Report type: Weekly Strategy

Breaking Away From “PBR Shakeup” and Low PBR Stocks

The closing price of the Nikkei Average on 19/5 was 20,433 points, which was 299 points higher than that of the previous day, and the weighted average PBR (Price-to-Book Ratio) increased to 1.0 times. The weighted average PBR recovered to the net asset price level in about two months after the ratio had fallen to 0.82 times on 16/3. Up until now, the basis of the fundamentals for the Nikkei Average being considered as oversold and undervalued in the midst of Covid-19 infection was the weighted average PBR being 1.0 times. We can say that it has reached a level where immediate future milestones can be easily attained.

On the other hand, the current period forecast PER (Price Earnings Ratio), an investment measure most favored by investors, exceeded 20 times on 13/5 based on the weighted average of the closing price of Nikkei Average, for the first time since 2013/4. It continued to rise even after that date to reach about 40 times on 21/5. Due to the uncertain impact of Covid-19, a number of companies have declined to announce their earnings forecasts. With forecast earnings expected to decline even if performance forecasts are announced, it is becoming increasingly difficult for investors to use forecast PER as an investment measure. Therefore, in general, focus is on the certainty of net assets increasing even if profits were to decline so long as earnings do not result in a loss. It is therefore conceivable that there will be no choice but to continue to rely on investments based on actual PBR. In that sense, it can be said that an environment called the “PBR shake-up” is evolving where the level of low PBR stocks which is well below a PBR of 1.0 times is likely to occur.

However, low PBR is not the only option. First, the inability to effectively use the assets and the capital deposited by shareholders tends to be a reason for a particular stock to be neglected as being undervalued. Therefore, in addition to shareholder return measures to improve asset efficiency, it is also important that business structural reforms such as selection and concentration of businesses and withdrawal from unprofitable businesses are carried out. Next, while many listed companies are not disclosing their business outlook, those that disclose their business outlook even if profits are likely to fall will likely be investment targets because we are likely to see sustainable increase in net assets, and value these as bargain stocks because the gap between the stock price and net asset price per share is increasing. With the prolonging of the “nest dwelling consumption” as a result of Covid-19, we can see that increasing demands for corrugated boxes due to expansion of online mail-orders are leading to an increase in corrugated box production. Furthermore, the demand for non-woven fabric materials for masks is increasing worldwide. With the resumption of economic activities, it has become necessary to use robots to clean hospitals, train stations, airports, commercial facilities, etc., safely with disinfectants to prevent infection, and to install acrylic sheet between facing seats at restaurants. It is therefore not surprising if companies arise from amongst paper and chemical manufacturers which can take advantage of such demands to eliminate their low PBR conditions.

In the 25/5 issue, we will be covering Tomoku (3946), Mitsui Chemicals (4183), Nippon Steel (5401), and CYBERDYNE (7779).

・A general packaging manufacturer established in 1949. Operates the Corrugated Board Business that handles corrugated board sheet and cases, the Housing Business that sells housing materials to Sweden House, and the Transportation and Warehouse businesses.

・For FY2020/3 results announced on 8/5, net sales increased by 2.9% to 176.583 billion yen compared to the previous year, and operating income increased by 32.8% to 6.911 billion yen. While striving to revise cardboard product prices, the spread of Covid-19 infections had contributed to the increase in corrugated board production for beverages, processed foods, chemicals, detergents, etc., thereby contributing to higher sales and profits.

・For FY2021/3 plan, net sales is expected to increase by 4.8% to 185.0 billion yen compared to the previous year, and operating income to increase by 8.5% to 7.5 billion yen. In the Corrugated Board Business, the medium- to long-term market expansion for online shopping, the stay-at-home situation due to Covid-19 leading to increase in demand for food-related products resulting from “nest dwelling consumption”, and the increase in export prices for corrugated boxes as a result of shutdowns in Europe and the US leading to decrease in waste paper supply, had all become push factors

・A comprehensive chemical manufacturer established in 1997 through the merger of the former Mitsui Chemical Industry with Mitsui Toatsu Chemicals. Main businesses include the Mobility Business, Health Care Business, Food & Packing Business and manufacturing and sales of basic materials.

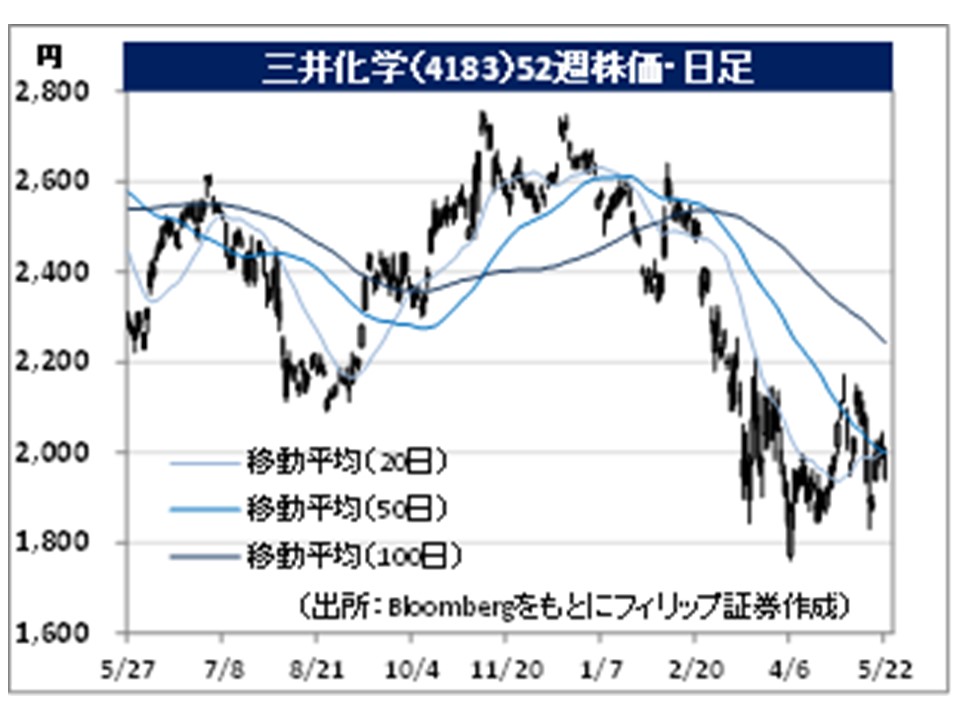

・For FY2020/3 results announced on 14/5, net sales decreased by 9.7% to 1.3389 trillion yen compared to the previous year, and operating income decreased by 23.3% to 71.636 billion yen. Sales declined due to a drop in sales prices as a result of a fall in crude oil prices and a decline in sales volume due to the spread of Covid-19. In addition, sales conditions deteriorated and fixed costs increased, leading to a decline in profits.

・For FY2021/3 plan, net sales is expected to be 1.145 trillion yen, and operating income to be 37.0 billion yen. Comparisons with the previous period are not stated as the company has adopted IFRS with effect from FY2021/3. Automotive parts business is expected to continue to struggle, and there is concern about supply of IPA (Isopropyl Alcohol) as a disinfectant in Europe and the US even as demand there is increasing. In addition, the price of non-woven fabrics for masks and protective clothing is increasing due to global demand. Company is therefore also expanding production by increasing factory capacity.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: