|

Report type: Weekly Strategy |

“Between Tightening and Easing; Commodity Shift Remains Unchanged”

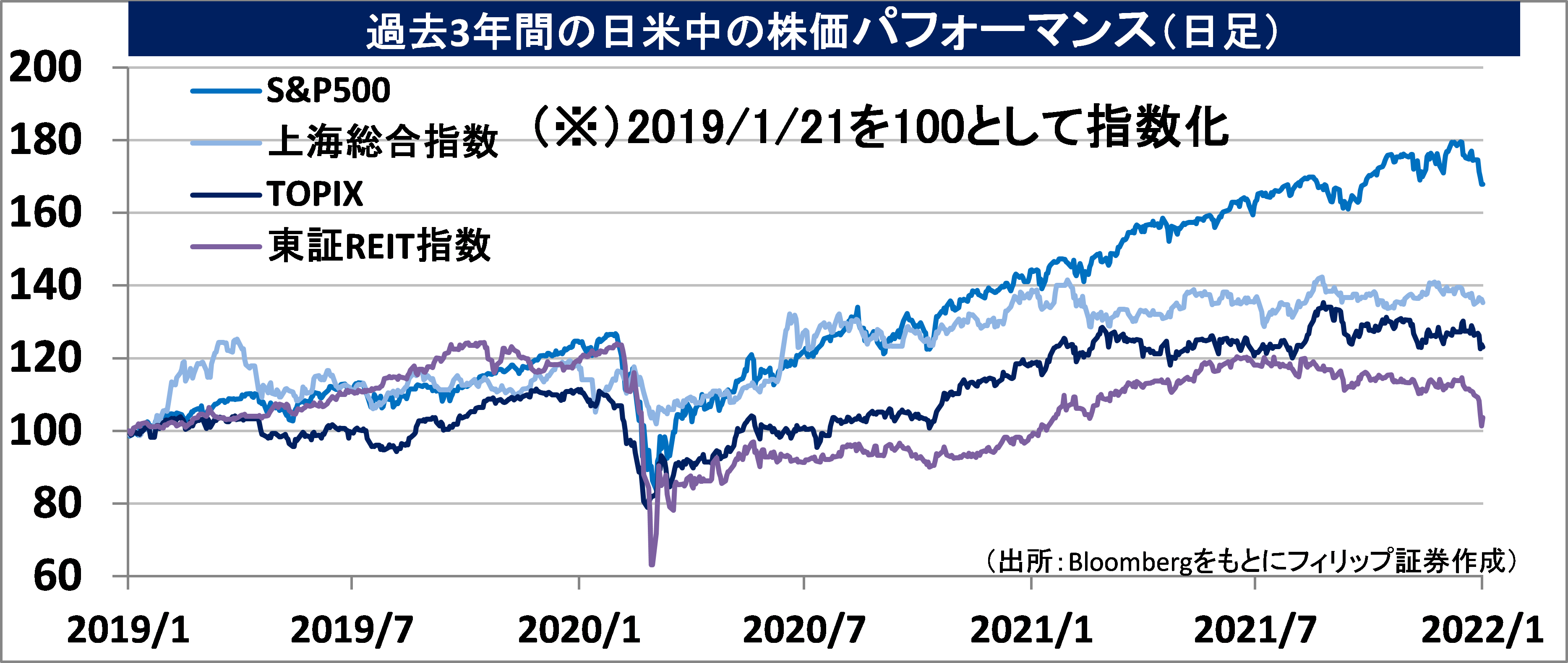

The Japanese stock market may have begun to surge as it is caught between the US market, which is wary of monetary tightening being hinted at the US FOMC meeting on 26/1, and the Chinese market, which, in contrast, has been easing monetary policy, with the PBOC lowering its preferential lending rate for two consecutive months.

The Nikkei Average, which maintained the level of around 28,000 points on 14/1, had ended in the 27,000 points range from 18/1 onward. At the closing price on 20/1 (27,772 points), the Price-to-Book ratio (PBR), weighted by market capitalization, was 1.25 times. It has been difficult for the market to decline due to the lingering effects of the replacement of three stocks at the end of September last year with high PBR stocks that are popular among investors. However, the average PBR level of 1.20 times (26,660 points), which is the average level over a 5-10 year term, is likely to be the target for lower prices for the time being.

HSBC Asset Management’s New Year online seminar for the media held on 19/1 has attracted a lot of attention. Against a current awareness that “The global economy is currently in a mid-cycle ‘expansion’ phase, with economic growth and corporate profits past their peaks, inflation rising, and policy normalization underway”, it is noted that “investors have enjoyed high returns over the past 18 months, mostly from borrowing from the future at high PERs, causing the macro outlook to deteriorate due to higher market valuations and lower margins of safety”. In addition to this, it was noted that European, Japanese, and Asian emerging market stocks, which have been lagging behind US stocks, have shown some promise. It was further noted that China’s economy has moved from monetary policy and regulatory tightenings to monetary policy easing to prepare for shocks such as credit concerns in the real estate industry.

From Dec 2020 to Jan 2021, this Weekly had reported that the multiples of the “S&P GSCI Total Return Index” for commodities to the S&P500 Index were at historic lows, that a “commodity shift” accompanying a “shift to emerging economies” had occurred from around 2002 to mid-2007 after the bursting of the IT bubble in 2000, and that amongst Japanese stocks, steel and shipping stocks had outperformed other industry indices by a wide margin due to this commodity shift. In the 13th Dec issue last month, we had expressed our bullish stance on the Japanese stock market, citing that, “Although the supply-demand situation has stalled, we are waiting for inflation-averse money”. The view that a major trend toward a commodities shift has already begun remains unchanged at this point, one year later. In terms of the Poverty Index, which is the sum of the unemployment rate and the inflation rate, Japan is among the lowest in the world, and China is also low globally. If inflation-averse global money were to shift from the US to China, there seems to be no reason that such funds will also not come to Japan.

In the 24/1 issue, we will be covering Nichirei (2871), Japan Tobacco (2914), Marubeni (8002) and Gakken Holdings (9470).

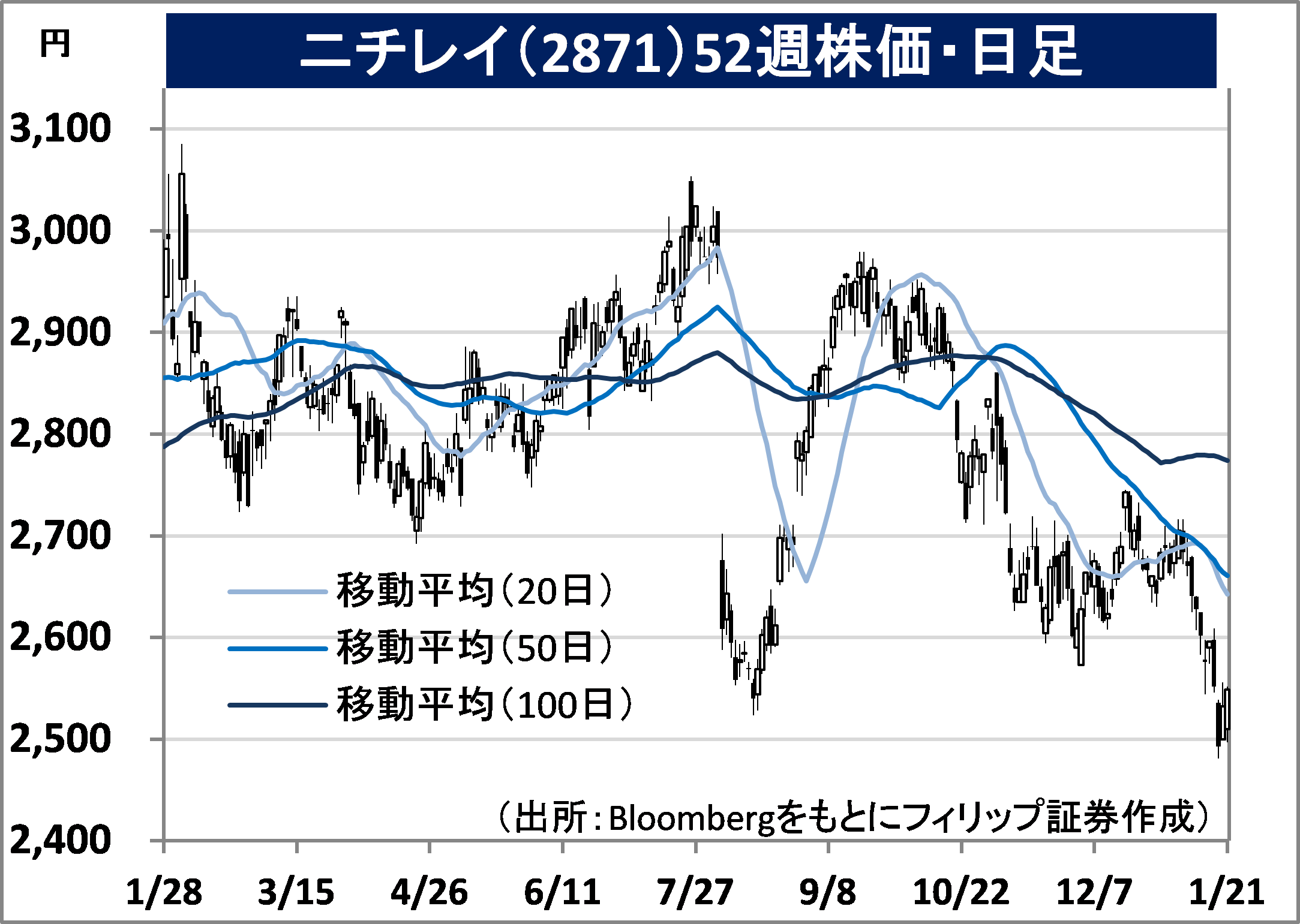

・Established in 1942 based on the Fisheries Control Order. Mainly engaged in the Processed Food Business, Marine Products, Meat and Poultry Business, Cold Storage Logistics Business, and Real Estate Business. In addition to being the leader in refrigerated warehousing and frozen foods, low-temperature logistics is expanding, especially in Europe.

・For 1H (Apr-Sep) results of FY2022/3 announced on 2/11, net sales increased by 4.5% to 294.578 billion yen compared to the same period the previous year, and operating income decreased by 4.3% to 16.02 billion yen. Net sales increased owing to steady sales in mainstay Processed Food Business and Cold Storage Logistics Business, but operating income decreased due to lower capacity utilization caused by the spread of Covid-19 infection in Thailand, and higher raw material and procurement costs.

・Company has adjusted its full-year plan downwards. Net sales is expected to remain unchanged at 600.0 billion yen, up 4.8% YoY, and operating income to increase by 0.2% to 33.0 billion yen (original plan 35.0 billion yen). Company is strong in croquettes and fried rice in the frozen foods for home use sector, ranking second in domestic production of croquettes and third in fried rice in 2020, with a 51% increase over the previous year. Furthermore, the Covid-19 situation in Thailand, a factor in the decline in profits, has stabilized since Oct last year.

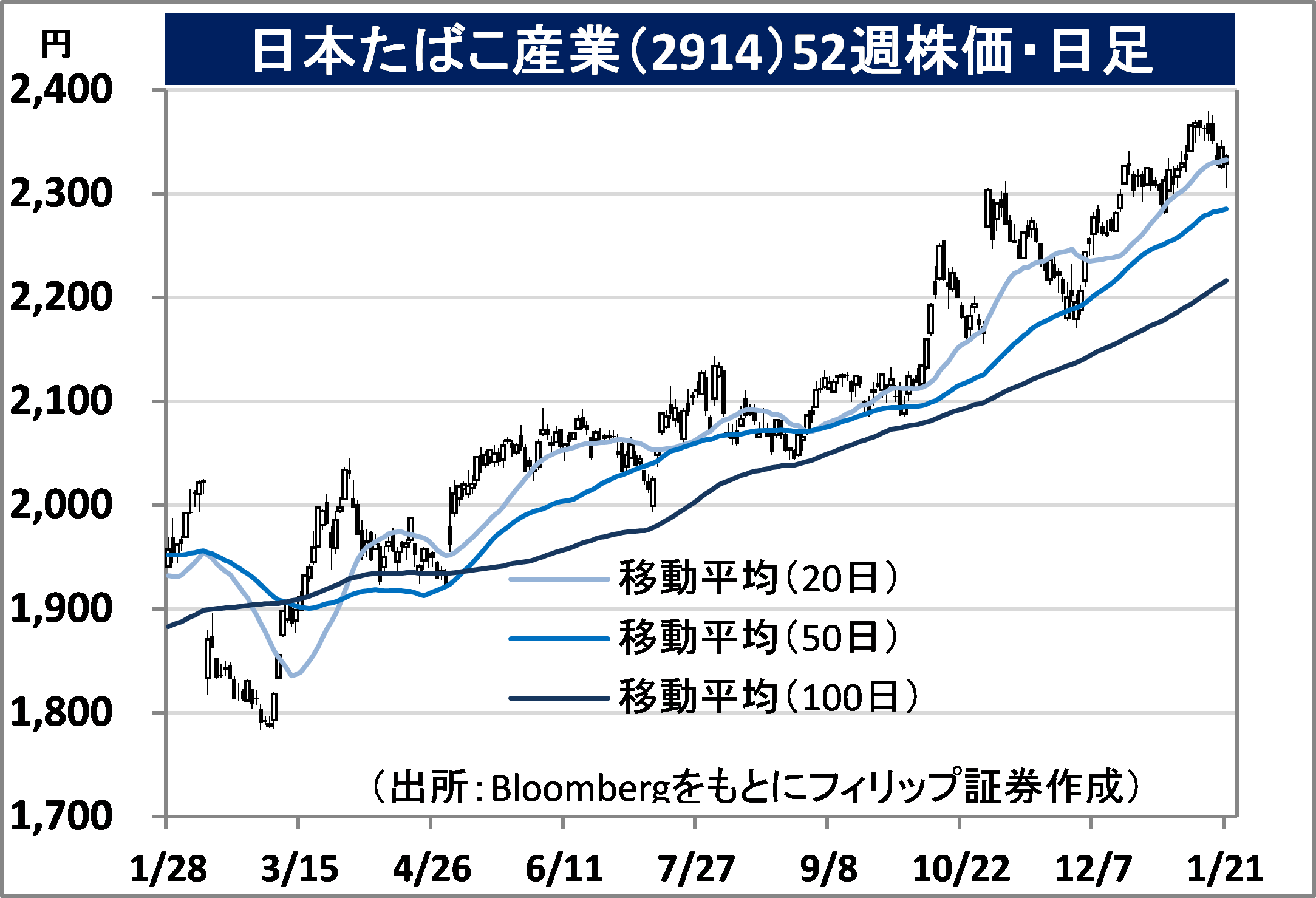

・Established in 1985. It was previously known as the Japan Tobacco and Salt Public Corporation. In addition to the mainstay domestic tobacco and overseas tobacco businesses, also proactively diversifying into pharmaceuticals, processed foods, etc. Acquired Katokichi (now TableMark) through TOB in 2008.

・For 9M (Jan-Sep) results of FY2021/12 announced on 29/10, sales revenue increased by 10.9% to 1.766 trillion yen compared to the same period the previous year, and operating income increased by 23.2% to 480.696 billion yen. Sales increased due to price hike and sales volume increase in overseas cigarette business. With the launch of Ploom X, sales of RRP (products that may reduce health risks associated with smoking) had also increased.

・Company has adjusted its full-year plan upwards. With the strong performance of the overseas tobacco and pharmaceutical businesses, company has increased sales revenue by 9.0% YoY to 2.28 trillion yen (original plan 2.20 trillion yen) and operating income by 1.9% to 478.0 billion yen (original plan 402.0 billion yen), while reducing the annual dividend by 14 yen to 140 yen (original plan 130 yen). TableMark, a wholly-owned subsidiary of the company and formerly known as Katokichi, is strong in udon noodles, which is the leading frozen food for household use by category, and packaged rice.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: