Report type: Weekly Strategy

“Foreign Money Showing a Positive Attitude Towards Japanese Stocks”

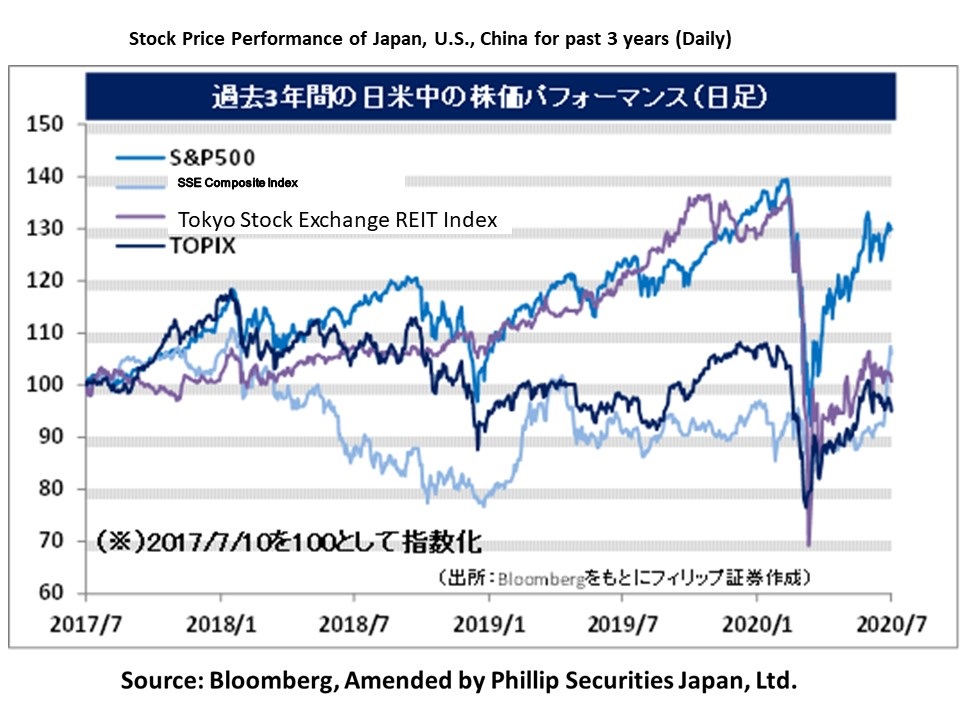

On 6/7, 2 companies from the U.S. showed a positive attitude towards investing in Japanese corporations. First, the world’s largest asset management, BlackRock, revised their stance to Japanese stocks upwards in their weekly commentary dated 6/7. Although there was mention in the past of the possibility of upgrading Japanese stocks, it was upgraded by 1 rank from underweight previously to neutral. The main reason is “the adoption of strong fiscal policy and public health measures, which show possibility in rapid normalisation”. In addition, it also brought up the close relation with the recovery of China’s economic climate due to it being China’s trade competitor country. In other regions, due to expectations of policies and a restart of the economy in the Euro area, it was upgraded by 2 ranks from underweight to overweight. On the other hand, the U.S. was downgraded by 1 rank from overweight to neutral, and emerging markets were downgraded by 1 rank from neutral to underweight. Furthermore, in terms of each factor, attention has been on the upgrading of value investments by 1 rank from underweight to neutral. We can infer the presence of investment money attempting to shift from gross investment of U.S. corporations such as FAANG stocks, etc. towards value stock investments focused on the undervaluing of the net asset value of Japanese corporations.

Next, major U.S. investment company The Blankstone Group predicts a recovery in demand for foreign tourists visiting Japan (inbound) after the COVID-19 crisis, and clarified their intentions in considering investment in Japan’s tourism-related corporations. Demand which vanished from the spread of infection is presumed to be able to recover by a certain extent in the next 2 to 3 years, and along with the pharmaceutical / medical field and logistics services, it is regarded as a part of the 3 fields on close watch for investment in Japan. Just at that moment on 10/7, the Ministry of Land, Infrastructure, Transport and Tourism announced that they would be bringing forward the launch of the “Go To Travel” which was targeted for early August, which would subsidise domestic travel costs, and support would be applicable for travel from 22/7 onwards. We can likely expect this to have the effect of supporting movements of foreign money which have their eye on investment in Japan’s tourism-related corporations.

For the present Japanese stock market, with the Nikkei average at a growing standstill at around 22,500 points, in addition to China’s Manufacturing Industry and Service Industry PMI for June and the U.S. ISM Manufacturing and Non-Manufacturing Index being strong, also in Japan, following the announcement of ITOCHU (8001) carrying out the TOB for Family Mart (8028), with rising expectations on TOBs (takeover bid) for subsidiaries of other parent-subsidiary listings, etc., there has been a gradual increase in positive factors on stock prices. Due to the unclear impact of the COVID-19 calamity, perhaps there may be an increase in movements to retain profits of subsidiaries or cash within the corporate group. The start of the Apr-Jun term financial results for major U.S. corporations from 13/7 could also become a factor that will likely stimulate the Japanese stock market.

In the 13/7 issue, we will be covering Toda (1860), Nitto Denko (6988), Mitsubishi Shokuhin (7451), and AEON Financial Service (8570).

・Founded in 1881. Their main businesses are the domestic construction business, the domestic civil engineering business, the investment development business, the new frontier business (including the floating wind turbine business) and the overseas business, and expands other PFI businesses, etc. related to each business.

・For FY2020/3 results announced on 29/5, net sales increased by 1.6% to 518.683 billion yen compared to the previous year and operating income increased by 2.1% to 35.243 billion yen. Despite the number of construction orders decreasing by 17.5% and the number of civil engineering orders decreasing by 3.6%, net sales involving the investment development business increasing by 34.1% and segment operating income increasing by 2.1 times contributed to the increase in income and profit.

・For FY2021/3 plan, net sales is expected to decrease by 5.6% to 445 billion yen compared to the previous year and operating income to decrease by 26.3% to 24 billion yen. After progressing with the suspension and abolishment of coal-fired power generation which came under heavy criticism across the world, the government has begun creating rules with a priority on the application of renewable energy. With offshore wind power generation regarded as promising, the company has built a floating wind turbine facility off the coast of Goto in Nagasaki Prefecture. We can likely expect an increase in efficiency in offshore wind power generation installation work due to the company’s technology.

・Established in 1918. Manages 4 other departments which handle industrial tapes, which deal with core function materials, etc., optronics, which deal with information function materials, life sciences regarding medical-related materials and polymeric separation membranes, etc.

・For FY2020/3 results announced on 27/4, sales revenue decreased by 8.1% to 741.018 billion yen compared to the previous year and operating income decreased by 24.8% to 69.733 billion yen. The decrease in the number of units manufactured in the automobile market and the suspension in operation following the spread of COVID-19, etc. affected, which led to a decrease in revenue across all 4 departments. Furthermore, all 4 departments had a decrease in operating income and an increase in operating deficit.

・Although the FY2021/3 plan is undecided due to the unclear impact of the COVID-19 calamity, for 1H (Apr-Sep) results, sales revenue is expected to decrease by 7.5% to 350 billion yen compared to the same period the previous year and operating income to decrease by 14.8% to 35 billion yen. The company supplies about 70% of reverse osmosis (RO) membranes which recycle sewage water to drinkable water in Singapore, who imports water from Malaysia. The company’s future policy is to expand their environment and energy field pertaining to water purification in India and South America.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: