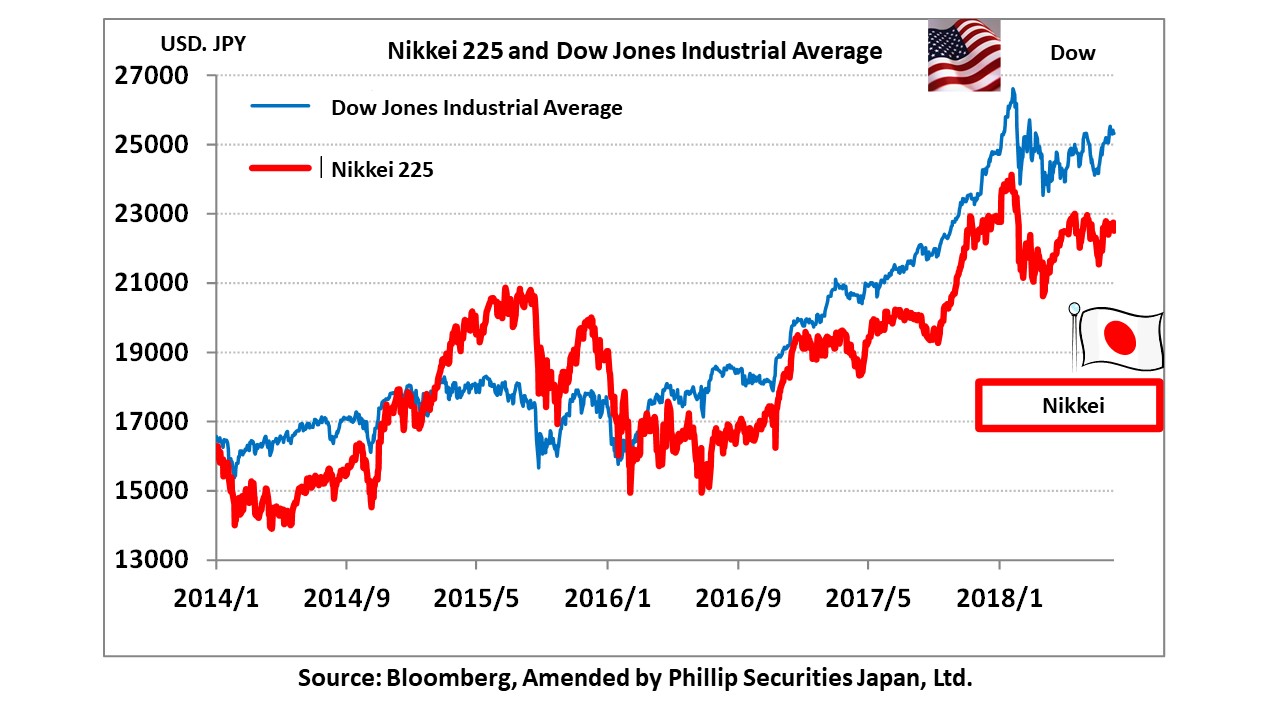

With the extremely hot weather striking the Japanese archipelago, corporate earnings releases of major companies are at their peak. Indeed, the market is getting hot, what with Apple (AAPL) achieving market capitalization of 1 trillion dollars. The US is showing strong economic performance, with GDP for the April-June quarter increasing by 4.1%. At the same time, monetary policy tweaks by the BOJ is also making strong impact on interest rate and forex movements. However, hardline US trade policy against China has thrown cold water onto the market, affecting Japanese stock movements.

On 7/31, President Trump announced that, as a third step of additional tariffs on China, he was considering imposing 25% additional duties on 200 billion dollars’ worth of imports to the US. It seems that he is of the view that the original 10% tariff was not enough owing to the depreciation of the RMB, and has therefore given instructions to raise the tariff to 25%. He is seeking industry input regarding this 25% tariff, and a final decision is due after September. On 7/6, the US fired the first shot with a 25% tariff on 34 billion dollars’ worth of imports from China. Following that, it is currently planning another round for 16 billion dollars’ worth of imports. US sanctions on Chinse imports amounted to 250 billion dollars, largely exceeding total imports from the US. As a result, China is currently not taking any countermeasures in the meantime.

While refraining from the Beidaihe meeting where important matters are usually informally discussed, and with trade pressures from the US in mind, the meeting of the Political Bureau of the Central Committee of the CPC chaired by President Xi Jinping decided on a policy to prop up the economy through proactive fiscal policies in the second half of 2018. The plan is apparently to expand public investment such as rural infrastructure improvement. Monetary policy seems to be aiming for maintenance of reasonable adequate liquidity, and moving towards monetary easing. On the working level, US Treasury Secretary Mnuchin and Chinese Vice Premier Liu He are leading the trade negotiations. At the same time, some US officials and corporate executives have requested Chinese officials to get Vice President Wang Qishan to visit the US for negotiations so as to resolve the trade friction. Since the 1990s, he has been interacting with many US stakeholders both as a banker and a senior government official, and is well looked upon by the financial and political circles in the US. For the time being, the progress of trade negotiations will be a factor influencing market fluctuations.

Although the outlook is uncertain, companies such as Konica Minolta (4902), Sony (6758) and Tokyo Electron (8035) have either announced good results for the period from April-June, or adjusted their full-year performance upwards. Good progress towards full-year performance had also been confirmed for Mitsubishi Corporation (8058) and Mitsubishi UFJFG (8306). We need to identify investment targets including expected PER levels.

In the 8/6 issue, we will be covering Konica Minolta (4902), MODEC (6269), Japan Cash Machine (6418), Sony (6758), Mitsubishi Corp (8058) and Mitsubishi UFJ Financial Group (8306).

Selected Stocks:

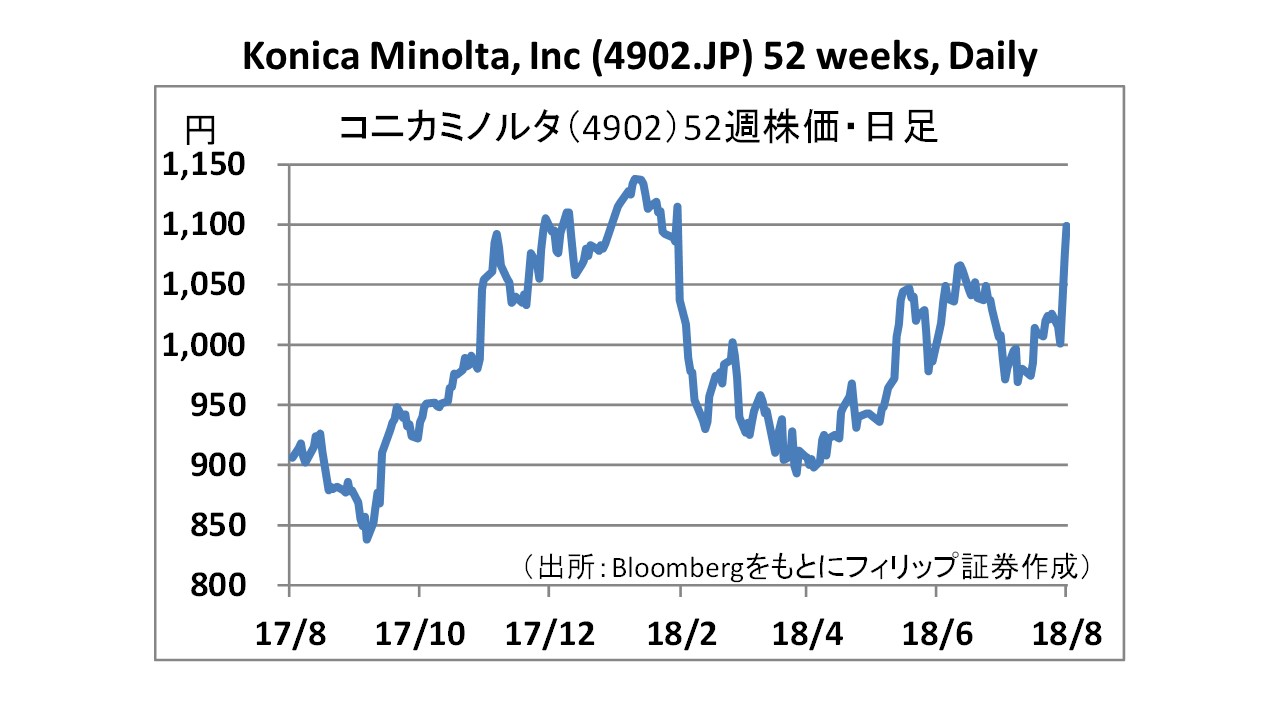

Konica Minolta, Inc (4902)

・Founded in 1873. Handling office, professional print, health care, industrial materials and equipment businesses. Involved in multifunction machines, digital printing systems, image diagnostic systems (digital X-ray diagnostic imaging, diagnostic ultrasound systems, etc), TAC films, OLED lightings, and industrial inkjet heads, etc.

・For 1Q (Apr-June) of FY2019/3, net sales increased by 9.8% to 255.214 billion yen compared to the same period the previous year, operating income increased by 77.2% to 15.445 billion yen, and net income increased by 2.1 times to 11.18 billion yen. Office business had performed well. In Europe, strong growth mainly in color 65/75 ppm machines. Sales have grown in all regions including North America, Japan, China and SE Asia, etc.

・As revenue from securitization of assets has increased more than anticipated, company has revised its FY2019/3 plan upwards. Net sales is expected to maintain that of the original plan, increasing by 4.7% to 1.08 trillion yen compared to the previous year, operating income to increase by 15.1% to 65.0 billion yen (original plan 60.0 billion yen), and net income to increase by 19.4% to 38.5 billion yen (original plan 37.0 billion yen). Premise exchange rate remains unchanged.

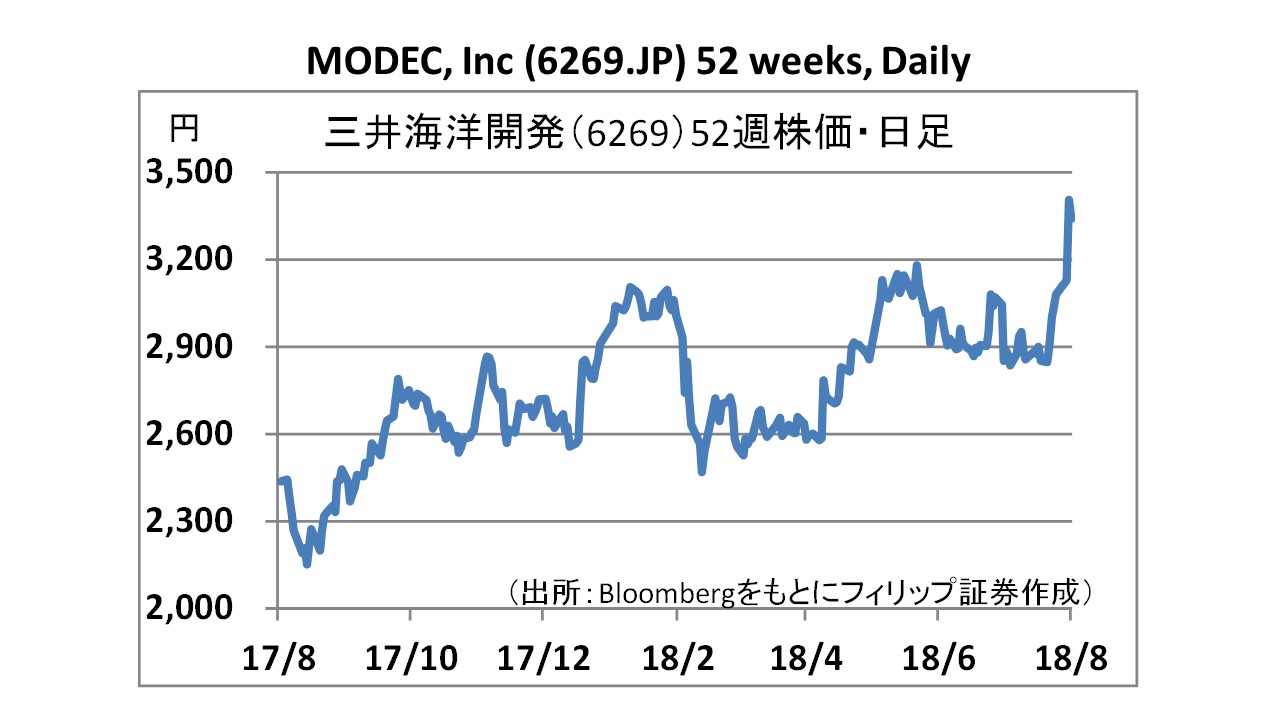

MODEC, Inc (6269)

・Founded in 1968. Core business includes design, construction, installation, leasing and operation servicing of floating marine oil and gas production facilities such as FPSO, FSO, TLP and semi-submersibles. Providing total service relating to marine oil and gas exploration projects to petroleum exploration companies around the world. Has No.2 global share of the FPSO business.

・For 1H (Jan-June) of FY2018/12, net sales increased by 10.9% to 112.843 billion yen compared to the same period the previous year, operating income increased by 4.0 times to 10.844 billion yen, and net income increased by 61.4% to 10.207 billion yen. Gross profit increased by 6.8 billion yen owing to realization of previously unrealized profit accompanying the start of MV29 charter. ROI temporarily declined due to accounting treatment of affiliates. ・Company has revised FY2018/12 plan upwards. Net sales is expected to maintain that of the original plan, increasing by 15.1% to 220.0 billion yen compared to the previous year, operating income to increase by 4.8% to 12.0 billion yen (original plan 10.0 billion yen), and net income to decrease by 22.9% to 15.0 billion yen (original plan 14.0 billion yen). Company plans to pay an annual dividend of 42.5 yen per share. Excluding special dividends, this is an increase for 14 consecutive years.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: