Report type: Weekly Strategy

“Could This Be an Adjustment Phase That Follows a Transition Period From Economic Recovery to Expansion?”

Compared to the U.S. real GDP in 2019 prior to the spread of COVID-19 at 19.2 trillion dollars, its real GDP from January to March this year at 19 trillion dollars is almost nearing a complete recovery since the recession when annualised, and on 13/5, Bullard, the President of the U.S. Federal Reserve Bank of St. Louis, expressed that “it is transitioning to the expansion phase in the economic cycle”. In contrast, for Japan’s GDP from January to March (preliminary figures) which is planned to be announced on 18/5, in terms of market prediction, a negative growth is predicted which was last seen 3 quarters ago in response to the second declaration of a state of emergency on the COVID-19 disaster. In addition, a third declaration of a state of emergency which is being implemented from 25/4 has been expanded to other regions and extended until end May, and Nomura Research Institute revealed a trial calculation of its economic loss that exceeds 1 trillion yen. In that case, is the sharp decline in the Nikkei average from 11/5 a reflection of concerns on the said economic loss?

There is a predicted acceleration in the popularisation of COVID-19 vaccinations in Japan from this month. Based on the high correlation between the rise in U.S. stocks from January to mid-April this year and the increase in the number of vaccinations per day, perhaps the immediate economic loss following the increase in vaccinations could instead be regarded as an benefit to the stock market in the form of a demand that is carried over to the future (pent-up). With there being predictions of a transition from a recovery to expansion phase in the economic cycle similar to the U.S., perhaps it is reasonable to regard the recent decline in stock prices as an adjustment phase which causes a fall in stocks perceived to have weak resistance against rises in prices and interest rates following a transition to economic expansion.

Looking back at the Nikkei average in the past, during a period of an increasing trend from April 2003 to June 2007 from the 7,600 point level to near to 18,300 points, after increasing to the 12,200 point level in April 2004, there was a period of a plateaued boxed range until August 2005, which skyrocketed to exceed the upper limit of the range after the “dissolution of the Koizumi House of Representatives”. Also, during a period of an increasing trend from June 2012 to June 2015 from the 8,200 point level to near to 21,000 points, after increasing near to 16,000 points in May 2013, it fell to the 12,400 point level in June the same year in response to concerns of U.S. monetary tightening from the “Bernanke shock”, and exceeded 16,000 points in December that same year.

In periods of an increasing trend lasting 3 to 4 years following an economic cycle such as these, after it goes from the bottom of the stock market through a bull market that lasts about a year, it transitions to an adjustment phase and goes through a period of fluctuation within a plateaued boxed range. Similarly, in this occasion, since this month will be the 14th month since the Nikkei average plummeted to the 16,300 point level in March 2020, there is also a possibility that in the meantime, it would be a plateaued boxed range similar to past examples. It is likely that it will be regarded as a period to switch over to a portfolio that anticipates “the move from economic recovery to expansion”.

In the 17/5 issue, we will be covering Healthcare & Medical Investment Corporation (3455), Tokuyama (4043), ENEOS Holdings (5020), and Benesse Holdings (9783).

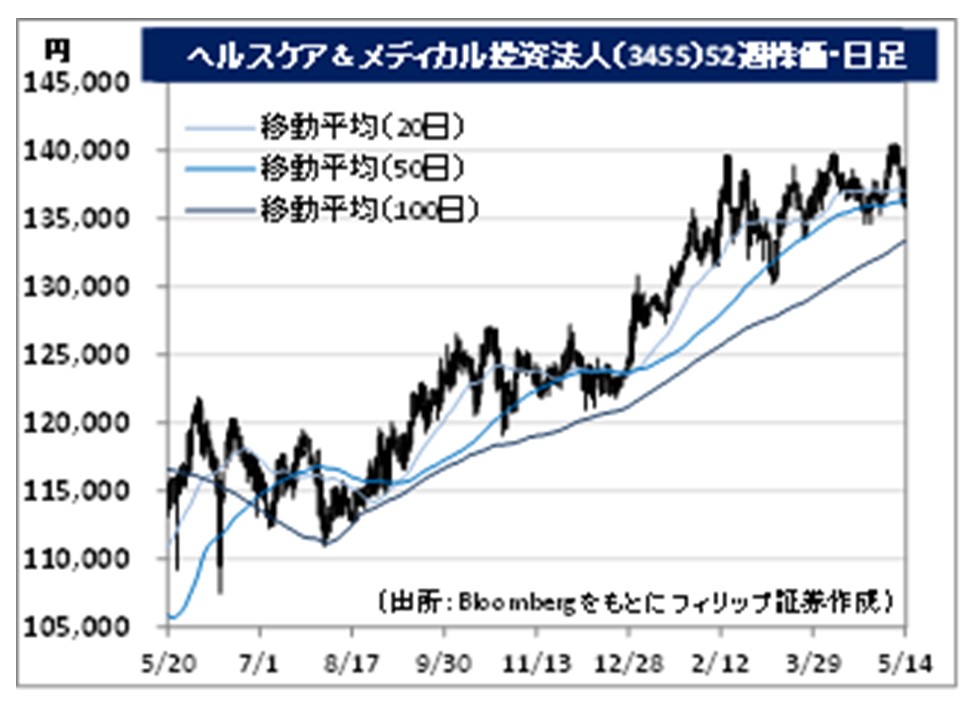

・A healthcare-specialised J-REIT which is the main sponsor for NEC Capital Solutions, Sumitomo Mitsui Banking Corporation as well as Ship Healthcare Holdings, which handles a nursing care and healthcare business. The first J-REIT to acquire hospital assets in Nov 2017.

・For FY2021/1 (2020/8-2021/1) results announced on 16/3, operating revenue increased by 1.7% to 2.058 billion yen compared to the previous period (FY2020/7), operating income decreased by 0.4% to 1.067 billion yen and distribution per unit decreased by 0.4% to 3,226 yen. Transfer and acquisition of new assets were not carried out as a measure on the spread of COVID-19. Ownership at the end of the period was 36 properties with 100% occupancy rate.

・For FY2021/7 (Feb-Jul) plan, operating revenue is expected to increase by 0.7% to 2.072 billion yen compared to the previous period (FY2021/1), operating income to decrease by 0.2% to 1.07 billion yen and distribution per unit to increase by 0.3% to 3,236 yen. Company forecasted annual dividend yield up to FY2022/1 (closing price on 13/5) is 4.75%. With the increasing sense of uncertainty in the real estate market focusing on commercial facilities and hotels due to the COVID-19 disaster, the investment corporation concluded fixed rental fee and long-term leasing contracts with healthcare facility business operators.

・Started in 1918 in Tokuyama City, Yamaguchi Prefecture (presently Shunan City) as Nihon Soda Kogyo, and is a global semiconductor silicon giant. Operates 4 segments, which are “chemicals”, “specialty products” such as polycrystalline silicon, etc., “cement” and “life & amenity”.

・For FY2021/3 results announced on 28/4, net sales decreased by 4.3% to 302.4 billion yen compared to the previous year and operating income decreased by 9.8% to 30.921 billion yen. The decline in the overseas market condition of caustic soda in the chemicals business had affected the decrease in sales and income. Compared to the previous quarter 4Q (Jan-Mar), as a result of good sales performance of polycrystalline silicon for semiconductors, net sales increased by 5.0% and operating income increased by 5.2%.

・For FY2022/3 plan, net sales is expected to decrease by 1.9% to 310 billion yen compared to the previous year and operating income to decrease by 18.3% to 28 billion yen. With silicon wafers, a material of semiconductors, being round thin plates (wafers) which are processed single crystal ingots made from highly pure polycrystalline silicon, there are concerns circulating in the industry on silicon wafers falling into a global supply shortage in 2023. There will likely be an increase in demand for the company’s polycrystalline silicon in the next few years.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: