Report type: Weekly Strategy

Concern On the Japanese Economy and Expectations of Undervalued Japanese Stocks

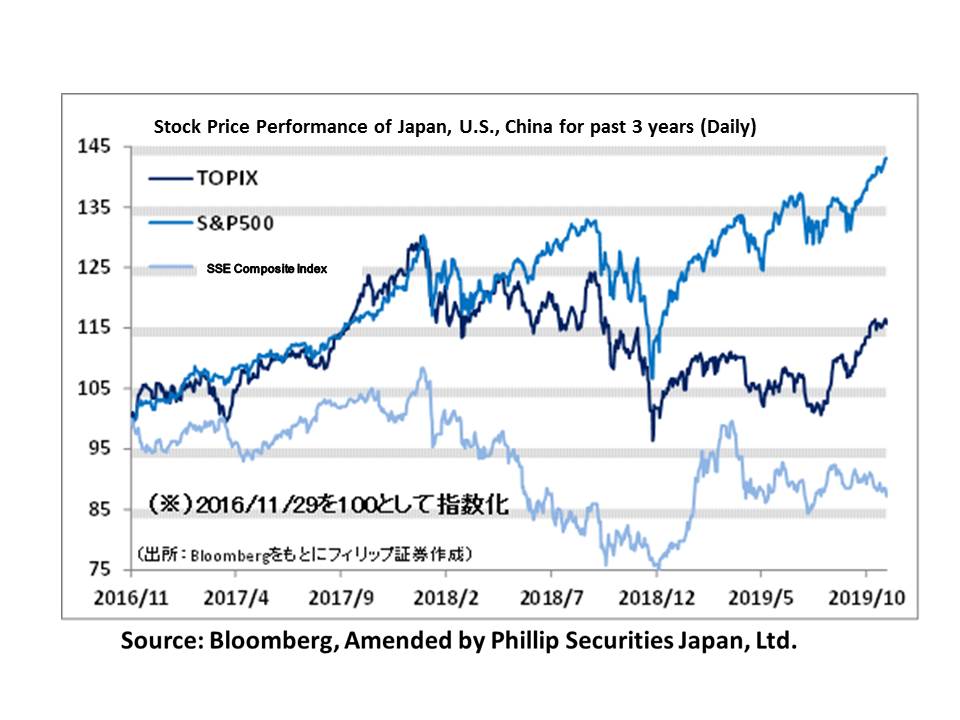

Amidst growing concerns on the future of the Japanese economy in 2020, we may see the gradual emergence of an ambivalent market mentality where attention is focused on undervalued Japanese stocks from the value aspect. In the Japanese stock market in the week of 25/11, as a result of the announcement that China would be reinforcing protection on intellectual property, major stock price indexes in the US market renewed their record highs in addition to a dominance in buying due to expectations of progress in the US-China trade negotiations, which led the Nikkei average to mark the year’s record high at 23,608 points on 26/11. However, in the early morning (Japan time) on 28/11, President Trump signed and concluded the “Hong Kong basic human rights bill”. In the midst of concerns of implications from backlash from China on the US-China trade negotiations, trading was also thin due to the US stock market that was closed on Thanksgiving, which prevented the rise in price of the Nikkei average.

Retail sales for October announced on 28/11 by the Ministry of Economy, Trade and Industry fell by 7.1% YoY and this decrease surpasses the 4.3% decrease which immediately followed the previous tax hike. Despite difficulties in identifying trends due to the series of typhoons, consumption after the consumption tax hike got off to a difficult start with retail sales significantly declining, such as the 17.3% decrease in department stores and the 14.2% decrease in home appliance specialty stores. Although convenience stores, whose reward point system involving cashless payments proved to be effective, was strong with a 3.3% increase, it did not seem to be enough to support consumption as a whole. This appears to contrast with the highly prospective consumption in the year-end shopping season in the US economy, whose labour market remains strong.

The state of the “unsettled selling balance of arbitrage” exceeding the “unsettled buying balance of arbitrage” involving spot and futures arbitrage continuing from June 2019 can be regarded as a cause for concern since it could be a factor that causes a lead in long sales, which is feared as a trend in the Japanese economy after the Tokyo Olympics and the consumption tax hike. On the other hand, the weighted average PBR (price-to-book ratio) of the closing price of the Nikkei average on 28/11 was 1.15 times, and due to a predicted continuous increase in the BPS (book value per share) as well, presently, it is easy for one to feel at ease due to the low being stable. Furthermore, since we cannot look forward to bond yield which form the basis of asset allocation after a recession, we can expect that the likely continuance of investments in stocks which focus on dividend yield will also serve as a factor that will support the Japanese stock market.

The UN Climate Change Conference COP 25 will be held in Madrid from 2/12 and expectations on renewable energy are likely to rise all the more across the world. It looks like there will be room for technology reassessments in Japanese companies involved with floating wind turbines.

In the 2/12 issue, we will be covering Toda (1860), GiG Works (2375), Asahi Kasei (3407), Being (4734), Bandai Namco Holdings (7832) and Softbank (9434).

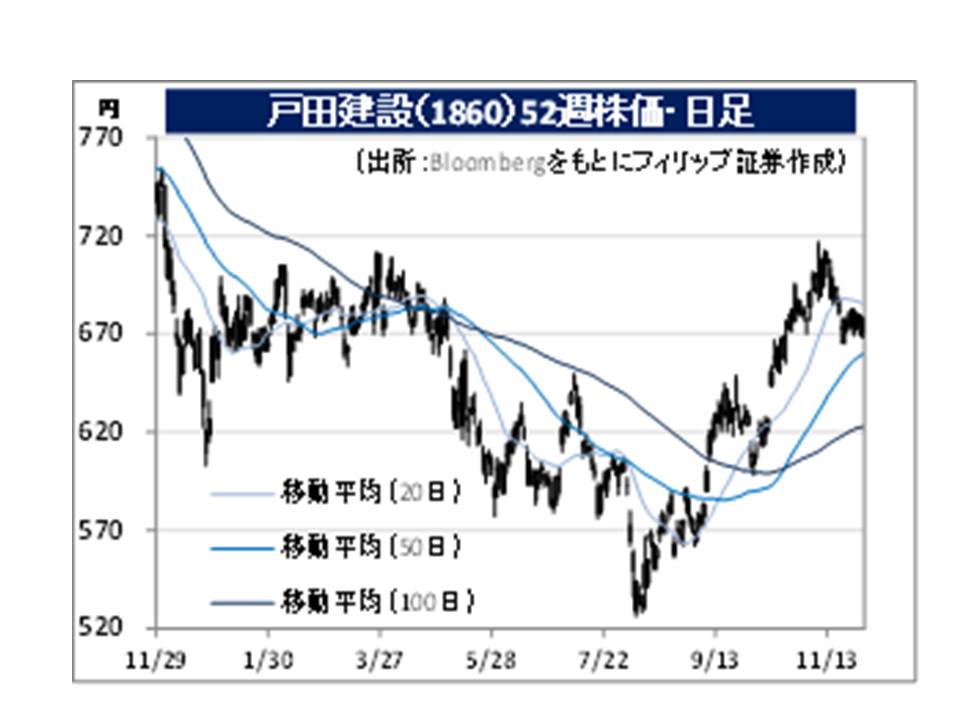

・Founded in 1881. Has the domestic construction business, domestic civil engineering business, investment development business, new business fields (including the floating wind turbine business) and the overseas business as their main businesses, in addition to expanding the PFI business involving various other businesses, etc.

・For 1H (Apr-Sep) results of FY2020/3 announced on 8/11, net sales increased by 15.9% to 235.365 billion yen compared to the same period the previous year and operating income increased by 50.8% to 15.544 billion yen. Although construction orders decreased by 33.0%, progress in domestic construction projects, an increase in sales of their overseas business, as well as progress in high profit major construction projects in domestic construction contributed to an increase in both sales and profit.

・For its full year plan, net sales is expected to increase by 1.9% to 520 billion yen compared to the previous year and operating income to decrease by 11.1% to 30.7 billion yen. Company has built a floating wind turbine facility in Goto Islands in Nagasaki Prefecture, which is a “promising region” under the ‘Act of Promoting Utilization of Sea Areas in Development of Power Generation Facilities Using Maritime Renewable Energy’. Due to applications of the semi-submersible float raiser developed by the company, we can look forward to a significant optimisation and simplification to the construction process of offshore wind power installation works. Expectations on the company is likely to rise along with the popularisation of Japan’s renewable energy.

・Established in 1977. Expands a “24-hour, 365 day” support service focusing on IT business across Japan for companies whose business targets are users of the IT environment and IT-related equipment as well as individuals and companies utilising them. Offers services in the gig economy area. Changed their trade name from ThreePro Group in Aug 2019.

・For FY2019/10 announced on 28/11, net sales increased by 9.5% to 17.584 billion yen compared to the same period the previous year, operating income increased by 33.8% to 784 million yen and net income increased by 45.1% to 448 million yen. Renewed their record profit which was 7 years ago. Projects for communication sales business operators have increased. A growth in their in-house developed CRM system and system repair projects have also contributed to a profit increase.

・For their FY2020/10 plan, net sales is expected to increase by 8.0% to 19 billion yen compared to the previous year, operating income to increase by 14.8% to 900 million yen and net income to increase by 22.7% to 550 million yen. In their mainstay BPO business, 2 out of 5 subsidiaries are scheduled to be reorganised via consolidation effective from 1/2. Company is working towards reducing management costs and integrating operating and recruitment activities.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: