Report type: Weekly Strategy

”Gazing at the “three shifts” relating to a weak dollar, commodities and emerging economies”

There are only a few days left in 2020 during which Covid-19 struck. As of 25/12, the Nikkei Average’s low for this year was 16,358 points, set on 19/3, and its high was 26,905 points, set on 21/12. The index fluctuated widely, at 5,273 points above and below the average of 21,631 points. The price of 21,631 points is between the low of 21,529 points on 15/6 and the low of 21,710 points on 31/7, and it is likely to function as a turning point in the price marking the bottoming out of the market in the event of a major decline in the future. Furthermore, the net asset price per share of 22,600 yen, calculated based on a weighted average PBR (price-to-book-value ratio) of 1.18 times as of the closing price on 24/12, is a price at which we can expect the lower limit to be reached if the market were to be oversold during a market adjustment phase.

I would like to mention “three shifts” as keywords when looking at the stock market in the coming year: (1) a risk-on weaker dollar shift as a result of the Fed’s monetary easing, (2) a commodities shift where commodity prices will be in the spotlight, and (3) an emerging markets shift where quantitative easing money flows into emerging markets as the dollar weakens.

The “shift to a weaker dollar” will create a structure and trend in which the expansion of the Fed’s balance sheet will reduce the supply of quantitative easing money in the US, making it more likely to flow to Japan and emerging economies instead. While the Japanese market had been playing the role of supplying quantitative easing money through the BOJ’s unconventional monetary easing since 2013, it is now suggested that it will be on the receiving end of quantitative easing money. US stocks have outperformed Japanese stocks since the Lehman shock, but the gap may narrow from next year.

In the “commodity shift,” prices of non-ferrous metals and precious metals are expected to soar as electric vehicles (EVs) and green energy infrastructure construction are promoted to reduce greenhouse gas emissions. In addition, the frequent occurrence of abnormal weather and natural disasters due to global warming, as well as changes in income levels, consumption and dietary habits in emerging countries with large and as yet growing populations, may lead to water and food shortages, which in turn may lead to higher grain prices. These factors will make it easier for overall commodity prices to soar.

A “shift to emerging markets” could, as a result of tighter antitrust laws and a weaker US dollar, see a shift from a structure in which market capitalization that is currently skewed toward a small number of major US high-tech companies, such as GAFA, to one in which investment funds flow to emerging markets with relatively low income levels. As a result, the income gap between developed and emerging markets will be narrowed. During the BRICs (Brazil, Russia, India and China) boom from 2000 to 2008, Russian stocks performed particularly well against the backdrop of soaring oil prices, but the next boom in emerging economies is likely to be led by countries with large populations, such as India, African countries and Indonesia.

In the 28/12 issue, we will be covering Healthcare & Medical Investment Corp (3455), IG Port (3791), Mitsubishi Materials (5711), and Toyota Tsusho (8015).

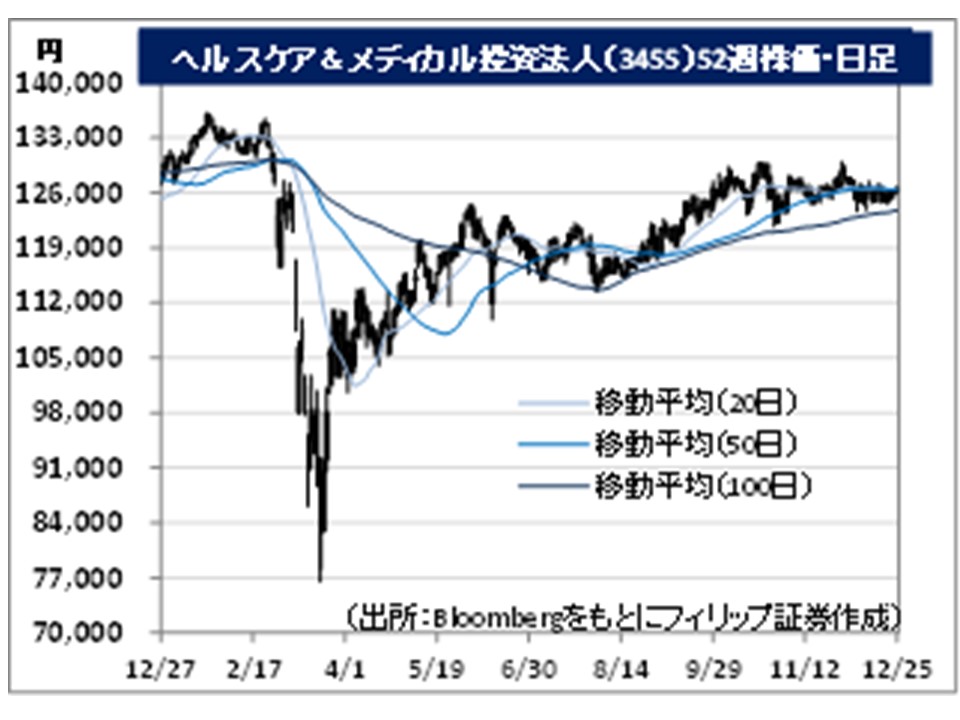

・A healthcare-focused J-REIT that has Sumitomo Mitsui Banking Corp and NEC Capital Solutions as major sponsors in addition to Ship Healthcare Holdings, which engages in the nursing care business. Acquired a J-REIT-first hospital asset in 2017/11.

・For the FY2020/7 (Feb-July) results announced on 15/9, operating revenue increased by 0.5% to 2.023 billion yen compared to the previous period (FY2020/1), operating income decreased by 2.8% to 1.072 billion yen, and distribution per unit decreased by 2.4% to 3,240 yen. Acquired two properties (total acquisition price: 1.456 billion yen): “Verde Hotaka” and “Sunny Life Kamakura”. The number of properties held at the end of the period was 35, and the occupancy rate was 100%.

・For FY2021/1 plan (2020/8-2021/1), operating revenue is expected to increase by 1.7% to 2.058 billion yen compared to the previous period (FY2020/7), operating income to decrease by 0.8% to 1.063 billion yen, and distribution per unit to decrease by 1.1% to 3,205 yen. The annual distribution yield (based on the closing price on 24/12) based on the company forecast for FY2021/7 is 5.08%. Amidst increasing uncertainty in the real estate market, particularly for commercial facilities and hotels, due to the Covid-19 pandemic, the corporation has concluded fixed-rent, long-term lease agreements with the facility operators.

・Founded in 1987 as an animation production company (IG Tatsunoko). Under its umbrella are animation production companies like Production I.G., Wit Studio, and Signal MD, as well as hit productions like “Attack on Titan”.

・For 1Q (Jun-Aug) results of FY2021/5 announced on 9/10, net sales decreased by 42.9% to 1.127 billion yen compared to the same period the previous year, and operating income fell to minus 150.0 billion yen from a positive 171 million yen in the same period of the previous year. In addition to the growth in the copyright business, the publishing business was also strong due to demands for comic books as a result of stay-at-home routines, but the lack of major sales in the video production business had a negative impact on performance.

・For its full year plan, net sales is expected to increase by 6.2% to 9.621 billion yen compared to the previous year, and operating income to decrease by 15.6% to 238 million yen. The popular movie, “Fate/Grand Order,” which had been postponed due to the Covid-19 pandemic, will be released nationwide this December. The sequel will be released in the spring of 2021. Media mix development linked with smartphone apps is also going well. It is expected to contribute to full-year results, including the demand for e-comics from those staying at home. Copyright business, such as design cans for “Attack on Titan”, is also strong.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: