|

Report type: Weekly Strategy |

■Draft for the Execution Plan for the “New Form of Capitalism” and the “Basic Policy”

On 31/5, the Japanese government indicated the draft for the plan to execute the economic policy, the “New Form of Capitalism”, and the “Basic Policy” involving economic and fiscal management and reform.

The draft for the execution plan comprises of 4 pillars: ① investment in people, ② science and technology, ③ startups (emerging enterprises) and ④ decarbonisation and digitalisation. In “investment in people”, regarding NISA (small amount tax exemption savings system), it appears that there are considerations on raising the limit on tax exempted share purchases or an extension of the period, and for iDeCo, where the amount of pension received changes according to the subscriber’s usage on contributing installments, considerations on raising its age limit on being under 65 years old. As a result of the expansion of NISA and iDeCo, perhaps attention will be on the “beginning of the month anomalies” of Japanese stocks. Also, as a policy that supports the transition of labour to growth sectors, support has been put into the improvement of abilities and the reemployment of 1 million people including non-regular work. Markets involving “reskilling (re-education)” focusing on the IT field will likely be promising.

Regarding “science and technology”, a national strategy which supports fields, such as quantum computing, artificial intelligence (AI) and biotechnology, etc., was compiled and called for corporate investment, and a science and technology advisor who will advise the Prime Minister will be positioned in the Japanese Prime Minister’s Office. In March this year, Fujitsu (6702) utilised the technology of the “Fugaku” supercomputer and succeeded in developing the world’s fastest quantum simulator of 36 quantum bits. They have made the first move in application development that anticipates practical applications of quantum computing. Also, in order to raise the research ability of Japanese universities to the top in the world, the government has begun operation of university funds of a scale of 10 trillion yen and expects to distribute tens of billion yen a year each to a few schools chosen as “internationally prominent research universities” from operational profits of the fund. HPC Systems (6597) is working with a high-performance calculation system used in science and technology and will likely benefit from supplying these to enterprises and universities.

In “decarbonisation”, the “aim to achieve investment in green transformation (GX) of a scale of 150 trillion yen in the public and private sectors within 10 years” was advocated, and bonds would be issued by the government as encouragement. As a result of the emphasis on the “maximum utilisation” of renewable energy and nuclear energy, there will likely be an increase in market expectations on the group of enterprises that may benefit from the resumption of nuclear operation and enterprises that are working on system facilities able to transmit power to other regions in a timely manner and level out the supply and demand balance of solar and wind power generation between daytime and nighttime, etc.

Regarding national security in the draft for the Basic Policy, “drastic reinforcement of Japan’s defence capability” was mentioned and it indicated a direction of easing export regulations on defence equipment. Regarding defence spending, with the question on whether to increase the amount of the aim for a 2% ratio to GDP, which is the standard in NATO countries, likely being drawn out as a future political issue, there will likely be expectations of continued benefits to key defence-related stocks, such as Mitsubishi Heavy Industries (7011), Kawasaki Heavy Industries (7012) and IHI (7013).

In the 6/6 issue, we will be covering J. Front Retailing (3086), &Do Holdings (3457), Ci Medical (3540), and Workman (7564).

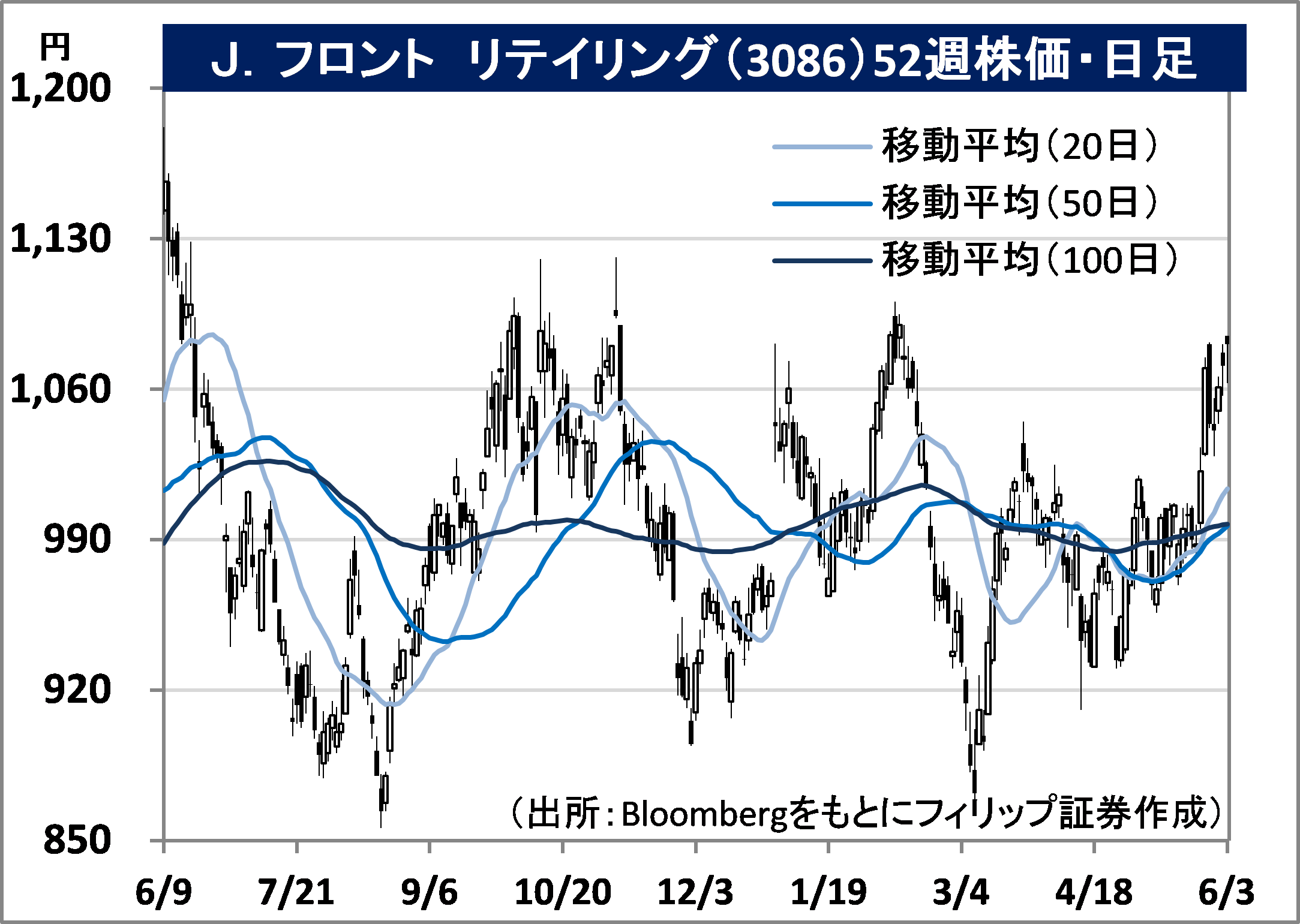

Became a holding company from a business integration between Daimaru and Matsuzakaya HD in September 2007. In addition to possessing Daimaru Matsuzakaya department stores, they operate businesses, such as Parco and Ginza Six SCs (commercial facilities), developers, settlement and finances, and wholesaling, etc.

For FY2022/2 results announced on 12/4, sales revenue increased by 3.9% to 331.4 billion yen and operating income returned to profit from (24.265) billion yen the previous year to 9.38 billion yen. With efforts made in OMO (fusion of real stores with online) and the increase in the number of Parco app members, department stores and SCs returned to operating profit. Developers and settlement and finance also increased in operating profit.

For its FY2023/2 plan, sales revenue is expected to increase by 11.6% to 370 billion yen compared to the previous year, operating profit to increase by 2.2 times to 21 billion yen and annual dividend to increase by 2 yen to 31 yen. For same-store sales in May announced on 1/6, also due to the recovery in the number of in-store customers and the rebound from the temporary suspension in business in the same month the previous year, the total of Daimaru Matsuzakaya department stores increased by 86.2% compared to the same month the previous year. The driving force was high-price products, such as jewellery, etc. and summer wear following the increase in opportunities to go out. The lifting of the ban on accepting foreign tourists visiting Japan is likely to benefit.

&Do Holdings Co., Ltd. (3457) 901 yen (3/6 closing price)

Established in 2009. In addition to the FC business, such as real estate purchasing and selling and leasing, they operate the house lease-back business, which enables the house to be sold off while living in it; the finance business, such as reverse mortgage, etc.; the real estate purchasing and selling and brokerage business; and the renovation business, etc.

For 9M (Jul-Mar) results of FY2022/6 announced on 12/5, net sales increased by 15.0% to 29.161 billion yen compared to the same period the previous year and operating income increased by 50.3% to 1.903 billion yen. Segment profits have grown with FC increasing by 9%, house lease-back increasing by 27%, finance increasing by 34%, real estate purchasing and selling increasing by 62%, real estate distribution increasing by 43% and renovation increasing by 15%.

For its full year plan, net sales is expected to increase by 0.2-13.8% to 39.1-44.438 billion yen compared to the previous year and operating income to increase by 14.8%-41.9% to 2.973-3.673 billion yen. Changed its company name from “House Do” in January this year. With House Do aiming for 1,000 stores in Japan, through a merger company which the company invests 49% in, they have begun FC expansion of purchasing and selling and the brokerage of pre-owned houses in Thailand similar to Japan, and their policy is to aim for 500 stores under the House Do brand within 10 years focusing on the capital of Bangkok.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: