|

Report type: WeeklStrategy |

“Increase in Activity in the Movement of Activists and Fully Automatic Driving”

There has been an increase in activity in the movement of activists (activist shareholders), such as City Index Eleventh, etc. under the former Murakami Fund, Silchester from the U.K. and Oasis Management, which focuses on Hong Kong. There has been an increase in purchases of stocks related to construction, such as general contractors, and recently, pressure to reinforce a bold return to stockholders, such as a significant increase in dividends and stock buyback TOBs with the target being second-tier major general contractors, such as Nishimatsu Construction (1820) and Hazama Ando (1719). Since November, City has been expanding purchases of Pacific Metals (5541), which is under the Nippon Steel group.

Generally, cash-rich stocks where its stock prices are left undervalued are targeted. In “Lifetime Investor” authored by Yoshiaki Murakami, he mentions “screening the shareholder composition, P/B ratio and percentage of cash and deposits accounted for in the market capitalisation, etc. through scoring when choosing stocks to invest in using a fund”. Furthermore, it appears that the point of time when there is a drop in sales while prioritising sound finance is seen as an investment opportunity. As reserves for a return to stockholders, such as dividends and stock buybacks, etc., it appears that there is a wide use of the “net cash ratio”, which is obtained by dividing market capitalisation by net cash (cash and deposits + short-term investment securities – interest-bearing debt). In particular, it is likely that each of the recent general contractors that peaked out in construction related to the Tokyo Olympics while having highly sound finances and a tendency to have sluggish orders and sales as a result of COVID-19 was a factor for them to be targeted by activists.

Also, one of the conventional tactics of activists can be said to be the aspect of corporate governance, such as the nature of collusion in the general contractor industry where there are too many industry players posing a problem which leads to a reorganisation to be easily set up, such as a merger between two corporations that are invested in, which is used as a trigger to increase return on investment.

Among general contractors, in addition to Taisei Corporation (1801), which developed a concrete technology that traps CO2 using calcium carbonate, their subsidiary, Taisei Rotec, is cooperating with Aizawa Concrete from Hokkaido in researching a “self-healing type of asphalt” coating which naturally mends cracks, with plans for a test construction this fiscal year and efforts focusing on technological development. Perhaps there may be a need for an industry reoganisation towards strengthening overseas expansion and technological development.

In addition to the U.S. communication semiconductor indicating prospects of sales expansion involving those for automatic driving systems and next-gen Qualcomm (QCOM) driving support, etc., it was reported that the U.S. Apple (AAPL) is putting their focus on a project in developing a fully autonomous driving function in electric car (EV) development. Perhaps it will soon be the turn for the spotlight for Nisshinbo Holdings (3105), which has technology in simultaneously detecting speed information and 3D positional information through their subsidiary JRC Mobility, and for Zenrin (9474), which deals with map information required for automatic driving.

In the 22/11 issue, we will be covering Toda (1860), Takeuchi MFG (6432), Advantest (6857), Nitto Denko (6988) and Wilmar International (WIL).

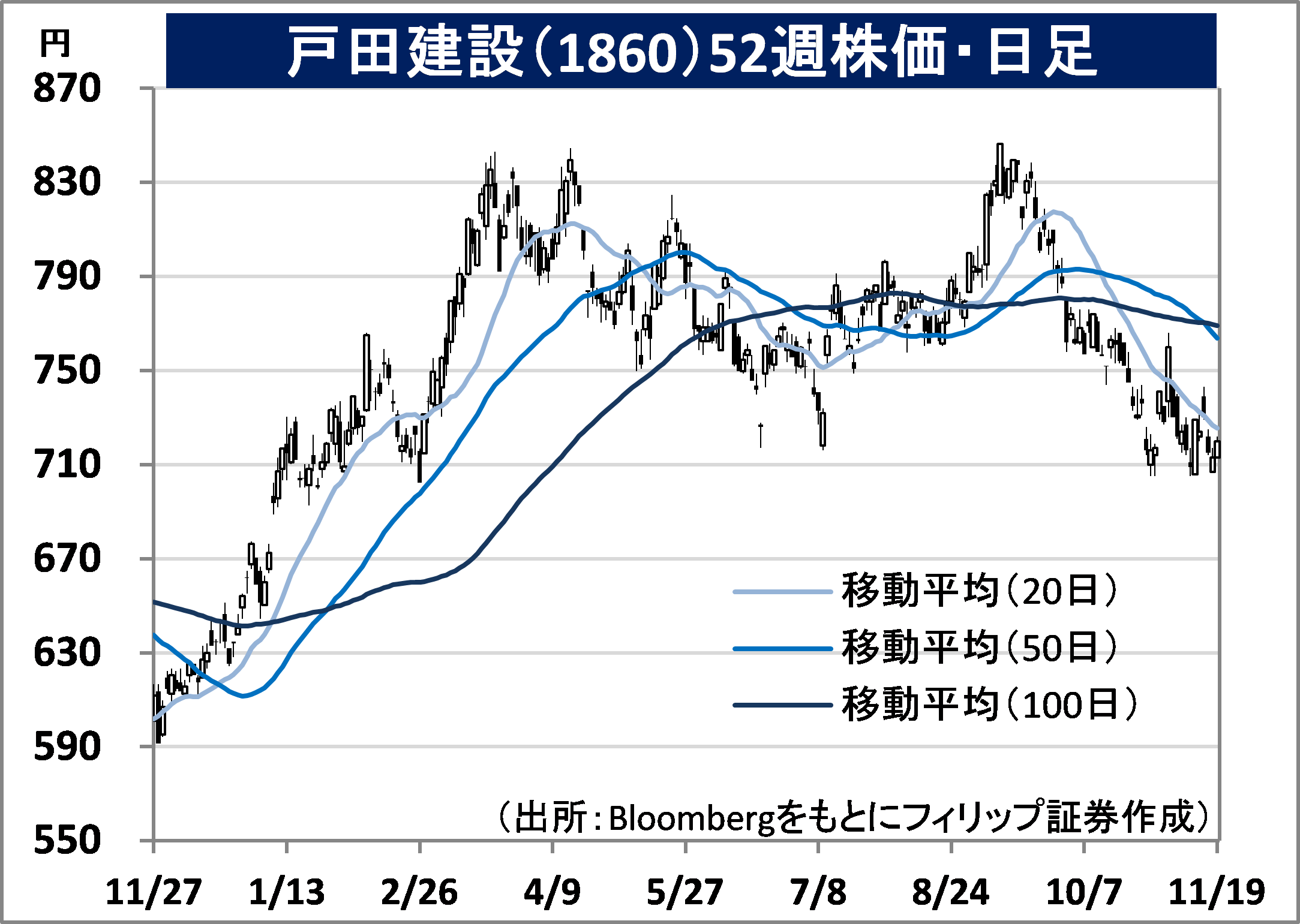

・Founded in 1881. Their main businesses are the domestic construction business, domestic civil engineering business, investment development business, new fields business (including the floating offshore wind power generation business) and overseas businesses, and expands the PFI business involving each of their businesses, etc.

・For 1H (Apr-Sep) results of FY2022/3 announced on 15/11, net sales increased by 9.8% to 235.574 billion yen compared to the same period the previous year and operating income increased by 40.8% to 8.598 billion yen. The increase in good profit construction in the civil engineering business and the increase in real estate business earnings in the investment development business contributed to the increase in operating income. Ordinary income increased by 44.2% as well due to the contribution from dividends received from investment securities.

・For its full year plan, net sales is expected to increase by 1.6% to 515 billion yen compared to the previous year and operating income to decrease by 14.8% to 23.6 billion yen. While there are expectations of public investment focusing on infrastructure development, in the profit aspect, they have considered the impact on construction progress following supply constraints. In June this year, they were selected as one of the 6 joint business operators for the floating offshore wind power generation in Nagasaki Prefecture’s Goto City offshore coastal waters. With activists joining the list of major stockholders, there will likely be a demand for continuing to respond to requests of a return to stockholders.

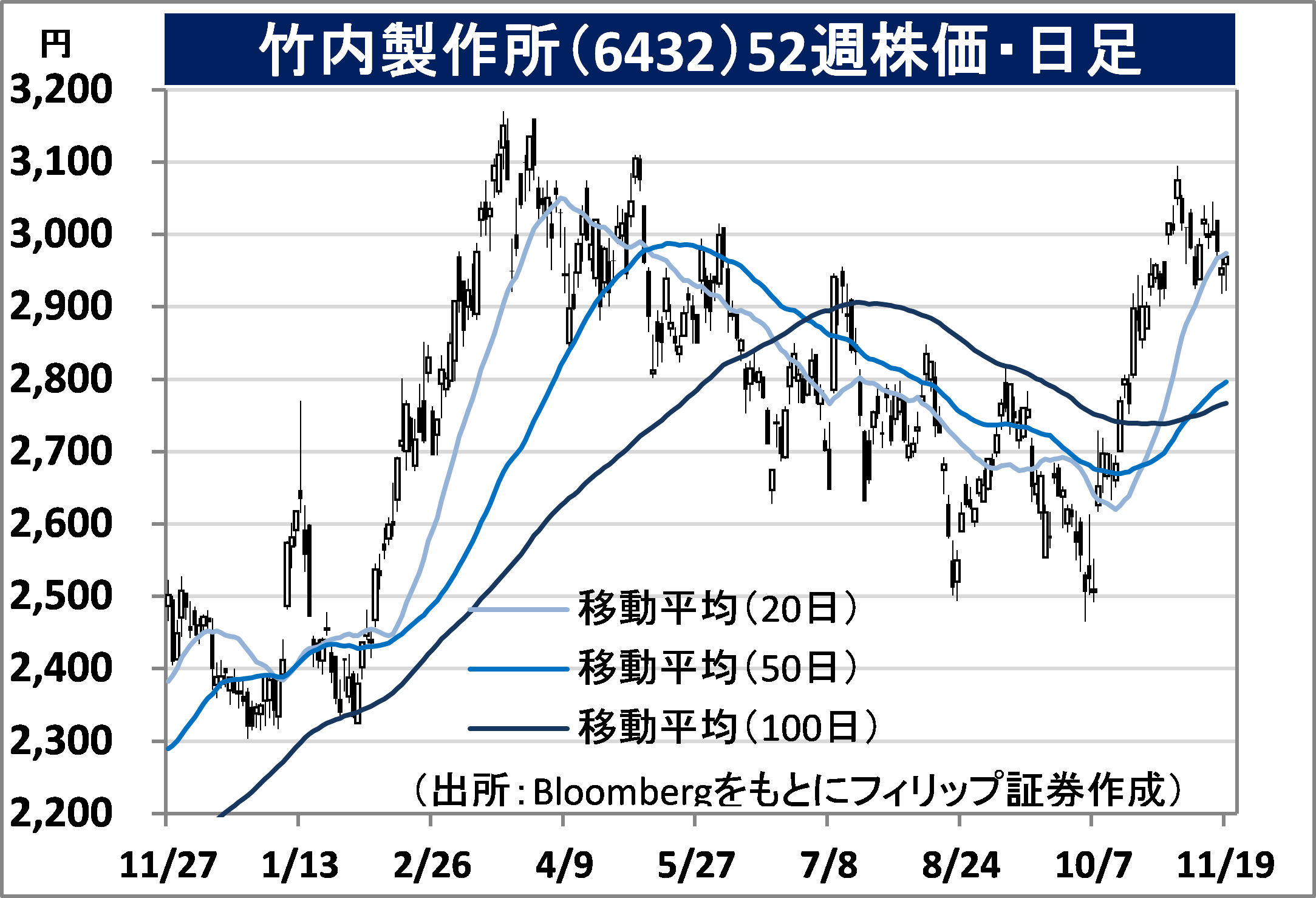

・Established in 1963. Carries out the manufacture and sale of construction machinery. Their main items are the mini shovel, hydraulic shovel and crawler loader with an overseas sales ratio of approx. 98%. They also handle agitators for the chemical and food industries and wastewater treatment facilities.

・For 1H (Mar-Aug) results of FY2022/2 announced on 7/10, net sales increased by 39.6% to 74.228 billion yen compared to the same period the previous year and operating income increased by 46.1% to 9.958 billion yen. Despite there being an increase in transportation charges and manufacturing cost, etc., the lifestyle infrastructure public business is looking up in the West. Product demand is performing strongly as a result of an increase in construction related to housing, such as new construction, remodelling and expansion, etc. particularly in the U.S.

・For its full year plan, net sales is expected to increase by 19.4% to 134 billion yen compared to the previous year and operating income to increase by 7.5% to 14.2 billion yen. With the company’s base in Nagano Prefecture, they developed the world’s first “mini shovel” construction machine weighing under 6 tonnes. Although it is not suited for large-scale construction compared to the 20 tonne-class ones excelled in by major companies such as Komatsu (6301), it has been actively used in urban area housing and waterworks construction. There is an emphasis on those geared towards lifestyle infrastructure in the 1 trillion dollar infrastructure investment bill passed in the U.S. as well.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: