Report type: Weekly Strategy

“Bank of Japan Monetary Policy Meeting, high voltage DC transmission, TV stations.”

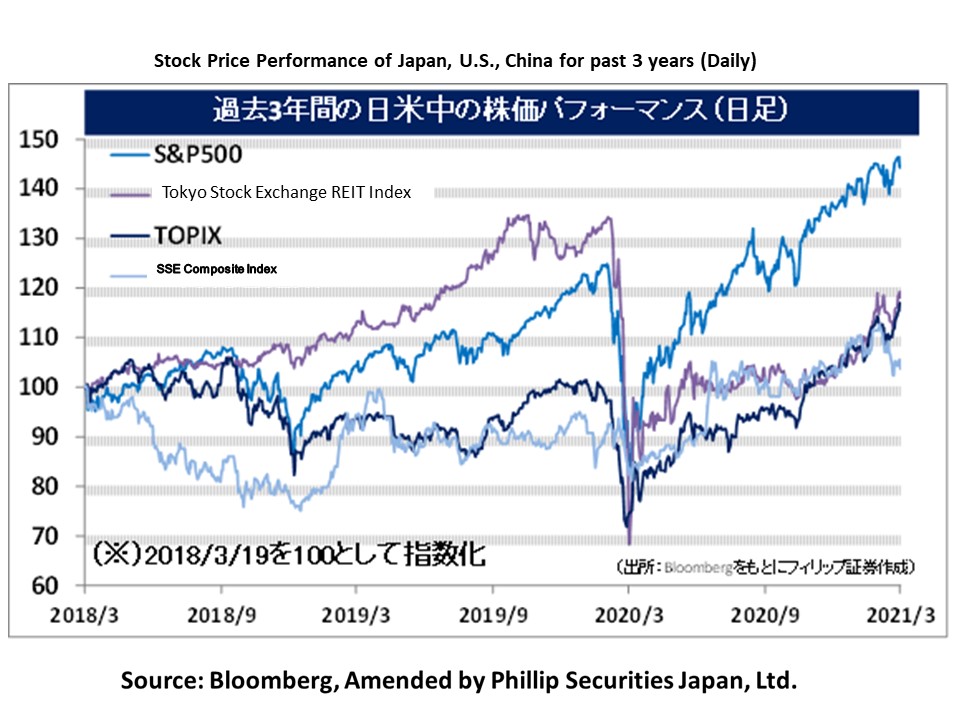

The BOJ decided at its Monetary Policy Meeting on 19/3 to raise the permissible range of fluctuation in the long-term interest rate for the yield on 10-year government bonds, which will continue to be pegged at around zero percent, to plus or minus 0.25 percent, instead of the previous 0.2 percent. It dropped “an annual 6 trillion yen” target for purchases of ETFs, while keeping the upper limit of annual purchase of 12 trillion yen. As for short-term interest rates, the application of a negative interest rate of -0.1% to the BOJ’s current account balance will remain unchanged, and earnings for financial institutions are expected to improve due to the widening gap between long- and short-term interest rates constituting the loan-deposit interest spread of financial institutions. In addition, the BOJ decided to purchase only TOPIX-linked ETFs, and on 19/3, the Nikkei Average fell from the previous day while TOPIX held steady, with bank and insurance stocks among others rising across the board. While the correction of low PBR (price-to-book value ratio) value stocks is likely to shift to the financial sector, high-priced stocks with high PBR which contribute more to the Nikkei Average are likely to be sold off.

It was reported that, in its effort to strengthen the power grid, which is a challenge for renewable energy power generation, the Ministry of Economy, Trade and Industry (METI) is considering installing offshore wind power transmission lines on the seabed using submarine cables, which are said to be less expensive than those used on land. In this regard, high voltage direct current (HVDC) technology is coming into the spotlight, as high voltage “direct current” with less power loss is suitable for long distance power transmission. In the HVDC market, in addition to Switzerland’s ABB, Germany’s Siemens, and the US’s GE, which have established DC power grids in Europe, we also have Toshiba (6502) and Mitsubishi Electric (6503). Together, these are the five dominant players globally in this field. Last year, Hitachi (6501) completed the acquisition of ABB’s power grid business and became the world’s top player in the HVDC sector. Sumitomo Electric Industries (5802) also has technology for DC submarine transmission cables used in HVDC, and has a business alliance with Siemens.

On 5/3, the Cabinet approved a decision to amend the Copyright Act to simplify the procedures for handling the rights of “simultaneous distribution,” whereby TV programs being broadcast are also streamed simultaneously on the Internet. This law is scheduled to go into effect in January, 2022. In addition to simultaneous distribution, “follow-up transmission” and “on-demand distribution” will also be covered. With the easing of regulations that required separate rights adjustment and processing for broadcasting and distribution, conditions are ripe for TV stations, that have been under pressure from a decline in terrestrial advertising revenue due to online advertising, to depend on TV program content sales and licensing revenue as their main source of revenue. Among Japanese stocks, IP (intellectual property) assets in the entertainment industry are highly valued overseas, which in some respect justifies the high PBRs of stocks of companies with IP. If the vast accumulation of IP assets such as TV program content from the past can be utilized on the Internet, it is unlikely that the current low PBR situation of related company stocks will continue.

In the 22/3 issue, we will be covering Iwatsuka Confectionery (2221), AEON REIT (3292), Rengo (3941), and Hitachi (6501).

・Established in 1947 in present-day Nagaoka City, Niigata Prefecture. Engaged in the rice cracker business, manufacturing senbei, arare, and okaki, all being various forms of rice crackers. Ranked third in Japan in the rice crackers sector. In terms of earnings, company is characterized by dividend income from Taiwan’s Want Want Group, in which it has invested and provided technical support.

・For 9M (Apr-Dec) results of FY2021/3 announced on 8/2, net sales increased by 1.8% to 16.995 billion yen compared to the same period the previous year, operating income increased by 60.7% to 384 million yen, and ordinary income increased by 18.5% to 3.099 billion yen. Dividend income, including stock dividends from Want Want Group, a diversified food manufacturer in which the company holds a 5% stake, rose 15.2% YoY to 2.626 billion yen.

・For its full year plan, net sales is expected to increase by 1.6% to 23.2 billion yen compared to the previous year, operating income to increase 2.1 times to 360 million yen, and ordinary income to decrease by 21.4% to 2.14 billion yen. Company’s shareholder special benefit program offers 1,000 yen worth of rice crackers for 100 shares or more, 2,000 yen worth for 200 shares or more, 3,000 yen worth for 500 shares or more, and 5,000 yen worth for 1,000 shares or more. For the month of March only, company is offering an additional 1,000 yen worth of benefits to shareholders who had continuously held at least 200 shares and are listed in the March shareholder registry for at least three consecutive times.

・A J-REIT sponsored by the AEON Group, a major retailer. Portfolio policy of at least 80% large-scale commercial facilities, up to 20% other commercial facilities, and up to 10% logistics facilities. Owns two commercial facilities overseas in Malaysia.

・For its FY2021/1 (2020/8-2021/1) results announced on 17/3, operating revenue increased by 0.7% to 17.701 billion yen compared to the previous period (FY2020/7), operating income increased by 0.3% to 6.802 billion yen, and distribution per unit increased by 1.9% to 3,184 yen. Acquired “AEON Ueda Shopping Center” in October last year with its own funds for 5.35 billion yen, increasing the asset size held to 395.5 billion yen.

・For FY2021/7 (Feb-Jul) plan, operating revenue is expected to decrease by 0.1% to 17.69 billion yen compared to the previous period (FY2021/1), operating income to decrease by 1.4% to 6.706 billion yen, and distribution per unit to increase by 0.5% to 3,200 yen. Company’s forecasted annual distribution yield through FY2022/1 at the closing price on 18/3 is 4.25%, and NAV (Net Asset Value) is 1.06x. Positioning as “lifestyle infrastructure assets” for local communities, company has secured stable rents through master lease contracts based on fixed rents with AEON Group companies.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: