| Report type: Weekly Strategy |

“Greeting the Major SQ With an “Extreme Bullish Sentiment”, to Sell on the Vaccine?”

11/12 is a “Major SQ date”, which falls on the 2nd Friday of March, June, September and December where there is an overlapping of the dates for calculating the SQ value (Special Quotation) involving the final settlement of stock index futures and options trading. Originally, with there being the characteristic of the market tending to fluctuate greatly depending on trends of the roll over, which is handed over to the next expiration month, this time round in the U.S. presidential election, with the deadline for each state to certify the election results (8th) and the date for the electoral college of each state to vote for the presidential candidate (14th) around the corner, it is believed that the market will likely fluctuate greatly both upwards and downwards, hence, caution must be exercised.

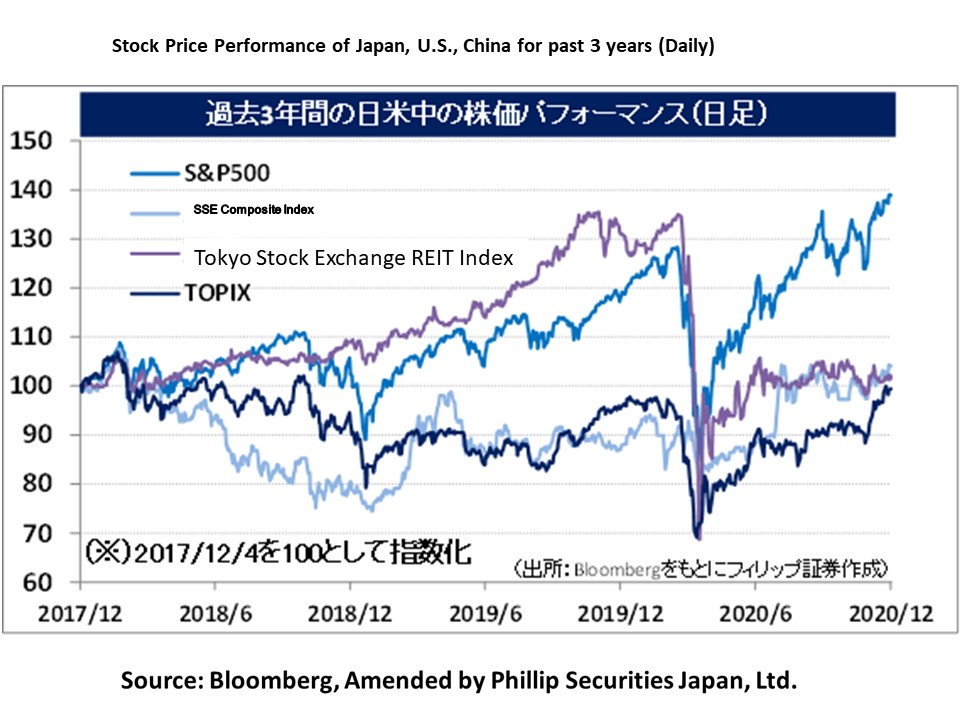

With the trend of rising stock prices across the world growing stronger, on 17/11, strategists from the Bank of America expressed their opinion that based on an investor survey, asset allocation towards stocks is at a high level that was last seen in Jan 2018, and based on the percentage of cash holdings becoming a low that was last seen in Apr 2015, etc., investor sentiment towards stocks is approaching “extreme bullish”, thus it is time to start selling risk assets on the statement, “sell on the news of the vaccine in the coming weeks to months”.

Inoculations for the COVID-19 vaccine jointly developed by the American Pfizer (PFE) and German BioNTech are scheduled to begin in the U.K. as early as 7/12. Also, in the U.S., it is predicted that inoculations for the vaccine will begin as early as 11/12 depending on the U.S. Food and Drug Administration (FDA)’s decision on 10/12 to approve its usage. On the other hand, according to a survey on public opinion by the research company, Gallap & Robinson, even if inoculations for COVID-19 were available for free, only 58% of Americans responded that they would like to be inoculated. The reality that the popularisation of the vaccine being viewed optimistically in the market turning out to be complicated, might become more prominent.

The forecast of the bullish sentiment towards stocks is in relation to the sudden rise in the influx of money to emerging countries. With uncertainty on the transition of the U.S. administration easing and increased money in emerging countries showing more activity, it was said that bonds along with stocks of emerging countries were bought for a record high of 76.5 billion dollars in November this year. In addition to the rise in the commodity market contributing to the stability of the economies of emerging countries, which rely on the export of resources, along with expectations of vigorous fiscal stimulus towards former FRB Chairman, Yellen, who was nominated as a candidate for the Secretary of the Treasury by former Vice President Biden, the continuing trend of the falling USD against currencies of emerging countries also benefits emerging countries by alleviating the burden of debts in USD. In the weekly commentary on 23/11 by the American asset management company, BlackRock (BLK), Japanese stocks remained at underweight while overall Asian and emerging markets except Japan were considered overweight due to them easily benefitting from the greater ability to forecast U.S. trade policies under the next administration.

In the 7/12 issue, we will be covering Digital Media Professionals (3652), Nippon Denko (5563), Toshiba Tec (6588), and Zenrin (9474).

・Established in 2002. Carries out the manufacture and retail of LSI products in addition to developing graphics IP cores and providing semiconductor IP cores integrated in mobile communication devices, automobiles and game machines, etc. to semiconductor and final product manufacturers.

・For 1H (Apr-Sep) results of FY2021/3 announced on 10/11, net sales was 533 million yen and operating income was (191) million yen. Figures from the same period the previous year were not listed due to the consolidated financial statement being created from the 1Q (Apr-Jun) of FY2021/3. Although there was a 3.5 times increase in revenue compared to the same period the previous year in the LSI products business, the decrease in revenue in the IP core license and professional services businesses had affected.

・For its full year plan, net sales is expected to be at 1.5 billion yen and operating income to be at (150) million yen. In addition to having started providing SaaS-based safety driving support cloud services that used Amazon Web Services (AWS) in the automobile safety driving support field, on 30/11, they announced their participation in the U.S. semiconductor giant NVIDIA (NVDA)’s partner program (NVIDIA Partner Network). In addition to the acceleration of the AI business, we can likely look forward to a reinforcement of their business tie-up with NVIDIA.

・Established in 1934 as an alloy manufacturer for steel. It is a group corporation of their principal shareholder, Nippon Steel (5401), and in addition to the manufacture and retail of their mainstay ferroalloy, they expand the functional materials, environment, electricity and other businesses.

・For 1H (Apr-Sep) results of FY2021/3 announced on 10/11, net sales decreased by 26.4% to 39.906 billion yen compared to the same period the previous year, and operating income returned to profit from (1.149) billion yen the same period the previous year to 4.613 billion yen. Although the decrease in crude steel production quantities in regions excluding China affected the decrease in revenue, raw material costs decreased due to a devaluation of book prices from an inventory asset valuation conducted at the end of last year.

・For its full year plan, net sales is expected to decrease by 29.1% to 50 billion yen compared to the previous year and operating income to return to profit from (5.572) billion yen the same previous year to 5 billion yen. The company holds the top spot in Japan for manufacturing hydrogen occlusion alloys, which are able to occlude and discharge hydrogen, and is the largest supplier for nickel-metal hydride batteries for hybrid cars. They are also carrying out a manufacturing consignment from Sumitomo Metal Mining (5713) for materials for the positive electrode of lithium-ion batteries.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: