Report type: Weekly Strategy

Hearing of Nominee for next BOJ Governor and situation in Ukraine

The 24th of this month is likely to be an important day for the stock market. First, it is the day when the Diet will hold a policy hearing and Q&A session with Mr Ueda, the nominee for the next BOJ governor. Second, it is exactly one year to the day since the Russian invasion of Ukraine. While the stock market was in a state of increasing deadlock, the closing price of the Nikkei Stock Average Volatility Index (Nikkei VI), also known as the Japanese version of the fear index, began to rise from 14.71 points on 16/2 to the 17 points level on 22/2, just before 24/2.

On the morning of 24/2, after the national holiday on 23/2, Mr Ueda indicated that the BOJ would continue its current monetary easing policy, saying that “the monetary policy being conducted by the BOJ is appropriate”, and stressed the need to basically achieve a 2% inflation rate, saying that the current consumer price increase was not sustainable. In addition, he stated that there was no need to change the wording of the joint statement by the government and the BOJ for the time being. This was perceived by the market as a proactive “dovish” stance with regards monetary easing, and the stock market responded by rising. In the bond market, although trading of newly-issued 10-year JGBs was not concluded in the morning, long-term JGB futures (March contract) with the 10-year JGB as the standard contract reacted with higher bond prices (lower yields), with the morning closing price 21.00 points higher than the previous day.

Trading volume also swelled at the close of trading on 22/2, especially for stocks with large market capitalization. It can be inferred that long-term funds such as pensions are buying at a bargain due to the feeling that fundamentals are underpriced. Furthermore, TSE’s strong request for disclosure by “companies with PBRs (price-to-net-worth ratio) consistently below 1x” from this spring is expected to accelerate expectations of medium-term management plan reviews for stocks with low PBRs. This suggests that for the time being, there is room for Japanese equities as a whole to see a firming up of the market.

The overseas situation is likely to remain a risk factor. While Russian President Vladimir Putin announced in his annual State of the Union address his intention to suspend the nuclear disarmament treaty and increase nuclear forces, US President Joe Biden made a historic visit to the Ukrainian capital of Kiev. There is therefore growing concern that the hardline stance of both sides may prolong and deepen the current state of war. The UN General Assembly’s adoption of a resolution for the immediate withdrawal of Russian troops and peace in Ukraine may lead to stronger economic sanctions against Russia in the future, and there are concerns about the negative impact on European stocks in particular, where major stock indices are near record highs amid growing optimism.

China’s top diplomat, Wang Yi, had visited Russia and met with President Putin. China risk is likely to increase for G7 countries amid the ongoing fragmentation of the international economy, and the importance of India with a neutral stance will increase.

In the 27/2 issue, we will be covering TerraSky (3915), Nippon Paint Holdings (4612), Sumitomo Rubber (5110), and Honda Motor (7267).

TerraSky Corp (3915) 1,943 yen (24/2 closing price)

・Established in 2006. Comprises the solutions business based on the cloud systems of Salesforce and AWS (Amazon Web Service), and the product business that provides cloud services in Japan and overseas as a SaaS vendor.

・For 9M (Mar-Nov) results of FY2023/2 announced on 16/1, net sales increased by 25.6% to 11.405 billion yen compared to the same period the previous year, and operating income increased by 2.4% to 460 million yen. Sales in the Solutions business, which accounts for approximately 90% of sales, increased 29% YoY due to increase in cloud implementation development and cloud migration business. Segment income also increased 13% YoY, absorbing increased expenses caused by aggressive investments.

・Company maintained its full-year forecasts for net sales of 15.646 billion yen (up 24.4% YoY) and operating income of 328 million yen (down 50.1% YoY), but 3Q results had already exceeded the full-year operating income forecast. While growth in the US public cloud market is slowing, the domestic market is expected to continue to benefit from increased corporate digital transformation (DX) demand. Spread of interactive searches such as ChatGPT will also increase the demand for cloud services through the use of artificial intelligence (AI).

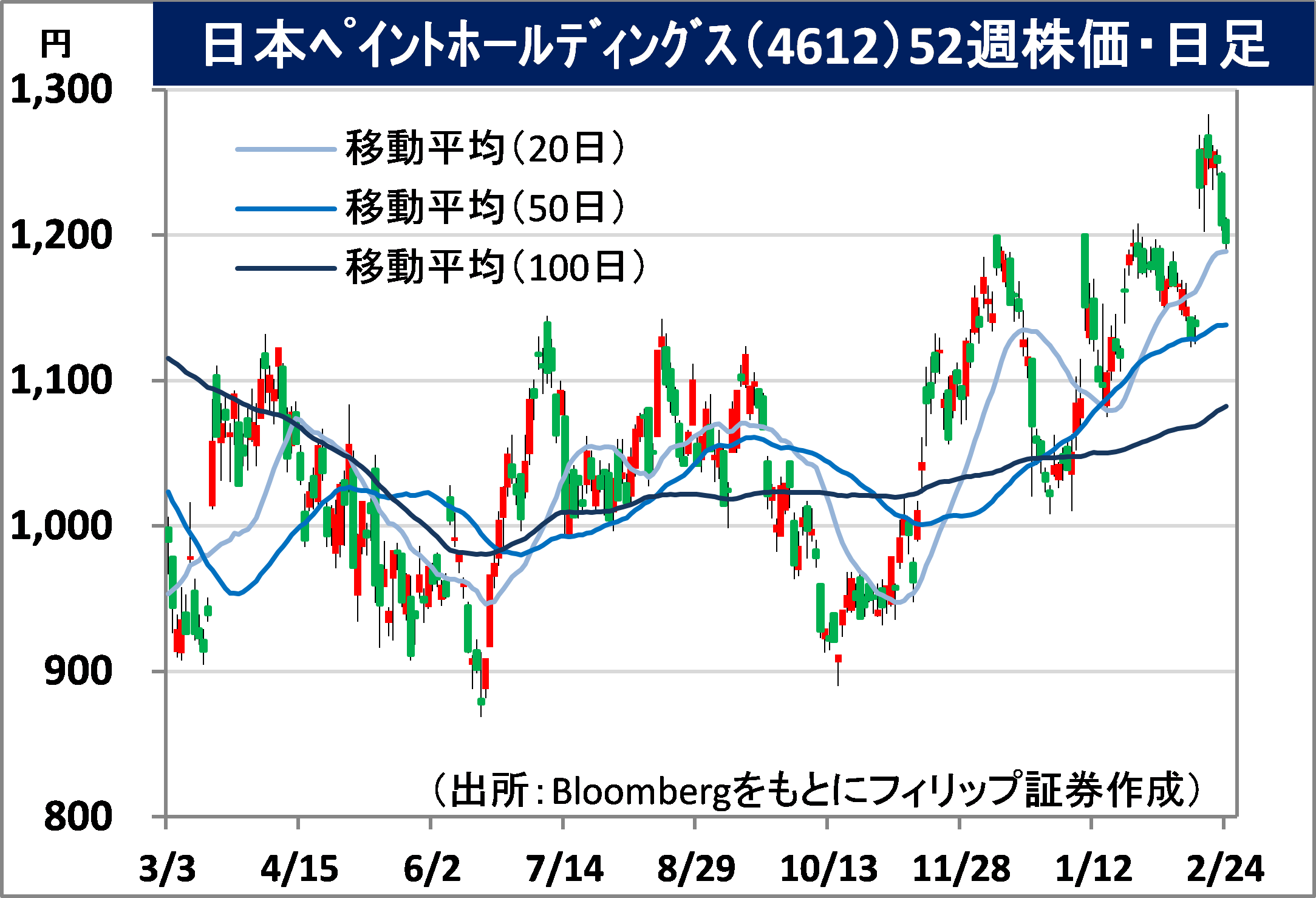

Nippon Paint Holdings Co., Ltd (4612) 1,195 yen (24/2 closing price)

・Comprehensive paint manufacturer founded in 1881 as the first paint and pigment manufacturer in Japan. Nipsea International, a subsidiary of Singapore investment company Wuthelam, is the largest shareholder with 54.5%. Leader in paint industry in Japan and the fourth largest in the world.

・For FY2022/12 results announced on 14/2, net sales increased by 31.1% to 1.309 trillion yen compared to the previous year, and operating income increased by 27.7% to 111.8 billion yen. Acquisition of two European paint manufacturers (Cromology and JUB) as subsidiaries and price increases for general-use paints in China contributed to higher sales. Gross profit margin declined only 0.7 points YoY to 37.1% despite the sharp rise in raw material prices.

・For FY2023/12 plan, net sales is expected to increase by 7.0% to 1.4 trillion yen compared to the previous year, operating income to increase by 25.1% to 144.0 billion yen, and annual dividend to increase by 2 yen to 13 yen. Optimism around the effects of product price increases, especially for construction, a recovery in the automotive market, and an improvement in raw material cost ratio. Based on its scale and strong branding as the largest paint manufacturer in Asia, company plans to become a world-class company through aggressive acquisitions. Focusing on construction sector applications, which are expected to be in more solid demand than automotive applications.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: