Report type: Weekly Strategy

Attention on the Appreciation of the Dollar Against the Yen, Super Apps and Locusts

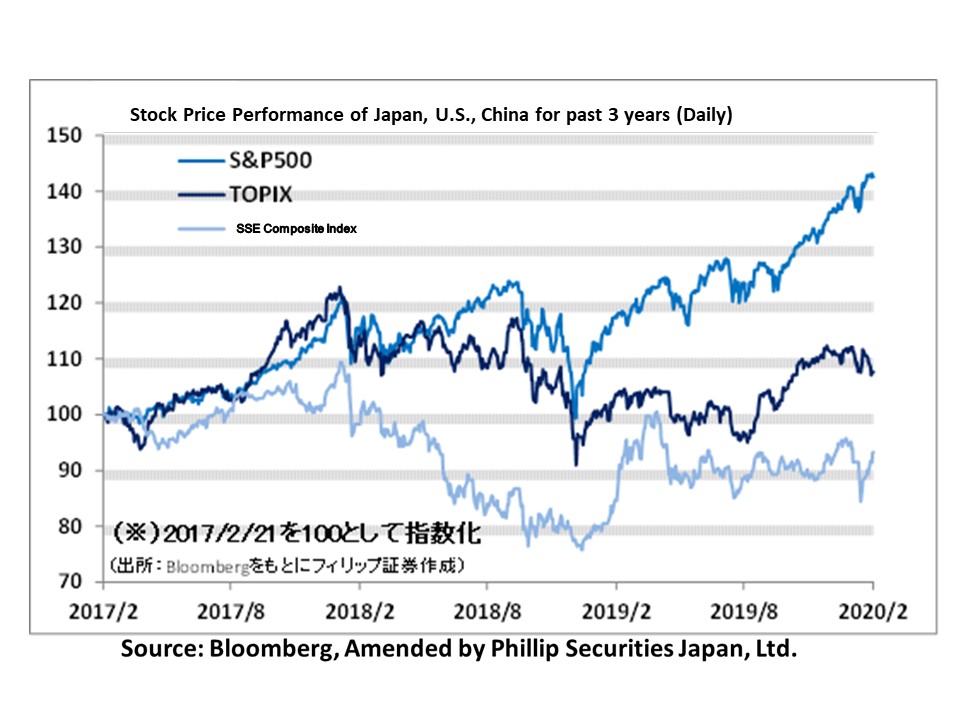

The dollar/yen exchange rate which had a closing price of 1 dollar to 109.86 yen in the NY stock market on 18/2 started showing movement after the end of the trading hours in Japan on 19/2 and rose sharply on 20/2 to 112.22 yen, which was last seen in Apr 2019. With the novel coronavirus infection spreading worldwide, there are indications of a change in the nature of the yen exchange rate, where the trend in the past was that it would be bought during a risk-off period in the same manner as the price of gold, leading to the yen appreciating against the dollar and the dollar appreciating against the yen during a risk-on period. Although this could be due to the supply and demand aspect where a “short squeeze” involving a stop loss occurred during an accumulation of large amounts of dollar selling positions at the 110 yen level, however, real GDP preliminary figures for the FY2019/10-12 period announced on 17/2 at -6.3% at an annualized rate conversion, along with criticism from abroad regarding the Japanese government’s countermeasures for infection on the cruise ship where a mass infection of the novel coronavirus took place, etc. were likely factors which easily led to “Japan selling”. On the other hand, perhaps another major factor was the sudden flow of investment funds to USD buying due to the U.S. economy showing no signs of a fall in pace even after entering February, such as the further increase from January in the Philadelphia Federal Reserve Manufacturing Index and the Federal Reserve Bank of New York’s Empire State Manufacturing Survey for February in the U.S. Although appreciation of the dollar against the yen is generally seen to be a result of a rise in Japanese stocks, despite the sharp appreciation in the dollar against the yen, the Nikkei average fell under 23,500 points after rising to 23,806 points on 20/2.

On 20/2, it was reported that MUFG Bank would be carrying out a capital and business tie-up with Singapore’s biggest ride hailing service Grab, which will invest up to 80 billion yen. It is said that they intend to expand by utilising the customer base of Grab and having joint businesses of financing or insurance via the smartphone app. With the growing importance of “Super Apps”, which offer various lifestyle-related services all in 1 app, we could be seeing manifestations of the sense of danger that businesses will not be able to survive without Super Apps. Grab has been contending with Gojek from Indonesia in the ASEAN region over the supremacy of Super Apps, while in Thailand, a capital business tie-up is being carried out by Siam Commercial Bank with Gojek and Kasikornbank with Grab. Also, in Japan, attention in the future will be on LINE, PayPay and Mercari / Merpay, etc. In addition, it is believed that AEON Mall (8905), which has been expanding across Asia, holds potential in the fintech area from the viewpoint of customer data utilisation.

As a result of unusual weather, there have been occurrences of large swarms of locusts in East Africa, India and Pakistan, which have led to tremendous damage to crops. With risks of climate change becoming apparent, we may have to consider the possibility of a string of unprecedented risks and dangers.

In the 25/2 issue, we will be covering Fuji Oil Holdings (2607), ITOCHU Advance Logistics Investment Corporation (3493), Ryoyo Electro (8068), and AEON Financial Service (8570).

・Established in 1950 via investment from ITOCHU (8001). Mainly carries out the manufacture and retail of oil and fat products, confectionery and bread making ingredients and products and soybean products. Is recognised for their unique technology such as the development of chocolate which does not stick even when touched.

・For 3Q (Apr-Dec) results of FY2020/3 announced on 4/2, net sales increased by 28.6% to 291.499 billion yen compared to the same period the previous year and operating income increased by 4.4% to 16.64 billion yen. Despite a decrease in operating income due to reasons such as the effect of cheaper currency in the procurement of ingredients from Brazil in their industrial chocolate business, there was an increase in operating income in the vegetable fat and oil business, the emulsified and fermented ingredients business and the processed soybean ingredients business.

・For its full year plan, net sales is expected to be 430 billion yen and operating income to be 25.5 billion yen. Rate of change compared to the previous period is undisclosed due to a change in the accounting period of overseas consolidated subsidiaries. In addition to reports that MOS Food Services (8153) is planning to release a 100% plant-based hamburger using a soybean-based meat substitute this summer across Japan as well as major meat manufacturers entering the household plant-based meat market, etc., we can expect growth in the soybean meat market which the company has been focusing their development in.

・Established in May 2018 then listed in Sep 2018. Is a distribution facility REIT sponsoring ITOCHU, which is strong in lifestyle consumption-related businesses that have a high affinity with distribution. Their flagship property is the “i Missions Park Inzai” in Chiba Prefecture.

・For FY2019/7 (Feb-Jul) results announced on 13/9, operating revenue increased by 32.1% to 1.718 billion yen compared to the previous period (FY2019/1), operating income increased by 9.9% to 810 million yen and distribution per unit including profit excess was 2,311 yen. i Missions Park Inzai and i Missions Park Moriya 2 were additionally acquired at 4.99 billion yen. Total acquisition price was 58.83 billion yen.

・For FY2020/1 period, operating revenue increased by 2.7% to 1.764 billion yen compared to the previous period (FY2019/7), operating income increased by 1.5% to 822 million yen and distribution per unit including profit excess increased by 2.4% to 2,366 yen. Predicted annual dividend interest based on the closing price on 20/2 is 3.78%. In addition to having their strength to be stable cash flow from tenants who are mainly clients of ITOCHU Group and the group itself, it is predicted that future expansion of e-commerce will support the demand of distribution facilities.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: