Report type: Weekly Strategy

“Could the Revival of the NTT Family Signal the Revival of Japanese Stocks?”

On 25/6, NTT (9432) announced that they would invest 4.77% in NEC (6701) and partner via a joint development on next-generation communications infrastructure. NEC is a main corporation in the “NTT Family”, which refers to corporations having a close relation with NTT’s predecessor, the Nippon Telegraph and Telephone Public Corporation. Along with NEC, major telephone exchange manufacturers at that time, Fujitsu (6702) and Oki Electric Industry (6703), were known as the big three, and Hitachi (6501) was also a main member. Since the Nippon Telegraph and Telephone Public Corporation monopolised the procurement of large quantities of equipment and supplied them, these members were made an example of by the Structural Impediments Initiative and the Japan-U.S. Framework for a New Economic Partnership, etc. for engaging in unfair “keiretsu (conglomerate)” transactions, and with the liberalisation of communications, gradually lost their international competitiveness in price and performance, etc.

The following 2 points are considered as factors for the revival of the NTT Family. Firstly, backed by the intensification of the U.S.-China conflict, due to the increasing importance of “communications security” in the U.S. that guards against confidential information being stolen via communication devices by the Chinese players, etc., there is a demand for a force that has enough international competitiveness to especially rival China’s communications devices giant, Huawei, who spends R&D expenses of a scale of 2 trillion yen annually.

Next, in terms of market capitalisation, compared to U.S. corporations Apple, Microsoft and Amazon.com which exceed 1 trillion dollars and Chinese corporations, such as Alibaba Group coming up to about 600 billion dollars, for Japanese corporations, NTT is only about 10 trillion yen and NEC about 1.3 trillion yen, hence, there is too much of a difference in scale for 1 company alone to win in terms of international competitiveness. NTT has already carried out a capital and business tie-up with Toyota Motor (7203) in March, thus there is a possibility of a scale up of the “Japan alliance” centring on the NTT Family. The IoT and 5G era, which instantaneously links the data of things to the digital realm, is an era with greater possibilities in giving rise to the birth of new technologies or expertise through the gathering and analysis of production, distribution and retail data not limited to the barriers of a corporation or industry, but from all over the world, in a digital realm that is an industrial platform. In the digital era, the NTT Family’s “keiretsu” may be viewed positively once again and member corporations could play a crucial role in the Japan alliance platform.

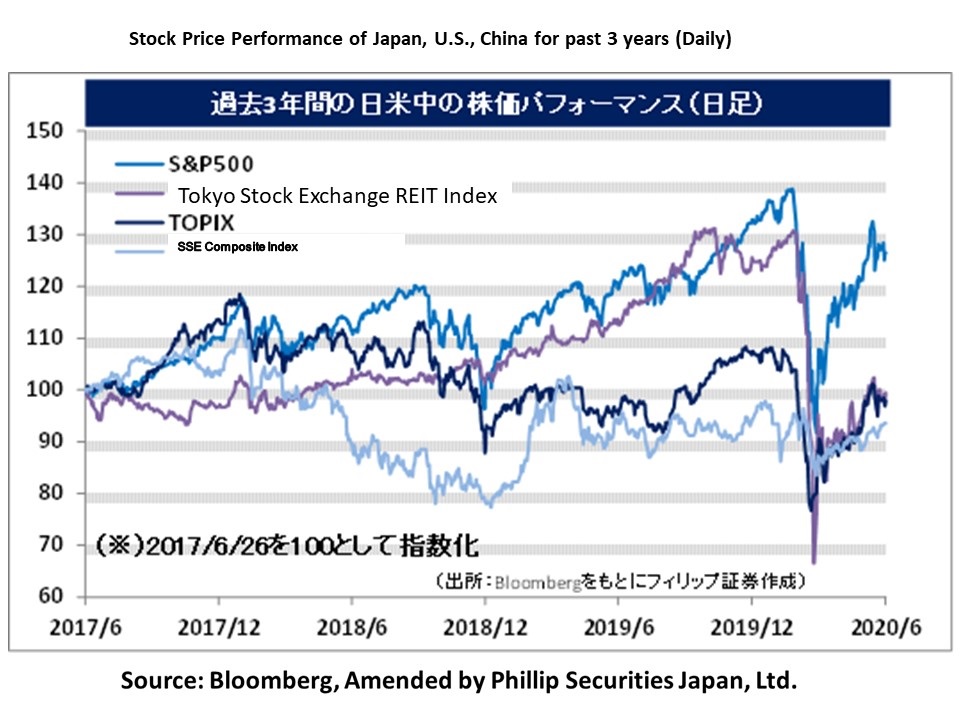

The Japanese stock market between 30/6-3/7 will likely be a week with focused awareness on the conclusion of the mid-term of Jan-Dec for pension rebalancing and the interim results, etc. of hedge funds mainly in overseas markets. Since there has been an increase stock prices in both Japan and overseas compared to end March and the U.S. 10-year bond yield shifted by an equal amount, we can infer that pension rebalancing will easily tend towards the sale of stocks and the purchase of bonds. With the U.S. stock market holiday on 3/7 around the corner, considering the series of announcements of important economic indicators in Japan and overseas on 1-2/7, there is a need to be careful of the possibility of violent price fluctuations at the end and beginning of the month.

In the 29/6 issue, we will be covering Z Holdings (4689), Nikkiso (6376), Oki Electric Industry (6703), and Zenrin (9474).

・Established in 1996 as a subsidiary of the current Softbank Group (9984). Handles the e-commerce business and the media business. Changed their company name from Yahoo Japan in Oct 2019. Company finally agreed on the business merger with LINE (3938) in Dec 2019.

・For FY2020/3 results announced on 30/4, sales revenue increased by 10.3% to 1.529 trillion yen compared to the previous year and operating income increased by 8.4% to 152.276 billion yen. The increase in earnings in their subsidiary ASKUL (2678) and ZOZO (3092) becoming their consolidated subsidiary contributed to the increase in operating income and revenue. An overall increase in profit was secured by absorbing the equity in losses due to the proactive investment in PayPay.

・Their FY2021/3 plan is undecided due to difficulties in reasonably calculating effects of COVID-19 at the moment. The return period in their consumer return business involving cashless payments ended in June, and applications for “My Number Points” aimed at popularising the My Number Card will begin from July. Since the applicable payment service is limited to one per person, it is likely to lead to an increase in the shares of the company who owns the popular PayPay and LINE Pay.

・Established in 1953. Expands the industrial business, the precision equipment business, the aerospace business, the “industrial section” under the deep UV-LED business and the “medical section” under the medical business. Their strength lies in chemical precision pumps and artificial kidneys.

・For 1Q (Jan-Mar) results of FY2020/12 announced on 15/5, sales revenue decreased by 2.7% to 36.481 billion yen compared to the same period the previous year and operating income decreased by 41.1% to 1.268 billion yen. Despite an increase in profit and income in the medical section from an increase in the demand to respond to acute renal failure and to prevent virus infection, the industrial section’s industrial business and aerospace business suffered the effects of the COVID-19 catastrophe.

・For its full year plan, net sales is expected to increase by 5.0% to 174 billion yen compared to the previous year and operating income to decrease by 11.8% to 11 billion yen. In addition to the increase in the demand to respond to renal failure from a worsening of the COVID-19 infection in the CRRT (acute blood purification therapy) business in the medical section, since the confirmed efficacy of the deep UV-LED applied spatial sterilising and deodorising device “Aeropure”, which launched in end Jan, their orders received have performed strongly.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: