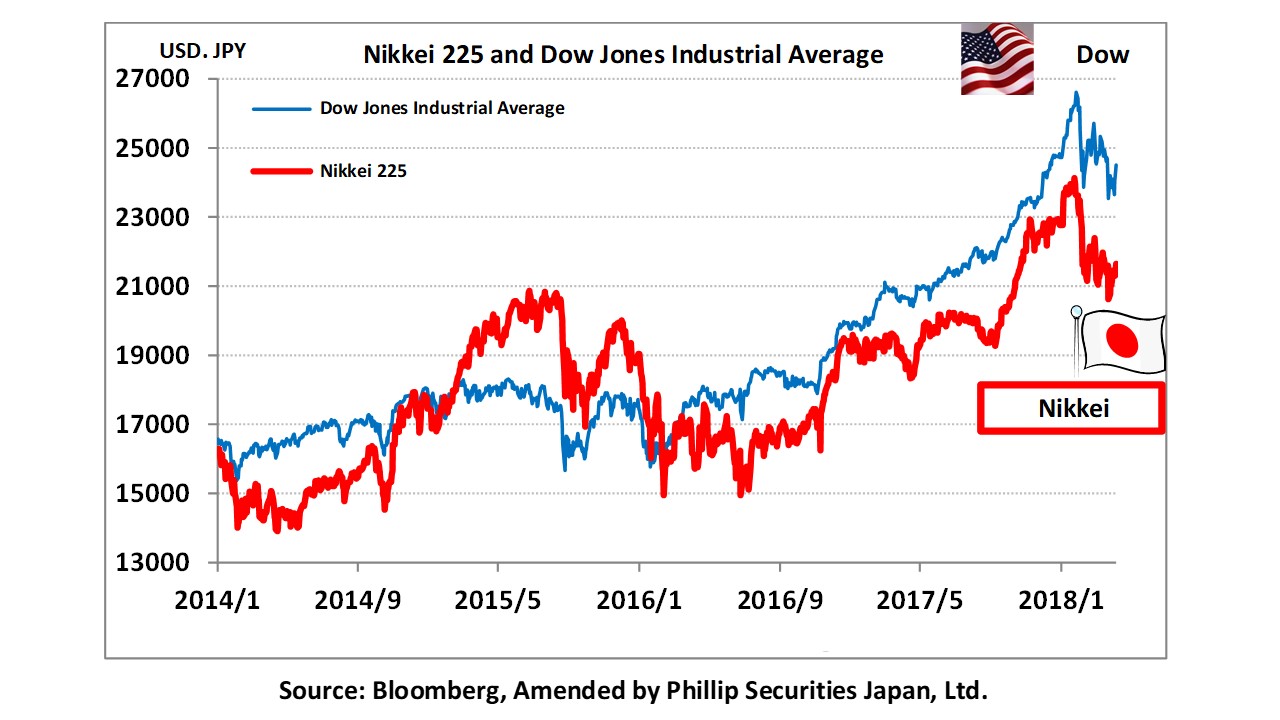

“Faint hope of foreign investors continuing to buy?”

As of 20th April, the Nikkei Average had fallen by 2.65% since the beginning of the year, remaining in negative territory. However, it had risen 3.30% since the beginning of April and is recouping losses. Markets had been turbulent in February and March, but the Nikkei Average managed to keep above Yen20,000. BOJ’s purchase of ETF in March was Yen833.3 billion per month, which was the highest ever recorded, representing a buying support.

Subsequent to that, foreign investors staged two continuous weeks of net buying, with Yen443.1 billion in the first week of April (Yen158.4 billion yen of spot trades + Yen284.7 billion in futures), and Yen572.9 billion in the second week (Yen84.5 billion in spot trades + Yen488.4 billion in futures). There were net selling of Yen9.4 trillion in spots / futures from the second week of January to the fourth week of March (▲Yen3.1 trillion in spot trades + ▲Yen 6.3 trillion in futures). However, the spot trades for the net purchase amount is small compared to that for the net sales amount. Buyback of futures by short-term speculators such as hedge funds may also have played a role. We need to continue to pay attention to the behavior of foreign investors.

There was agreement during the Japan-US Summit on 18-19 April to continue to exert “maximum pressure” on the denuclearization of North Korea. In terms of trade policy, there was agreement to establish a new trade agreement while not excluding Japan from import restrictions on iron and aluminum. Economic & Finance Recovery State Minister Motegi and USTR Lighthizer will proceed with practical consultation. While agreement was reached in the trade talks, PM Abe commented that “the return of the US to the TPP will benefit both Japan and the US”, and indicated that the FTA (Japan-US Free Trade Agreement) was not in his mind. On the other hand, President Trump said that “bilateral trade agreement is desirable”, and indicated his desire to negotiate including FTA. Indeed, we again discern a big gap between the expectations of both countries.

President Trump could be striving to reduce the US deficit as he faces the mid-term elections. As Japan is the third largest trade deficit country after China and Mexico, there seems to be great dissatisfaction against automobiles, which account for about 30% of imports. Going forward, we need to pay attention to future activities, including remarks on

currency exchanges etc. Currently, owing to concerns about slowing demand for smartphones, semiconductor stocks centering on semiconductor manufacturing equipment are being sold. Nevertheless, we are expecting good results from high-tech companies. We should examine performance results and narrow down investment targets accordingly.

In the 4/23 issue, we will be covering Toda Corporation (1860), Tsugami Corporation (6101), MODEC (6269), Daifuku (6383), Fanuc (6954) and Kintetsu Department Store (8244)

Selected Stocks

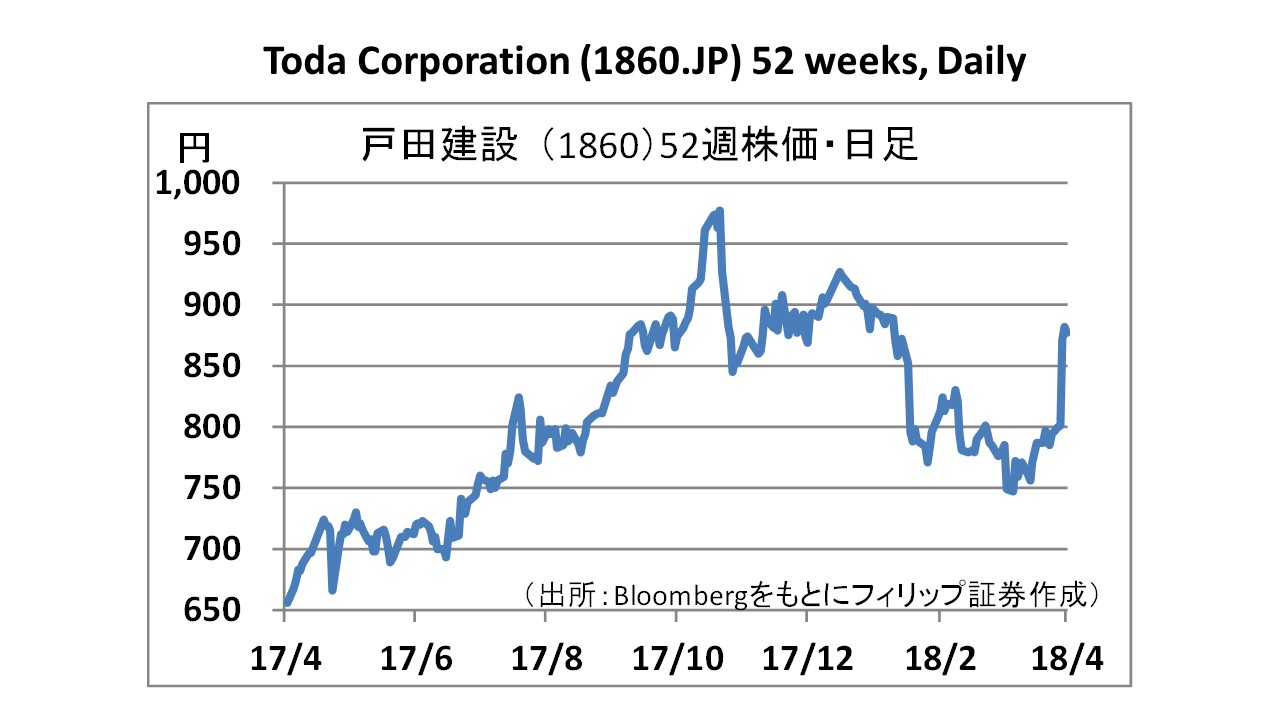

Toda Corporation (1860)

・Established in 1881. Involved with construction business, civil engineering and real estate business etc. Strengths in medical & welfare facilities, educational facilities, urban & transportation infrastructure, disaster prevention and conservation facilities, etc. Constructed the following in recent years: Marunouchi OAZO, W Comfort Towers, Konohana Dome, hospital affiliated to the Medical Dept of Tokai University, Minatomirai Line Bashamichi Station, and Yamadagawa Dam.

・For 3Q (Apr-Dec) of FY2018/3, net sales reduced by 5.9% to 289.657 billion yen compared to the same period the previous year, operating income increased by 4.8% to 20.31 billion yen, and net income decreased by 19.5% to 16.358 billion yen. Increase in operating income even with reduction in net sales through reduction in construction completion amount and thorough execution of orders with emphasis on profitability. Net income decreased due to increase in corporate tax burden.

・Company has revised FY2018/3 performance upwards. Net sales is expected to increase by 1.2% to 428 billion yen (original plan 421 billion yen) compared to the same period the previous year, operating income to increase by 22.0% to 30.5 billion yen (original plan 24.8 billion yen), and net income to increase by 39.7% to 25.4 billion yen (original plan 19.8 billion yen). Operating income is expected to hit new records thanks to robust private construction demand.

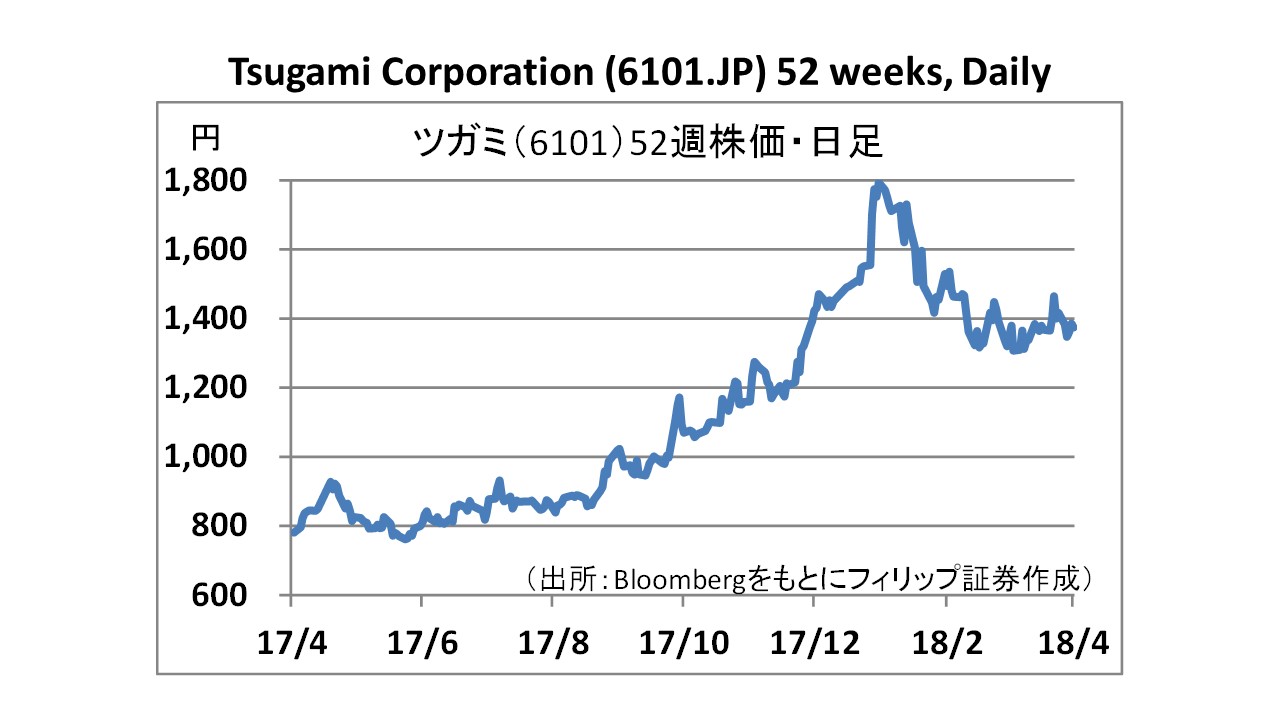

Tsugami Corporation (6101)

・Comprehensive manufacturer of compact ultra-precision machine tools established in 1937. Development, design, manufacture and sales of precision machine tools (mother machines), such as precision automatic lathes, precision grinding machines, precision machining centers, precision thread and form rolling machines, etc, used for processing components of various products. Has established an integrated production system that enables the company to carry out development, design, production and inspection all by itself.

・For 3Q (Apr-Dec) of FY2018/3, net sales increased by 38.6% to 42.269 billion yen compared to the same period the previous year, operating income increased 2.4 times to 4.976 billion yen, and net income increased by 48.7% to 3.14 billion yen. Sales of automatic lathes for the automotive industry had been strong.

・Company has revised FY2018/3 performance upwards as market conditions continue to be favorable. Net sales is expected to increase by 40.3% to 57.6 billion yen (original plan 52.0 billion yen) compared to the same period the previous year, operating income to increase by 2.3 times to 7.0 billion yen (original plan 6.0 billion yen), and net income to increase by 59.7% to 4.2 billion yen (original plan 3.6 billion yen). FY2018/3 full year results expected on 5/11.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: