Report type: Weekly Strategy

Expectations of a Level Adjustment from a Revision of Low PBR Stocks

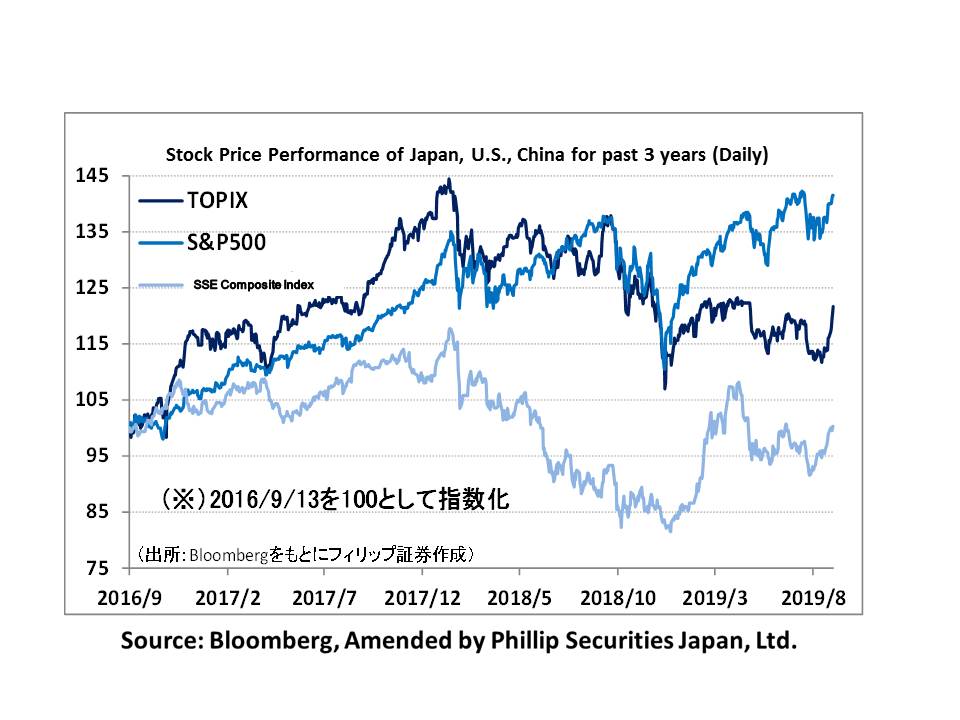

Continuing with the steady pace from the latter half of last week onwards, the Japanese stock market in the week of 9/9 saw the Nikkei average with a 9-day winning streak compared to the previous day up to 13/9. Although on 13/9, the SQ value of the Nikkei average involving the final settlement of futures and options for September was around 21,981 points (provisional figures), the Nikkei average saw strong developments by marking the high price of 22,010 points in its afternoon session, which was last seen since 7/5. As mentioned in last week’s issue (9th Sep 2019 issue), the Nikkei average rose sharply in September in the past 2 years, and currently shows the same outcome for this year as well. The current rise in stock prices are not only due to foreign factors, such as the US-China trade issue, etc., but are also greatly influenced by domestic factors.

Firstly, in the US-China issue, towards the cabinet-level trade talks between both the US and China scheduled to commence in October, on 11/9, the list of US products to be excluded from the additional 25% tariffs on China was officially announced, and as a result, US President Trump announced that the invocation of the 30% tariff hike sanction on 250 billion dollars’ worth of Chinese products would be postponed by 2 weeks to 15/10. Then, on 12/9, it was declared that the Chinese government would be resuming procedures to import US agricultural produce. The opposing parties of the US and China in the trade friction issue showing an actual stance towards a compromise has brought about a “risk-on” state with funds flowing into the global stock market. Furthermore, on 12/9, the European Central Bank resumed their no-deadline quantitative easing policy, and the decision of the interest rate cut when banks deposit surplus funds into the central bank also played a part in contributing to the risk-on market.

In terms of domestic factors, the announcement of the capital and business tie-up between SBI Holdings (8473) and Shimane Bank (7150) on 6/9 has served as a positive influence. In addition to Shimane Bank receiving investment from SBI, the cooperation in the retail of financial products, etc., marks SBI’s first step in their plan that boasts to cooperate with nationwide local banks. The Financial Services Agency, who hopes that SBI will enhance the credit of local banks facing the predicament of a shrinking regional economy and take over their regeneration, has expressed their stance in supporting the plan. Local banks are neglected, seen as typical cheap stocks with their BPS (net assets per stock) significantly lower than their stock prices, and have been pushed back by the fall in stock prices following the downturn. Due to expectations of an expansion in the capital and business tie-up, the stocks of local banks will serve as an ignition point where buyers will spread to bank and securities stocks, and then we can begin to see signs of increased buying on overall low PBR (price-to-book ratio) stocks. It may be approaching the right time for a level adjustment and a revision to the overall market from the aspect of asset value in addition to business performance.

In the 17/9 issue, we will be covering Marudai Foods (2288), Nippon Parking Development (2353), Tokyo Century (8439), SBI Holdings (8473), Japan Exchange Group (8697) and Saison Information Systems (9640).

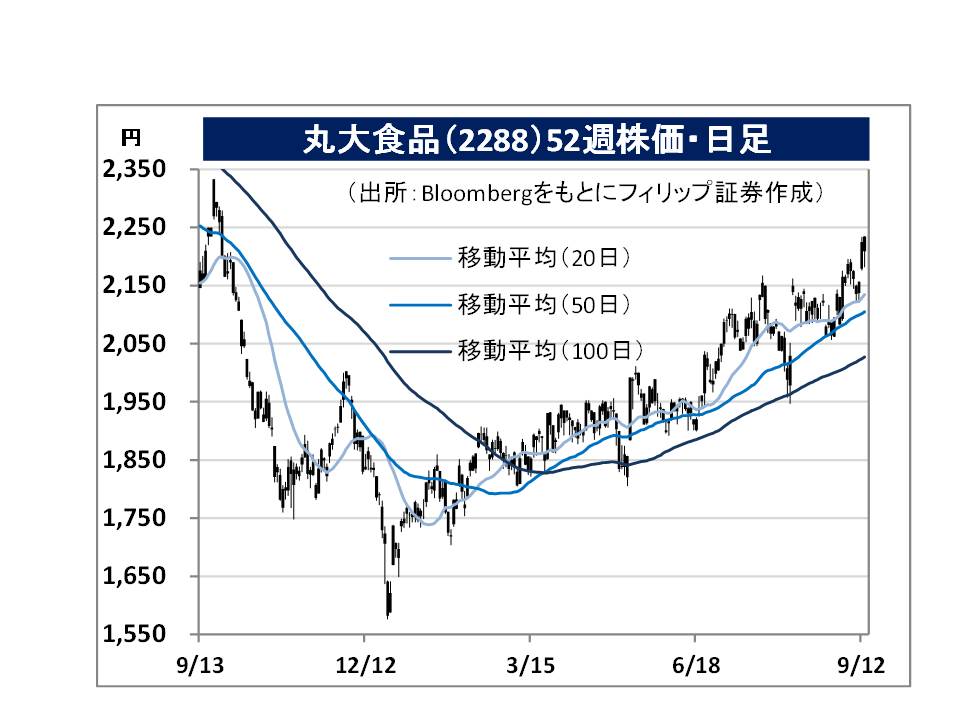

・Founded in Osaka in 1954. In addition to carrying out the processed food business involving the manufacture and retail of various cooking processed food, ham and sausages, and the meat business involving the processing and retail of meat, company also conducts services such as the insurance agency business related to those, etc.

・For 1Q (Apr-Jun) results of FY2020/3 announced on 6/8, net sales increased by 4.5% to 61.393 billion yen compared to the same period the previous year, and operating income increased by 2.8 times to 1.431 billion yen. Despite their mainstay ham and sausages department and the meat business decreasing in revenue, a significant increase in cooking processed foods such as their retort pouch curry, “Sundubu” and “Salad Chicken” range, etc., have led to an increase in both sales and profit.

・For its full year plan, net sales is expected to increase by 2.9% to 250 billion yen compared to the previous year, and operating income to increase by 55.3% to 3.5 billion yen. As a plan to transform their business structure by reinforcing their cooking processed foods, the company established a new factory for convenience stores in the previous year to counteract labour shortages. Good results from these strategies have already shown in the form of a profit increase in the 1Q. In addition to shareholder incentives, their positive attitude towards a return to shareholders, such as from their announcement on 26/8 to carry out a stock buyback, etc. is also likely to be highly rated.

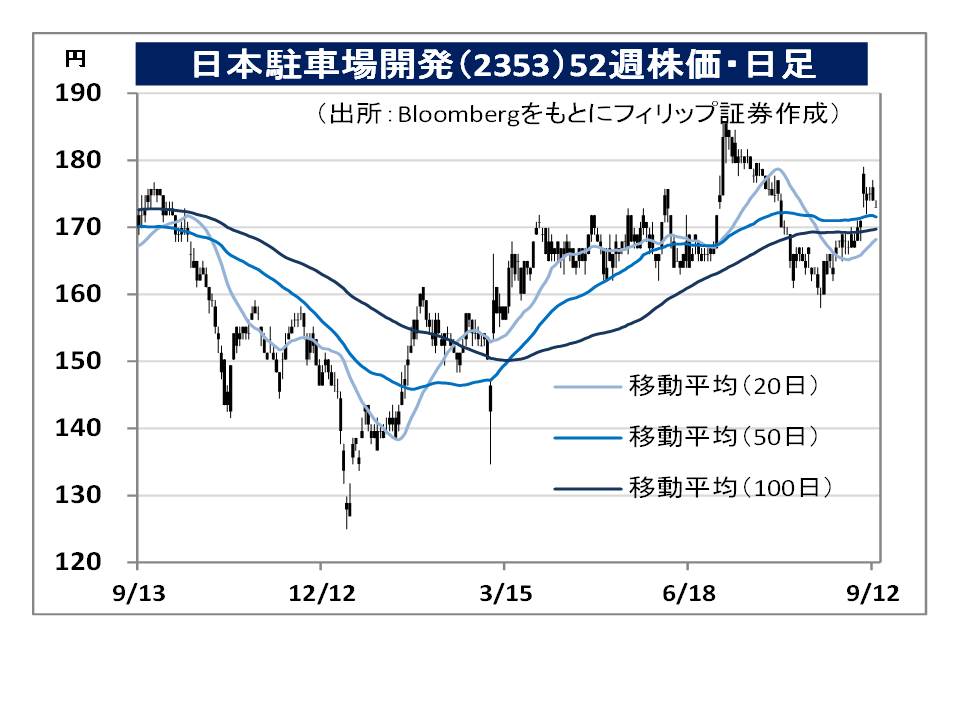

・Established in 1991. Expands the directly-managed business, effectively utilises non-operating parking spaces focusing on the consulting related to parking spaces, company also expands the leasing business entices excellent customers to non-operating parking spaces, the management business that carries out parking space management on behalf, as well as the VA services business which carries out due diligence and renewal consulting of parking spaces, etc.

・For FY2019/7 results announced on 6/9, net sales increased by 7.1% to 24.381 billion yen compared to the previous period, operating income increased by 17.7% to 4.157 billion yen, and net income increased by 27.7% to 2.823 billion yen. The progress in efforts to acquire overseas large-scale commercial facility parking spaces have renewed their record sales. Profitability has also improved due to price adjustments and sales promotion activities utilising manned operation.

・For FY2020/7 plan, net sales is expected to increase by 6.6% to 26 billion yen compared to the previous year, operating income to increase by 8.2% to 4.5 billion yen, and net income to increase by 0.6% to 2.84 billion yen. More or less finishing with the process of profit improvement of existing unprofitable properties across the nation up to FY2019/7 has led to significant improvement in their monthly contract ratio. Company’s future policy is to focus on acquiring new properties.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: