Report type: Weekly Strategy

Expectations on the Chinese Economy and Lifting the Ban on Group Tour Travel to Japan, the “Herd Mentality” Is Key

As stated in last week’s issue (27th February 2023), “trading volume swelled mainly in stocks with large market capitalization at the time of the end of trading on 22/2. We can surmise that buying the dip occurred due to a sense of undervaluement in the fundamentals aspect for long-term funds such as the pension”, and the Nikkei average rebounded at the bottom of the dip at the closing of 22/2, and rose to the 27,900 point level on the 3rd.

A large contributing factor for this was likely expectations on the recovery of China’s economy. The Purchasing Managers’ Index (PMI) for February announced on the 1st by the National Bureau of Statistics of China increased by 2.5 points compared to the previous month to 52.6, which became a high level last seen in April ’12. For the Caixin/S&P Global, the service sector for February announced on the 3rd at 55.0 also rose by 2.1 points compared to the previous month. This indicates that demand is recovering due to lifting the zero-COVID policy. There are rising expectations that a strong message will be delivered regarding China’s economic policy in the Chinese People’s Political Consultative Conference starting on the 4th and the National People’s Congress starting on the 5th. Even if the Hong Kong dollar were to maintain the U.S. dollar peg system, there will likely be a need to suppress the widening difference between the U.S. interest rate by increasing the demand for funds.

The Japanese government has switched its COVID-19 border control measures for China to random sampling testing for the testing of all entrants to Japan via direct flights from Mainland China. The Chinese government lifted the ban on overseas group tour travel to 20 countries on 6/2. We can consider it to be a hurdle less towards the inclusion of Japan. The lift on the ban on overseas group tour travel from China has the potential of becoming a great benefit towards a recovery to a pre-COVID state and an increase in inbound tourism consumption, and it could be regarded as a starting point on the track from a recovery in the Japanese economy to the Bank of Japan correcting the large-scale monetary easing.

Dai Nippon Printing (7912), which rocked the market by announcing on 9/2 their basic policy on the next mid-term management plan that aims for “a shareholders’ equity ratio (ROE) of 10% and a P/B ratio (price-to-book ratio) of over 1 times”, plans to hold a “seminar on the summary of the new mid-term management plan” for investors and analysis on the 9th, which will be attended by the company’s president. Milling, oil and fat giant Showa Sangyo (2004) also announced their “23-25 mid-term management plan” on 24/2, which states that their ROE for FY2025 will increase by 4 points compared to the FY2022 forecast to over 7.0%. As such, there has been a succession of movements responding to the strong call for disclosure carried out by the TSE for “companies having a consecutive P/B ratio of less than 1 times”, which is to be implemented this Spring. Ajinomoto (2802), which had its P/B ratio rising to approximately to 3 times, also released its mid and long-term management plan. It said to raise its ROE for FY2025 to 18%, an increase by 7 points compared to the FY2022 forecast, and to introduce “progressive dividends” which will increase the amount / maintain dividends without a dividend reduction. With the good side of the “herd mentality” in Japanese enterprises becoming apparent, an increase in the number of enterprises carrying out similar initiatives could mean the Nikkei average getting closer to exceeding a “big mark”.

In the 6/3 issue, we will be covering The Nippon Road (1884), Golf Digest Online (3319), Sakura Internet (3778), and Sankyo Tateyama (5932).

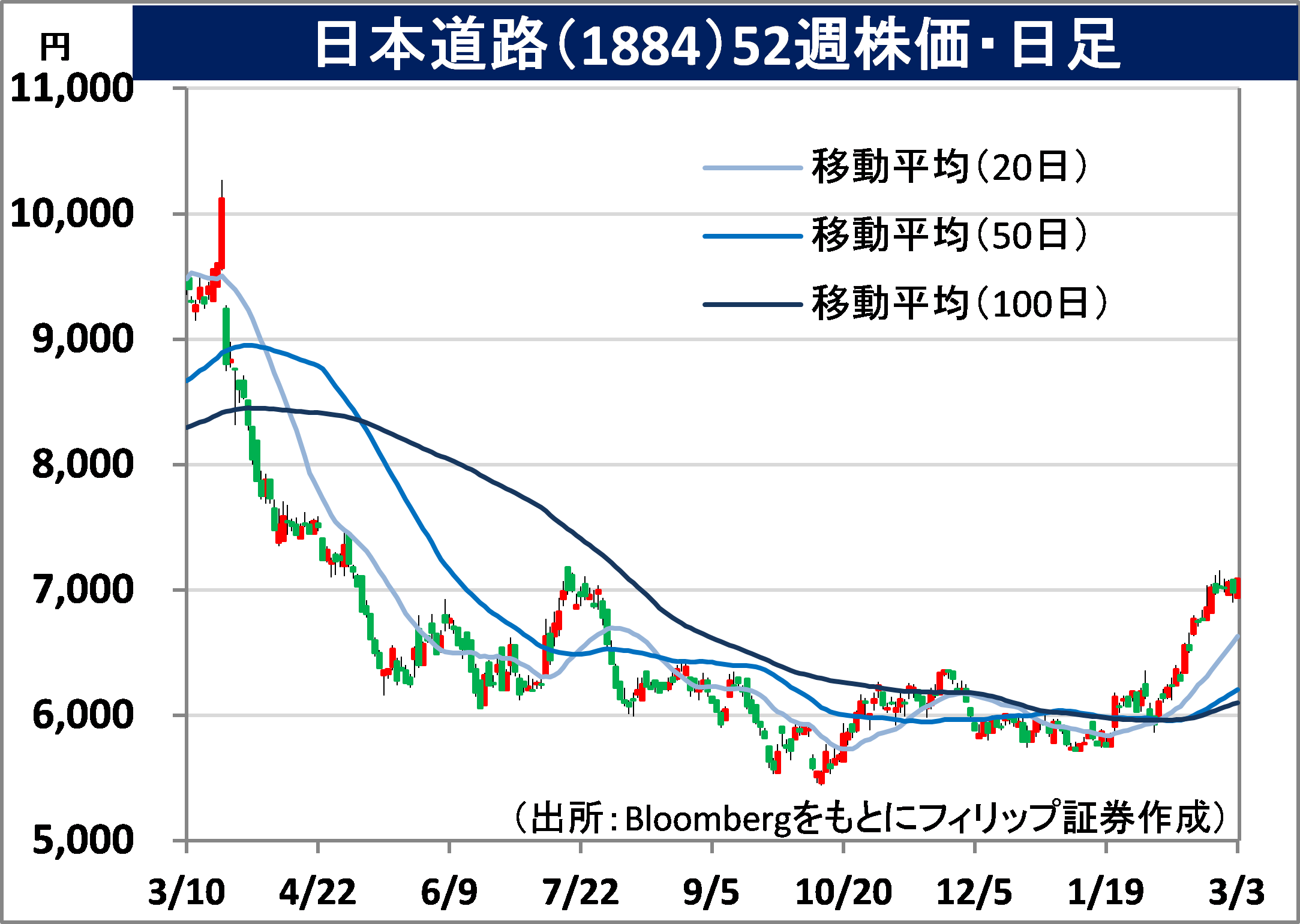

The Nippon Road Co., Ltd. (1884) 7,090 yen (3/3 closing price)

・Founded as Nihon Bitumars Hoso Kogyo in 1929. A subsidiary of the general contracting giant Shimizu Corporation (1803). Its main businesses are the construction business where coating works is its main, and the manufacturing and retail business involving asphalt mixture/emulsion and other coating materials.

・For 9M (Apr-Dec) results of FY2023/3 announced on 31/1, net sales decreased by 1.2% to 113.875 billion yen compared to the same period the previous year and operating income decreased by 44.5% to 3.446 billion yen. Orders received for works was strong for both government offices and private, which increased by 5.7% to 95.416 billion yen. For construction, there was a decrease in sales and income, and for manufacturing and retail, there was an increase in sales and a decrease in income. Soaring raw material and energy prices had affected the profit aspect.

・Company revised its full year plan downwards. Net sales is expected to increase by 1.0% to 158 billion yen compared to the previous year and annual dividend to remain the same at a 30 yen dividend reduction to 180 yen, however, operating income is to decrease by 32.9% to 5.5 billion yen (original plan 7.7 billion yen). The company is developing solar panels embedded in pavements and parking lots. They are aiming to retail to municipalities in FY23. Also, their P/B ratio at the closing on the 2nd was 0.65 times. Their parent company’s P/B ratio was also 0.66 times, and there will likely be a need for their corporate group as a whole to free themselves of a low P/B ratio.

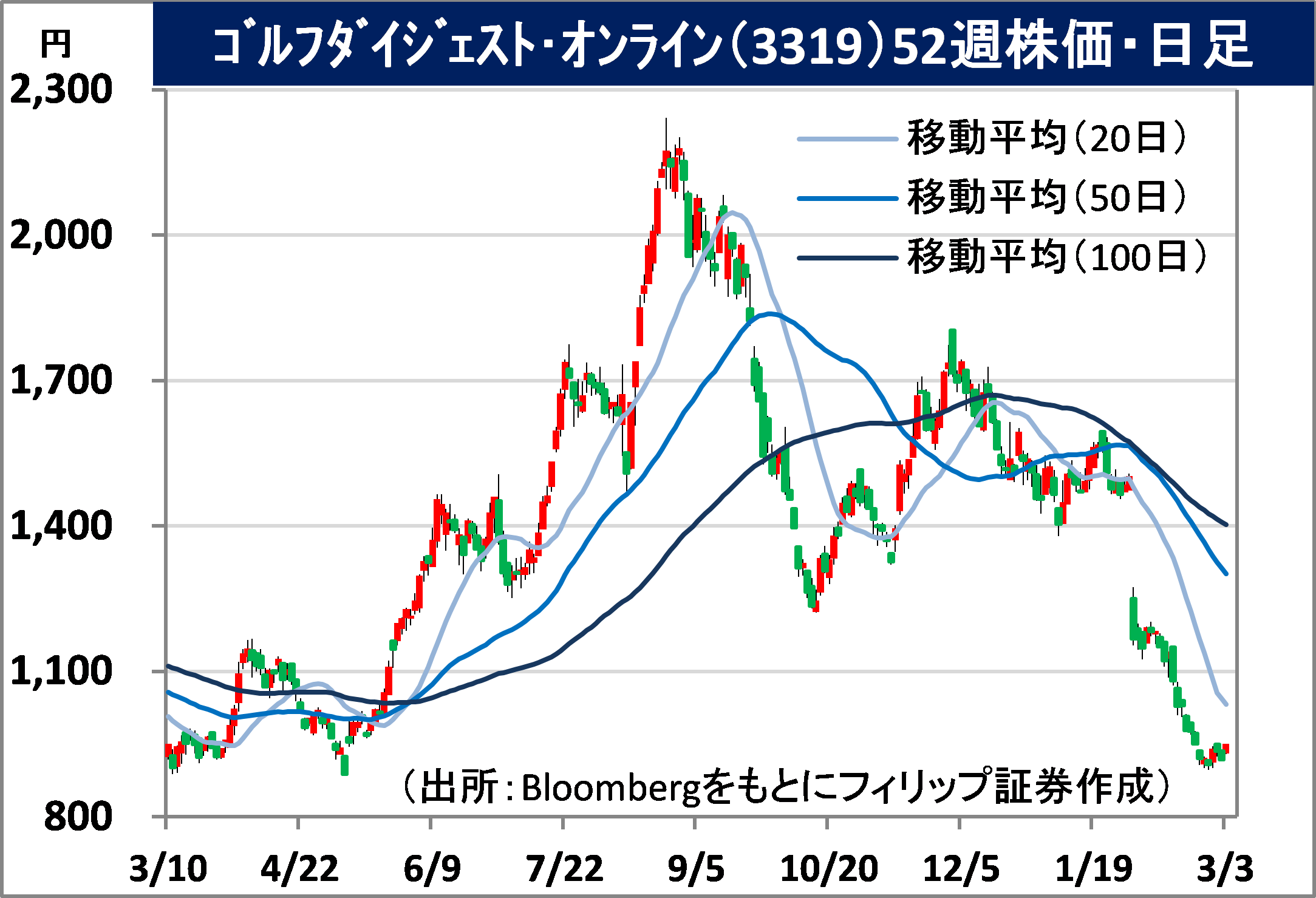

Golf Digest Online Inc. (3319) 948 yen (3/3 closing price)

・An IT services enterprise specializing in golf that established in 2000. Operates the “overseas business” involving golf-related business development, and the “domestic business” involving golf supplies retail, etc., golf course reservations, advertising and indoor lesson studio operation.

・For FY2022/12 results announced on 14/2, net sales increased by 16.4% to 46.09 billion yen compared to the same period the previous year and operating income decreased by 30.3% to 1.189 billion yen. As a result of strong golf demand in the overseas business, the addition of directly managed stores contributed to an increase in revenue. The acquisition of additional equity of their consolidated subsidiary the American GOLFTEC as well as the acquisition of the SkyTrak business involving a golf trajectory measuring machine have led to a decrease in operating income.

・For its FY2023/12 plan, net sales is expected to increase by 15.0% to 53 billion yen compared to the previous year, operating income to increase by 72.3% to 2.05 billion yen and annual dividend to remain unchanged at 9.50 yen. For the domestic business, net sales is expected to increase by 9% to 30 billion yen, EBITDA to increase by 19% to 3.15 billion yen, whereas for the overseas business, net sales is expected to increase by 24% to 23 billion yen and EBITDA to increase by 88% to 2.65 billion yen. With the increasing golf population in the U.S., the number of off-course golfers exceeded those on-course in ’22.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: