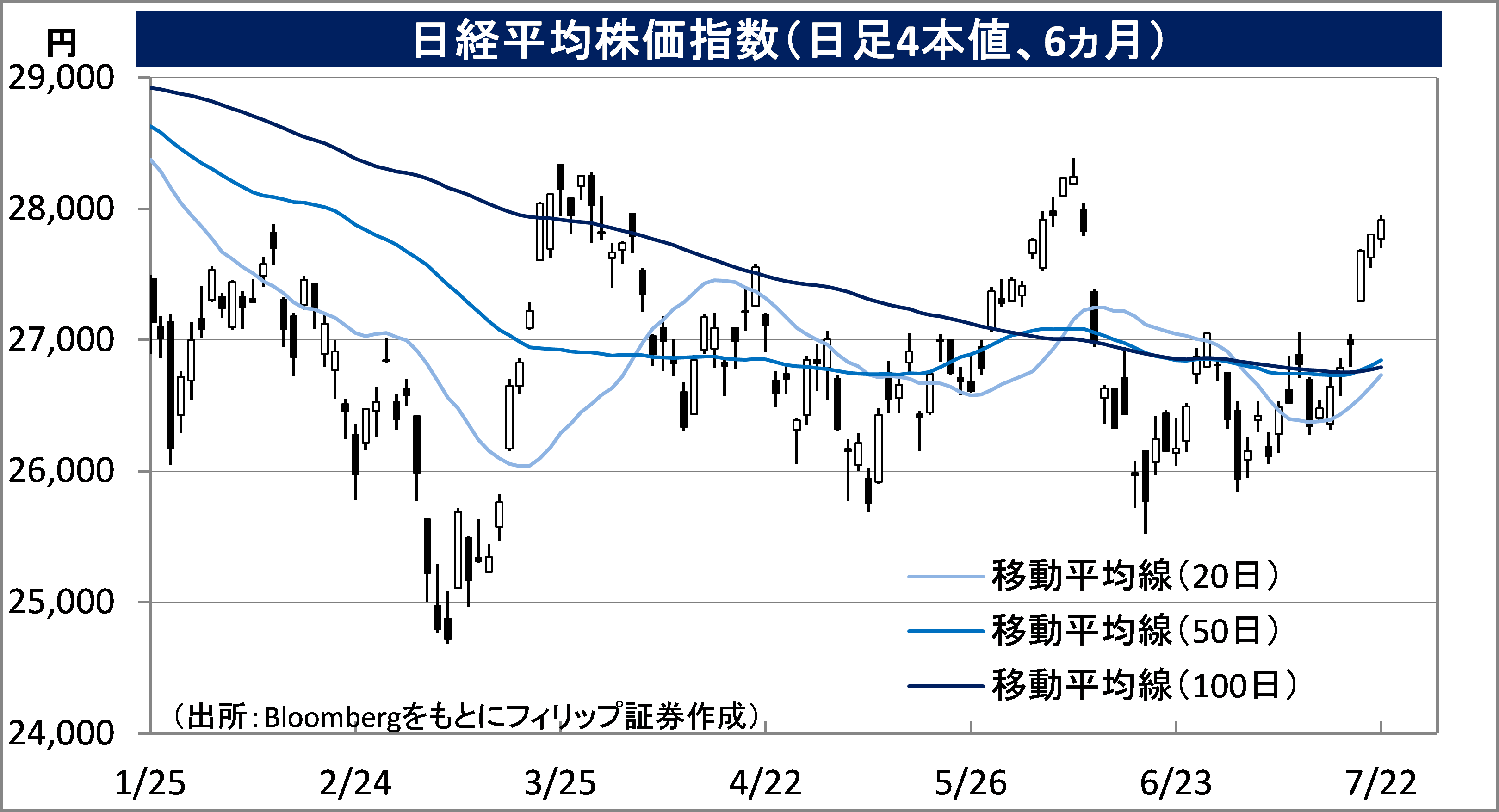

On the 21st at the Monetary Policy Meeting, the Bank of Japan decided to maintain the current large-scale monetary easing that keeps interest rates low, and at the same time, it raised the outlook for price inflation this fiscal year from 1.9% indicated in April to 2.3%. Although the Bank of Japan states that this price inflation is not accompanied by a wage increase, it is expected that it will cause an increase in the negative real interest rate (inflation-indexed bonds), which is obtained by deducting the expected inflation rate from the nominal interest rate. In theory, when there is a negative real interest rate, due to the value of money being less than the value of goods, it would be more beneficial to purchase goods or for capital investment by borrowing money, which would tend to function in the direction of the way the economy goes. However, there will likely be caution on the aspect of an increase in pressure of the yen depreciating against the dollar due to the increase in difference between the U.S. and Japan’s real interest rate.

As of the 20th, for the closing price of the U.S. and Japan’s 10-year inflation-indexed bonds (TIPS), compared to the U.S. at +0.642%, Japan was -0.701%. In terms of financial environment, Japan’s economy is more readily influenced compared to the U.S., therefore, for the stock market as well, perhaps there is also an aspect where Japan’s economically-sensitive stocks and growth stocks tend to be bought easier than those of the U.S.

The focus of the global financial market is gradually shifting towards Europe. In response to the rate of increase of the Consumer Price Index (CPI) for June in the eurozone having increased by 8.6% compared to the same month the previous year which is a record high, an interest rate hike of 0.50%, which is double the usual, was decided at the European Central Bank (ECB) council meeting on the 21st. However, the eurozone possesses a structural vulnerability of an issue of “regional disparity” due to the increase in interest rates in Southern Europe, which is heavily in debt. Most recently, in Italy, the coalition government collapsed from the resignation of Prime Minister Draghi, which is spurring political confusion. The Italian government’s outstanding debt to GDP ratio has exceeded 150% of late compared to being at only around 120% between 2010-2011 when the European debt crisis occurred. Europe’s weakness is not only limited to risks of economic cooling following concerns of Russia’s natural gas supply to Germany. If there is an increase in Southern Europe’s government bonds following the disparity with Germany’s government bonds, sooner or later, a situation may emerge which will test the effectiveness of the “Transmission Protection Instrument (TPI)”, which was approved as a new bond purchase measure at this council meeting.

In the annual long-term EV (electric vehicle) outlook announced by BloombergNEF on 1/6, as the primary cause for acceleration in popularisation in China, global sales of EV passenger cars is expected to be at 20.6 million vehicles in 2025, which is slightly over 3 times the current and greatly exceeds the 14 million vehicles estimated a year ago. It is said that EV passenger cars use approx. 4 times more copper than passenger cars that use petrol, etc. China is the country that consumes the most amount of copper and as a result of its economic slowdown following its zero COVID policy, the price of the LME Copper futures (3-month contract) fell by more than 30% from its high since the beginning of the year that was marked in March recently. This might turn out to be an investment opportunity for nonferrous metal enterprises that deal with copper.

In the 25/7 issue, we will be covering Nippon Koei (1954), SMS (2175), Maxell (6810), and Toyota Tsusho (8015).

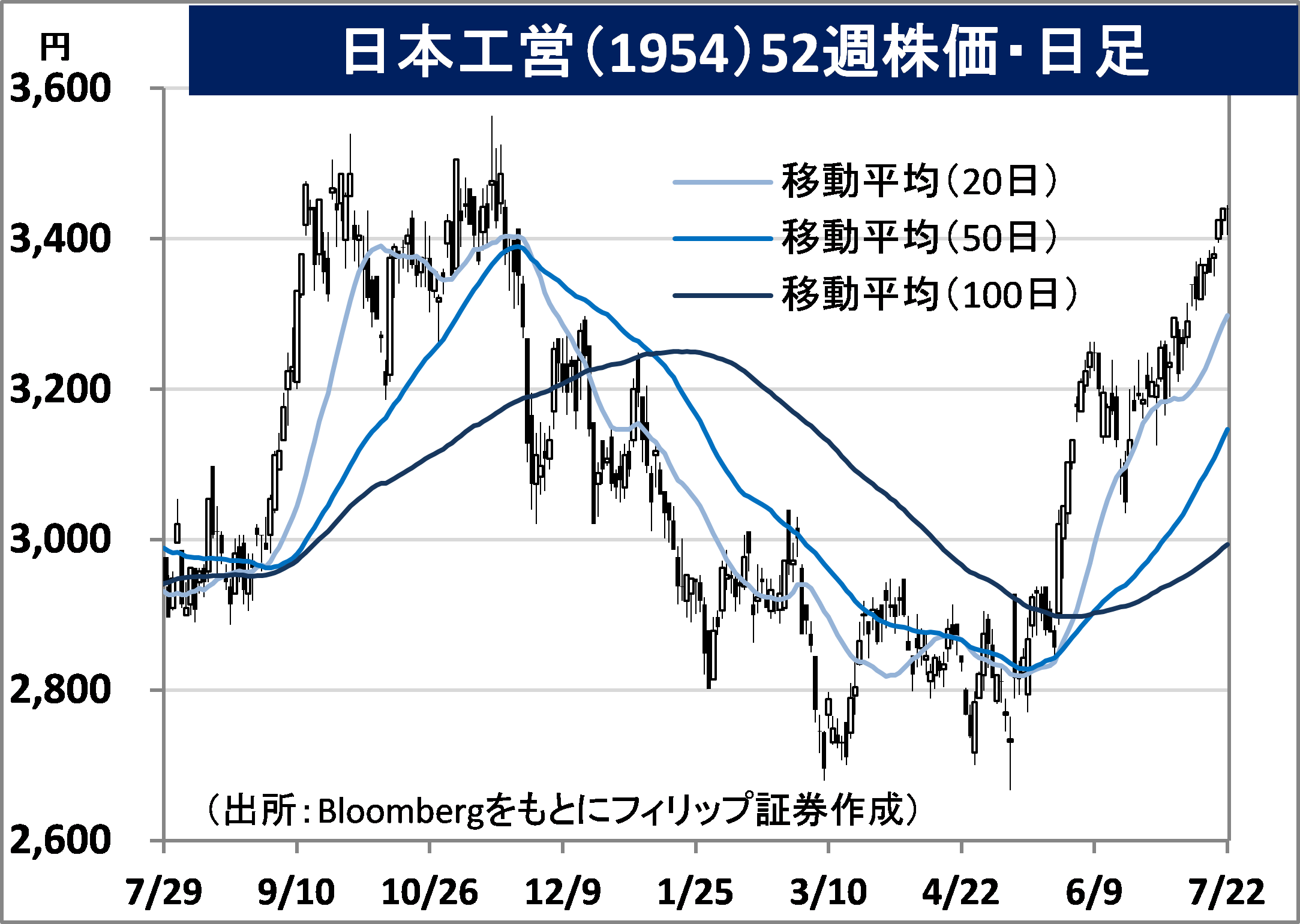

Nippon Koei Co., Ltd. (1954) 3,440 yen (22/7 closing price)

A general construction consultant founded in 1946 with the pre-war Korean electric industry as its parent. Operates the domestic consulting business, overseas consulting business, electricity engineering business, urban spatial business and the energy business, etc.

For 9M (Jul-Mar) results of FY2022/6 announced on 13/5, sales revenue increased by 10.6% to 95.682 billion yen compared to the same period the previous year and operating income increased by 39.0% to 9.509 billion yen. They are concentrating on 3 businesses, which are consulting, urban spatial and energy from the current period onwards. For operating income for each business, consulting increased by 43.8%, urban spatial increased by 2.3% and energy increased by 2.0 times.

Company revised its full year plan upwards. Although sales revenue remains unchanged to increase by 11.1% to 131 billion yen compared to the previous year, operating income is to increase by 26.3% to 9 billion yen (original plan 7.7 billion yen). Annual dividend is forecasted to have a 25 yen dividend increase to 100 yen. In addition to the company’s participation in the development survey of “Nusantara”, the new capital of Indonesia, along with SI giant TIS (3626), they are investing in an Indonesian Fintech enterprise which provides a transportation system electronic payment service, which will greatly contribute to Indonesia’s national policy (infrastructural development).

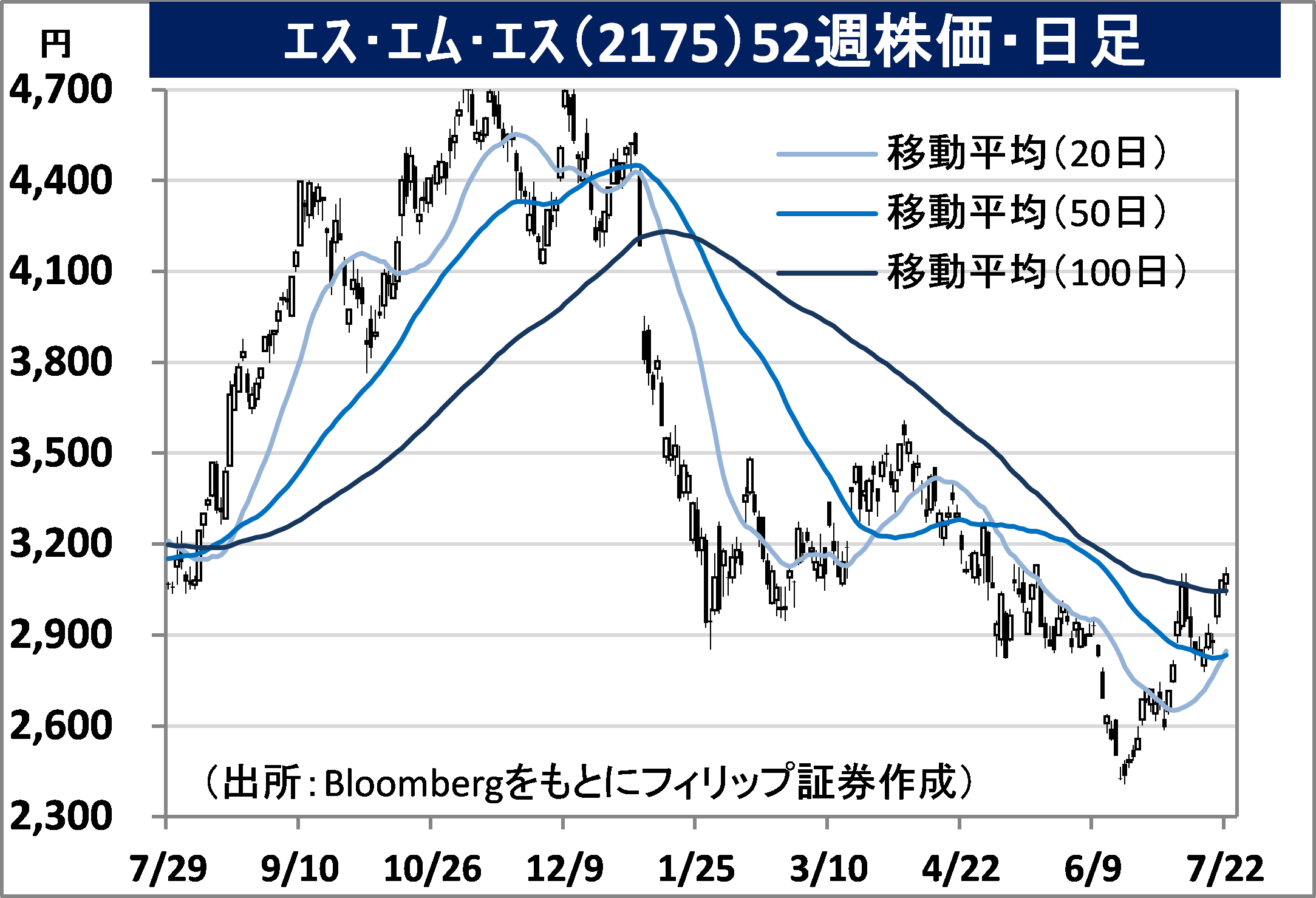

SMS Co., Ltd. (2175) 3,100 yen (22/7 closing price)

A recruitment industry leader geared towards the nursing care and medical industries which established in 2003. Mainly operates the “career field” which is a career-related business geared towards business operators, and the “nursing care operators field” which provides a management support platform geared towards nursing care operators, etc.

For FY2022/3 results announced on 28/4, net sales increased by 8.2% to 38.899 billion yen compared to the previous year and operating income increased by 15.5% to 6.318 billion yen. Although the career field stopped at a 0.1% revenue increase due to COVID-19, the nursing care operators field had a 21.5% increase in revenue, the overseas field had a 23.6% increase in revenue and the business development field had a 29.5% increase in revenue, which grew and contributed to business performance.

For its FY2023/3 plan, net sales is expected to increase by 18.4% to 46.063 billion yen compared to the previous year and operating income to increase by 14.6% to 7.238 billion yen. An increase in members is expected in the nursing care operators field. Regarding improvement in staff treatment in nursing care and nursing professions, as the focal policy of “enabling a good cycle of growth and distribution” via the Kishida administration, the salary of nurses is said to be raised by 4,000 yen which is equivalent to 1%, and for the salary of nursing care professions, by 9,000 yen which is equivalent to 3%, which is expected to benefit the company’s career field.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: