Report type: Weekly Strategy

How to Figure out and Survive the Tumultuous Market?

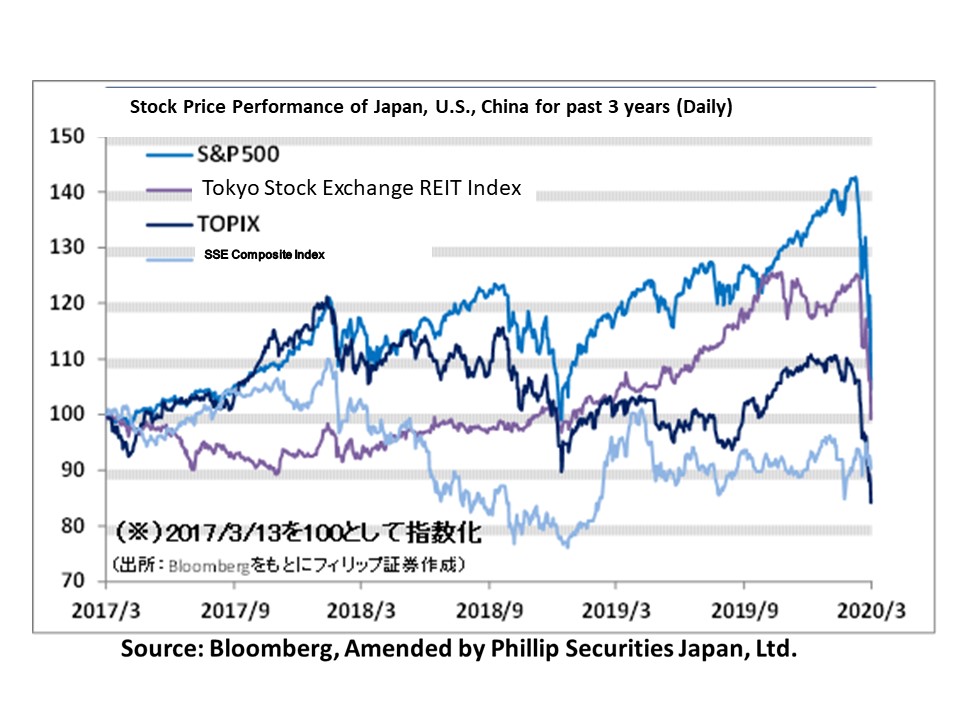

The Japanese market during the week of 9/3 was a tumultuous one. The Nikkei Average hit 20,347 points upon market opening on 9/3, but went into a wild spin upon news of strengthening COVID-19 infection in Europe. On 13/3, the Nikkei Average plunged to the 16,600 points range, its lowest since 2016/11 when President Trump was elected. In particular, President Trump’s announcement on banning entry from Europe (excluding the UK) after 12/3 and his suggestion of postponing the Tokyo Olympics by one year had significant impacts on Japanese stocks. The Nikkei Average fell more than 30% in less than two months from the high of 24,115 points on 17/1 to its low price on 13/3. Looking backwards, it can be said that this is almost comparable to what happened after the bursting of the Heisei bubble, when the Nikkei Average dropped about 30% within three months from 38,915 points at the end of 1989 to 27,251 points in the first week of 1990/4. At that time, the Nikkei Average did manage to recover half the losses when it rose to 33,344 points within two months by the first week of 1990/6. It is noteworthy that a phenomenon called “Mean Reversion”, where prices will tend to revert to the average price within a price range after a sharp fall within a short period, is likely to occur.

The Nikkei Average weighted average PBR (Price Book-value Ratio) was 0.89 times at the closing price of 18,559 points on 12/3. Based on the closing price on 12/3, the Nikkei Average on 2009/3 after the Lehman Shock when the PBR achieved a historical low of 0.81 times would have been 16,890 points. Depending on the extent of the spread of COVID-19 in Europe and the US, and on other triggering factors, there is a possibility for a reversion to a Mean Reversion from the current downturn. The day after President Trump’s announcement of a ban on entry from Europe, the US Fed announced a liquidity injection of USD1.5 trillion on 12/3 into the repo market. In addition, government securities purchased by the US Fed each month will include long-term bonds besides short-term bonds. In this regard, we may say that framework has been laid for the financial market to rebound quickly once the COVID-19 infection has been controlled in the US. In China, we may note that infections have slowed down for eight days after accelerating in 2020/2. We are also seeing derivative transactions taken by investors as part of their strategy to overcome current market fluctuations. Trading of stock index futures / options listed on the Osaka Exchange has been booming. Among spot trading ETFs (listed investment trusts) listed on the TSE, there are bear-type (inverse-type) ETFs of which the prices move in opposite direction from the Nikkei Average’s movement. After fully understanding the marketability of such products, and when the Nikkei Average has returned to a certain level, we may like to consider adding these to our portfolio for the purpose of hedging against downturns.

In the 16/3 issue, we will be covering Hisamitsu Pharmaceutical (4530), Giken (6289), Toshiba TEC (6588), and Japan Exchange Group (8697).

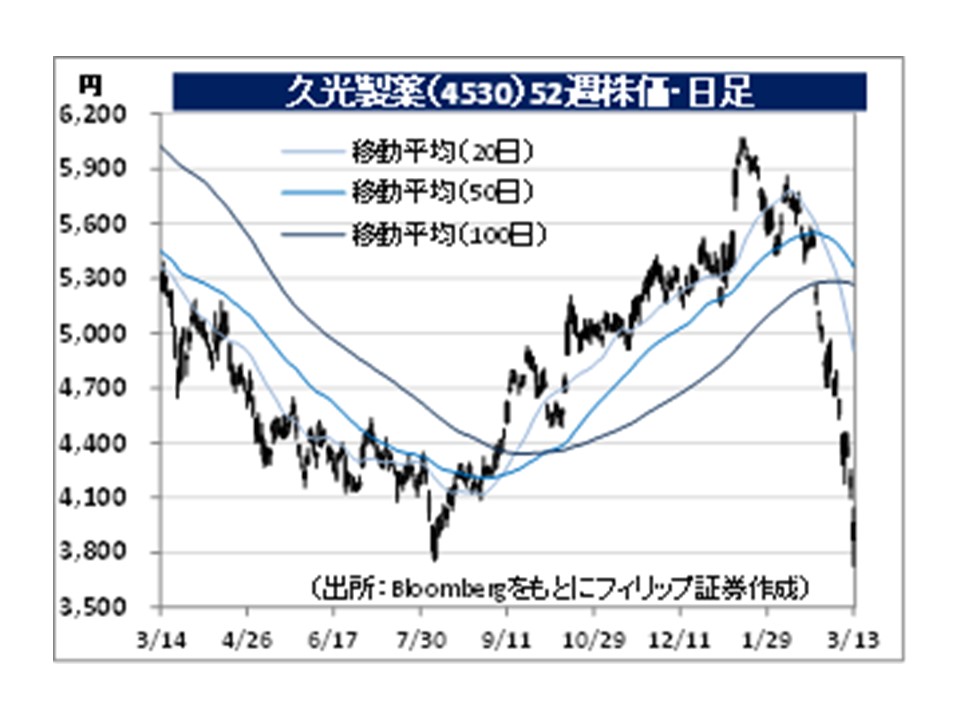

・Founded in 1847. Manufactures, sells, imports and exports pharmaceuticals and quasi-drugs. “SALONPAS” has been registered as a trademark in more than 100 countries and regions. Focusing on development of patches based on transdermal drug delivery systems.

・For 3Q (Mar-Nov) results of FY2020/2 announced on 10/1, net sales decreased by 3.4% to 99.078 billion yen compared to the same period the previous year, and operating income increased by 15.4% to 18.417 billion yen. Sales declined due to the impact of generics in the US ethical drug business and intensified competition in the domestic ethical drug business. However, improvements in the cost of sales ratio and decrease in SG&A expenses had contributed to profit growth.

・For its full year plan, net sales is expected to increase by 0.1% to 143.5 billion yen compared to the previous year, and operating income to increase by 2.8% to 22.9 billion yen. On 12/3, the Nikkei Keizai Shimbun reported that apparently full-year sales will decrease by 3%, and operating income will increase by 5%. “Haruropi Tape”, a transdermal therapeutic agent for Parkinson’s disease, released in Japan in 2019/12 is contributing to operating income. Demand is expected to increase as tremors in limbs due to ageing become a social problem as the population ages.

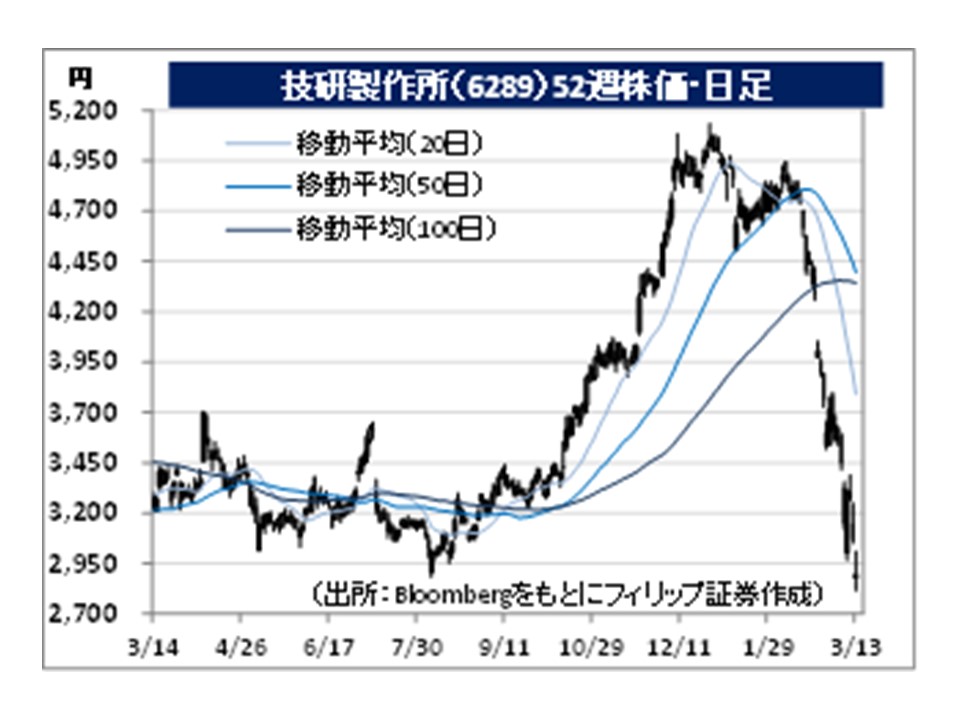

・Founded in 1967. Has the construction equipment business handling development, manufacturing, sales and maintenance of non-vibration, noiseless hydraulic pile jacking machines (Silent Piler), and the press-in construction business utilizing new press-in technologies.

・For 1Q (Sept-Nov) results of FY2020/8 announced on 10/1, net sales decreased by 12.7% to 5.867 billion yen compared to the same period the previous year, and operating income decreased by 66.8% to 435 million yen. Demands for disaster recovery work and disaster prevention and reduction work had continued, but sales declined due to seasonal factors involving preparation for the upcoming intensive order season. In addition, profits decreased due to an increase in personnel costs accompanying the strengthening of business structures.

・For its full year plan, net sales is expected to increase by 11.0% to 36.0 billion yen compared to the previous year, and operating income to increase by 3.2% to 6.9 billion yen. In 2019/10, Typhoon Hagibis caused extensive flood damage through river flooding and embankment collapse. In terms of embankment reinforcement work, company’s “implant embankment” is attracting attention. This is so also from the angle of building national resilience. For its overseas business, Phase 1 quay repair work at Dakar Port in the Republic of Senegal has completed, and is progressing smoothly into Phase 2 within this year.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: