Report type: Weekly Strategy

Implications of Trading Company Stock Purchases by “the Wise Man of Omaha”

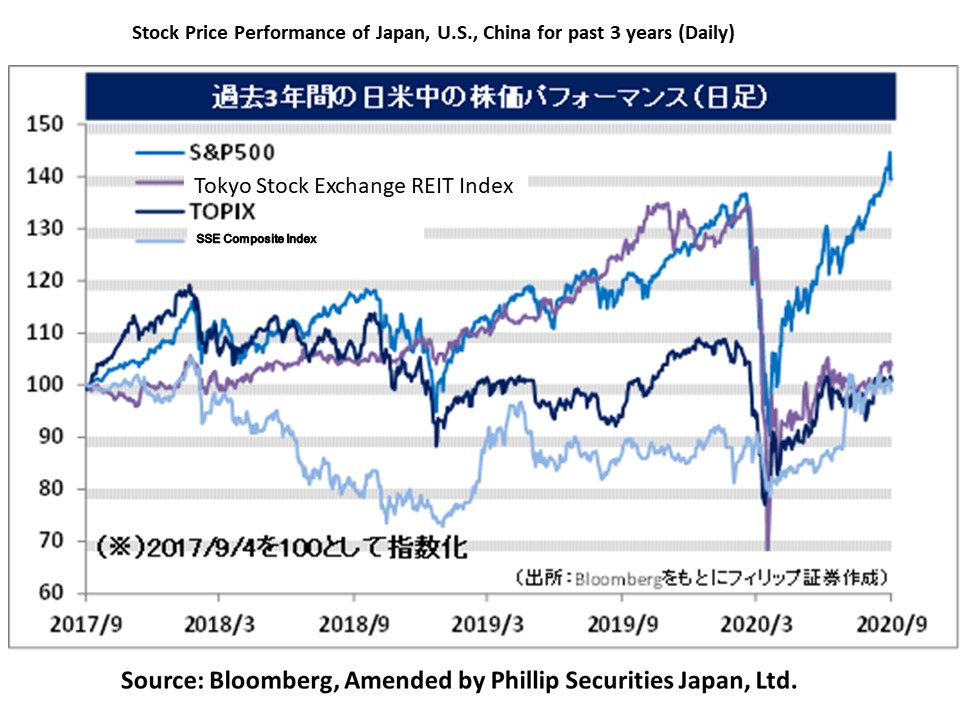

US investment firm Berkshire Hathaway, led by Warren Buffett, has been creating waves through its purchase of the five major general trading company stocks in Japan. Looking at the “Buffet Index” (Market capitalization of a country ÷ Nominal GDP of the country x 100), which originated from him, it is possible that US stocks are at a higher level than that during the IT bubble in the late 1990s. It could therefore be that Mr. Buffet is expecting foreign stocks to become more attractive as inflation progresses and the US dollar becomes weaker.

Berkshire issued its first yen-denominated bond in September last year. The total amount issued was 430 billion yen for six corporate bonds with maturities ranging from 5 to 30 years. Of these, the 10-year and 5-year bonds have low interest rates of 0.44% and 0.17% respectively. Using the yen funds raised as a result to invest in Japanese stocks with high dividend yields can ensure stable and long-term earning of carry income derived by subtracting costs from income gain.

Generally, when an overseas investor holding US dollars raises yen funds to invest in yen assets, it is also possible to convert the dollar funds into yen through dollar-yen swaps besides issuing bonds denominated in yen. If such a “dollar carry trade” is carried out on a large scale, we may expect the dollar-yen exchange rate to swing in favor of the yen’s appreciation. However, the strong yen in this case does not imply a risk-off environment. Rather, it indicates a “Japan buying” scenario with the same type of money flow as seen during the “high yen, high Japanese stock” situation after the 1985 Plaza Accord. It is therefore most noteworthy that Mr. Buffet’s purchase of the stocks of the trading companies has implications for a possible “high yen through Japanese purchases”.

This implies a need for a paradigm shift from “Abenomics”, in which yen depreciation accompanying unprecedented monetary easing is the main driving force for economic growth. At the moment, Chief Cabinet Secretary Suga is strongly slated to be the next prime minister, and at a press conference on 2/9, he said that he would “responsibly take over”

Abenomics. For a paradigm shift towards “Japan buying” by foreign investors, key will be the people assuming the major Cabinet posts. Firstly, the appointment of Defense Minister Kono, who is eager to expand cooperation in the “Five Eyes” framework for sharing confidential information amongst the five countries consisting of the US and UK etc, as the Chief Cabinet Secretary, and the appointment of Tax Panel Chief Amari, who is likely to proactively push forward financial measures as opposed to the fiscal consolidation stance of the Ministry of Finance, as the Minister of Finance, may encourage “Japan buying” in the context of the stock market.

Stock volatility is expected to rise further due to the MSQ (major SQ) related to Nikkei Average futures and options trading on 11/9, and the sharp drop in major US IT shares on 3/9. We therefore need to be very cautious.

In the 7/9 issue, we will be covering Sumitomo Forestry (1911), USS (4732), Nihon Nohyaku (4997), and Marubeni (8002).

・Established in 1948. Dealing in the business of trees for both upstream and downstream processes. Owns about 1/900 of the land in Japan as forests for its Forestry Business. Sales of Timber and Building Materials Distribution Business and Wooden Custom-built Housing Business are the highest in Japan.

・For 1Q (Apr-Jun, change of accounting period from this term onwards) results of FY2020/12 announced on 12/8, net sales increased by 4.5% to 245.583 billion yen compared to the same period the previous year, and operating income increased by 2.1 times to 9.275 billion yen. Although home remodeling and real estate brokerage had struggled due to the effects of Covid-19 in Japan, home sales in the US had recovered rapidly after May owing to the decline in mortgage interest rates.

・For its full year plan (irregular: Apr-Dec), net sales is expected to be 777.0 billion yen, and operating income to be 22.5 billion yen. 41% of the company’s 1Q sales came from the overseas housing and real estate segment, backed by rising needs for relocation to relatively large properties in the suburbs as the practice of WFH becomes established in the US. On top of that, it is noteworthy that oxygen supply from the forests from the company’s Forestry Business is contributing to CO2 reduction, and the international price of timber is rising

・Established in 1997 through the merger of Seishin Sangyo and the former USS. Engages in purchase and sale of used cars centering on auto (car) auction. Company has 39% share of the auto auction market (2019).

・For 1Q (Apr-Jun) results of FY2021/3 announced on 3/8, net sales decreased by 19.2% to 16.056 billion yen compared to the same period the previous year, and operating income decreased by 26.7% to 6.734 billion yen. The number of used cars registered and exported decreased due to the impact of Covid-19, causing the number of cars sold / contracts in the auto auction market to decrease, thereby affecting results.

・For its full year plan, net sales is expected to decrease by 13.9% to 67.3 billion yen compared to the previous year, and operating income to decrease by 24.5% times to 27.2 billion yen. Amid the movement to change from train to car commuting to avoid “close contact”, the number of used cars registered (including minicars) in June was 4.8% higher than the same month the previous year. Average contract price in July increased by 18.6% YoY. Demand for exports is increasing for overseas regions where urban lockdowns have been lifted.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: