Report type: Weekly Strategy

”Container problem following on the heels of the Covid-19 pandemic? – Focus on automotive industry”

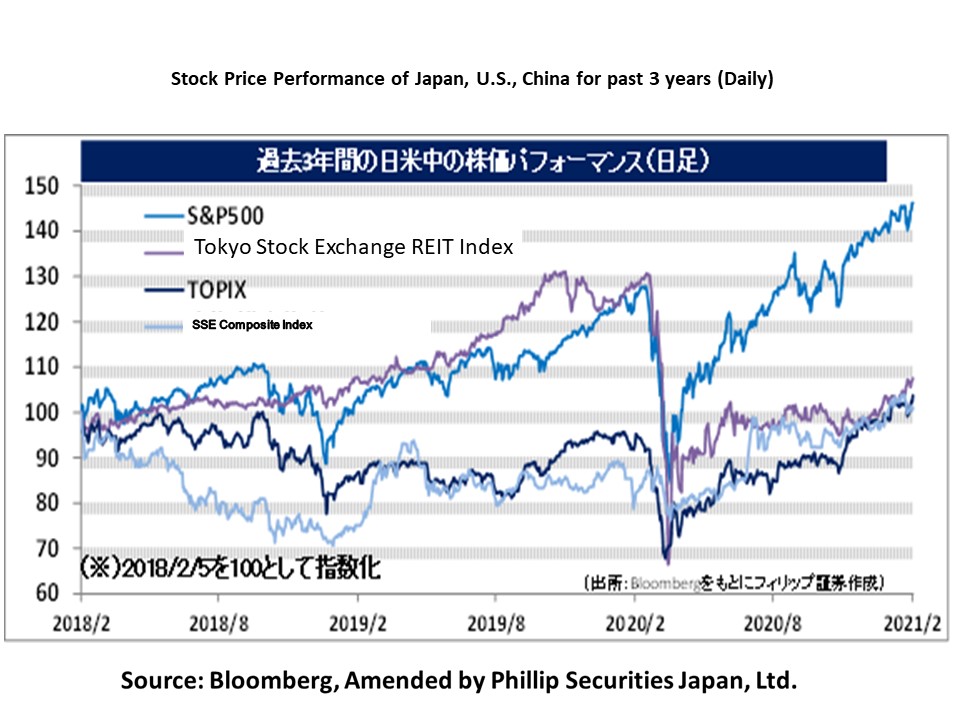

On 1/2, the number of people vaccinated against Covid-19 in the US reached 26.5 million, exceeding the cumulative number of positive test cases. As of 4/2, the number of people vaccinated worldwide has also reached 108.15 million, surpassing the cumulative number of people tested positive (104.83 million). In response to the widespread use of vaccinations, global stock markets are also increasingly focusing on economy-sensitive stocks in anticipation of economies returning to normal. As far as the forward-looking stock market world is concerned, it may not be an exaggeration to say that the Covid-19 pandemic has already passed.

Meanwhile, restrictions on economic activity continue in the real world. Demand for the transportation of furniture and home appliances to North America has been strong since last summer due to booming housing sales. Transportation of auto parts and semiconductors has also been recovering since autumn. Under such circumstances, freight rates for marine container transportation have soared due to the emerging shortage of containers. Rates have remained very high, with those for shipments from China to the US doubling from the same period last year, and those to Europe quadrupling for the same period. With the large number of containers piling up in the region, this shortage of containers has been exacerbated by the rapid increase in cargo and the slowdown of unloading operations at US ports due to Covid-19 response measures. In addition to the shift of some ocean freight to air freight due to congestion on container ships, the supply and demand for air freight space tightened due to a recovery in cargo movement especially for automotive parts, semiconductors and electronic equipment. As a result, air freight rates to Europe and the US have soared. It can indeed be said that “following on the heels of the Covid-19 pandemic, the next issue is container problem”.

In the automotive industry in particular, Germany’s Volkswagen was forced to reduce production at its largest plant in the world situated within Germany due to a worsening shortage of parts. Honda was also reported to be cutting production in the US and Canada due to difficulties in procuring semiconductors. The impact on business activities could be far-reaching, including production cutbacks, worsening cash flow due to increased product inventories, and stoppage of new orders until the turmoil is resolved, with concerns that it could spread to the entire industry.

It is also noteworthy that Apple (AAPL) has reportedly approached several automakers, including those in Japan, about producing electric vehicles (EVs). Indeed, a new wave is sweeping through the automotive industry. For Japanese automakers, the horizontal division of labor model, in which Apple does design and development and only outsources production, is not likely to be readily accepted. Some observers are speculating that Nissan Motor (7201) will take over the project because firstly, Apple’s R&D base in Japan is located in Yokohama, and secondly, Nissan’s subsidiary, Mitsubishi Motors (7211), will end EV production at the end of March, thereby freeing up production lines. There is a possibility that Alphabet (GOOG), which owns Google, and other companies may also follow suit, which will increase the attention of foreign investors to Japanese automakers.

In the 8/2 issue, we will be covering Matsuoka Corp (3611), Maxell Holdings (6810), Canon Electronics (7739), and Nippon Yusen (9101).

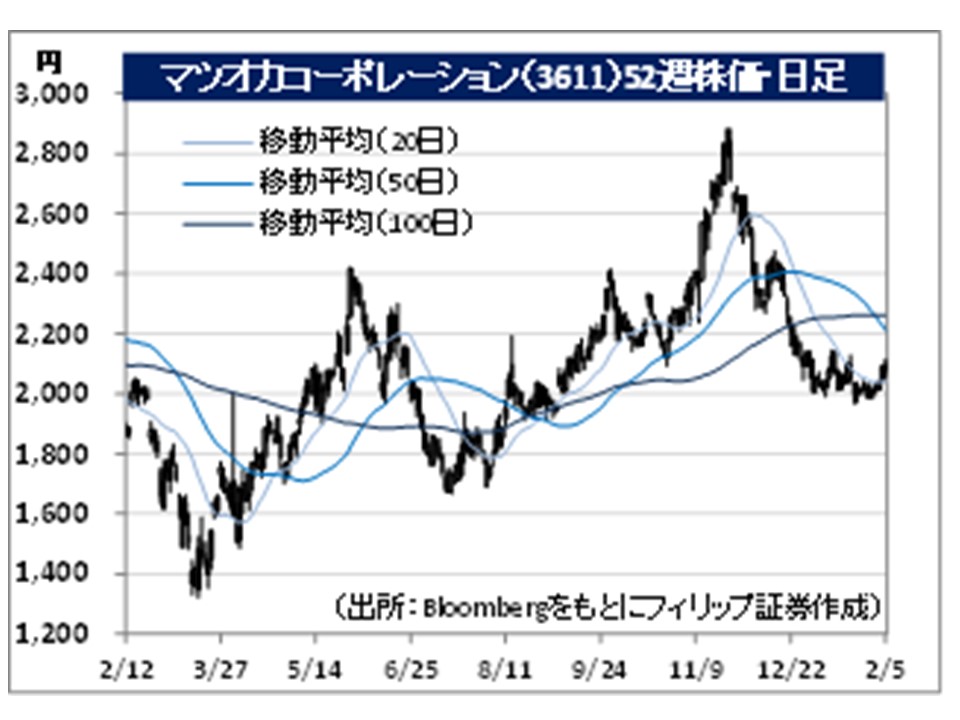

・Founded in 1956 as Matsuoka Kimono Store. Company operates an “apparel OEM business” in which it receives orders from apparel manufacturers, trading companies, and mass merchandisers to produce apparel under the consignor’s brand, including planning, manufacturing, and distribution.

・For 2Q (Apr-Sep) results of FY2021/3 announced on 13/11, net sales increased by 7.3% to 28.893 billion yen compared to the same period the previous year, and operating income increased by 89.2% to 2.918 billion yen. Although orders for existing products were sluggish due to a sharp drop in demand for apparel products following the Covid-19 pandemic, sales and profits increased thanks to the production of cloth masks and the development of a production system that responds flexibly to customer needs.

・For its full year plan, net sales is expected to decrease by 12.5% to 50.0 billion yen compared to the previous year, and operating income to increase by 22.9% to 3.2 billion yen. In response to the military coup that occurred in Myanmar on 1/2, company announced that there would be no disruption to operations at the two plants it operates in the country. As habits of wearing masks due to the Covid-19 pandemic take root, diversification of demand for masks with functions corresponding to seasonal changes, and those that are comfortable to wear, made of comfortable materials, and rich in design, should contribute to business performance.

・Established in 1966. After becoming a wholly-owned subsidiary of Hitachi, Ltd (6501) in 2010, company was relisted in 2014 and became independent from the Hitachi Group. Mainly engaged in the manufacture and sale of energy, industrial materials, and electrical and consumer products.

・For 9M (Apr-Dec) results of FY2021/3 announced on 29/1, net sales decreased by 7.2% to 103.336 billion yen compared to the same period the previous year, and operating income increased two times to 2.849 billion yen. Although sales of optical components for automotive applications decreased, sales of lithium-ion batteries for consumer use and embedded systems relating to semiconductor increased, while improved profitability of health and beauty care products and cost reduction measures contributed to higher operating income.

・Company has revised its full-year plan upwards. Net sales is expected to decrease by 5.5% to 137.0 billion yen compared to the previous year (original plan 133.0 billion yen), and operating income to return to profitability from minus 137 million yen in the previous year to 3.5 billion yen (original plan 1.5 billion yen). We expect to see more stay-at-home demand, recovery in automotive and semiconductor-related products, and continued improvement in the profitability of health and beauty care products. Company has developed a sulfide “coin-type all solid-state battery” that can be used at ultra-low temperatures of minus 50 to 125 degrees Celsius, which is expected to be in demand for transporting Covid-19 vaccine.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: