Report type: Weekly Strategy

“Annotations on Factors for the Plunge on the 14th, Ukraine Recovery Demand and Benefits of the Weak Yen”

In last week’s issue (12th September 2022 issue), we mentioned noting a trend in the Nikkei average where the market price has soared from around the “Major SQ” date in September since 2016 except in the presidential election year. Although the autonomous rebound (rebound) from the 8th last week prompted suspicions of a reoccurrence of that “anomaly” (a rule of thumb in the market that does not exactly have theoretical evidence), as a result of the U.S. Consumer Price Index (CPI) for August announced on the 13th surpassing market predictions, the closing price of the Nikkei average fell drastically by 796 yen on the 14th the following day compared to the previous day.

A clarification is certainly needed for this plunge. Firstly, prior to the U.S. FOMC (Federal Open Market Committee) on the 20th-21st next week, this was during a “blackout period” where policy members were prohibited from making statements based on monetary policy, and there was a greater likelihood of impact remaining in market participants on predictions of a significant interest rate hike of 1.00 points. Secondly, since Friday the 16th was a Special Quotation computation day involving the final settlement of futures and options of single stocks and the U.S. stock indices, and is a “U.S. version of the Major SQ” and a “quadruple witching”, we can consider that there was a greater likelihood of it linking with movements of relieving positions without carrying out a rollover (switching) to the forward month. If the extent of the policy interest rate hike at the FOMC is limited to 0.75 points, the Nikkei average along with the U.S. market is expected to regain stability.

There are concerns on a risk of global recession from reinforced monetary tightening by central banks, such as the U.S. FRB and the European Central Bank (ECB). On the other hand, in Ukraine, where there is ongoing military invasion by Russia, it was reported that the turnaround offensive attack by the Ukraine army has been growing stronger in the East and they have taken back control from Russia a region of more than 3,000 square kilometres since the start of September. If the offensive attack continues to grow stronger, infrastructure investment and development towards Ukraine’s recovery will start to move along, and we can likely expect it to absorb the pressure of recession that follows reinforced monetary tightening.

The Japanese government is working on adjustments in the direction of early easing from next month onwards to exempt short-term stay visas and allowing individual unrestricted travel along with scraping the maximum cap on the number of entrants to the country. Prior to the spread of COVID-19 in 2019, the dollar/yen exchange rate shifted within the 105-111 yen/dollar range. A rise is expected in inbound travel purchasing power per person at the current 140 yen/dollar level.

In order to cope with the advancing depreciation of the yen, movements have emerged in transferring production carried out in China factories to Japan factories, such as the household goods Iris Ohyama. In overseas enterprises as well, in addition to the American biotechnology Moderna looking to supply the COVID-19 vaccine to China and considering production facilities in Japan, the American aircraft manufacturer Boeing is setting up a next-gen aircraft research and development base in Nagoya City, etc. There is a noteworthy rise in Japan’s importance.

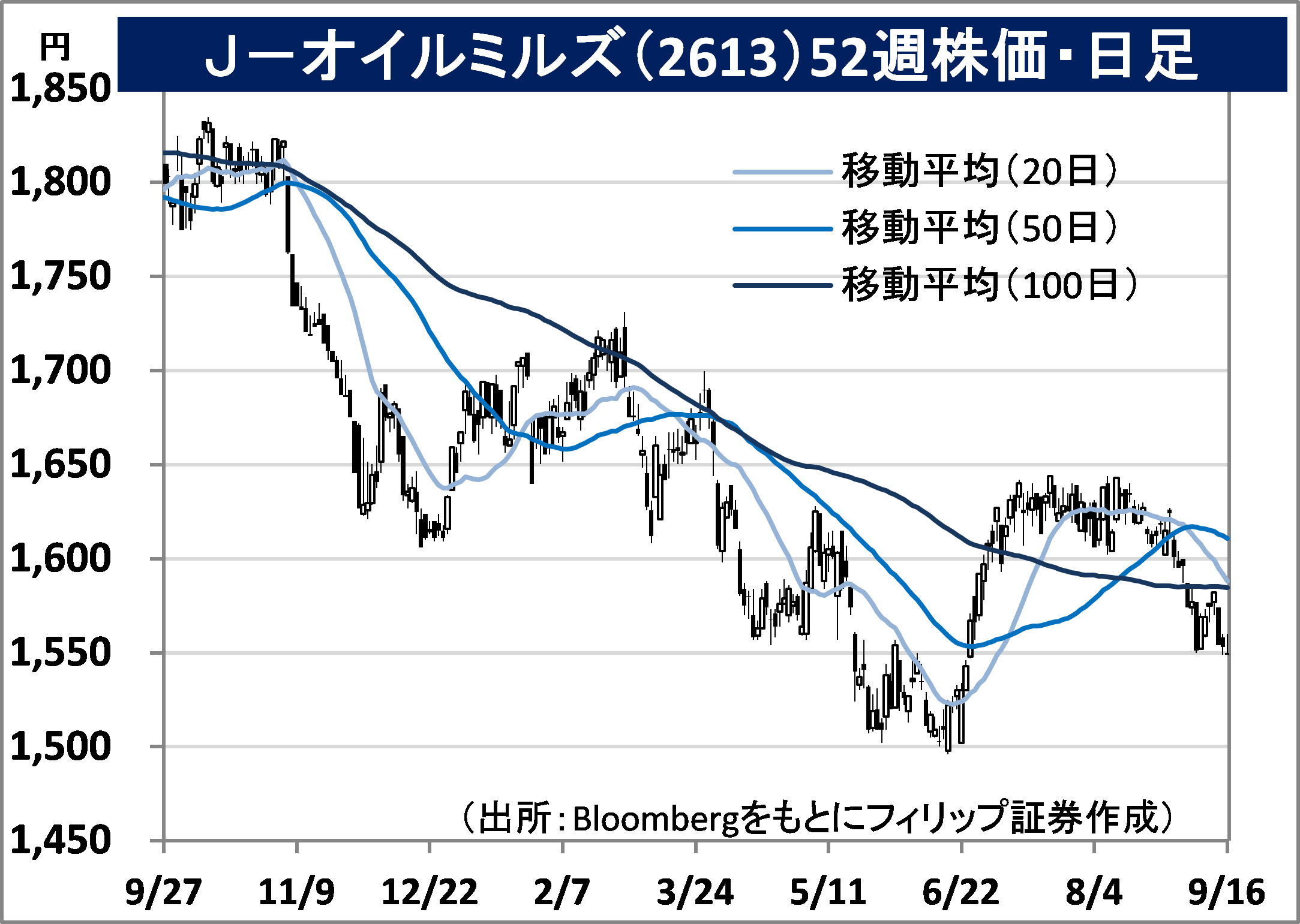

In the 20/9 issue, we will be covering J-Oil Mills (2613), F&M (4771), Shiseido Company (4911), and Japan Exchange Group (8697).

・Honen and Ajinomoto Oil Mills integrated in 2002. Mainly operates the specialty food business that involves the food materials section and the dairy PBF section such as margarine, as well as the oil and fat business that involves the meal (oilseed) section and the commercial and industrial oil and fat section.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 5/8, net sales increased by 30.0% to 60.017 billion yen compared to the same period the previous year and operating income returned to profit from (210) million yen the same period the previous year to 711 million yen. Despite skyrocketing raw material prices in the oil and fat business, the increase in retail prices was successful and net sales increased by 36.5% to 54.487 billion yen and segment profit returned to profit from a deficit the same period the previous year to 1.068 billion yen.

・For its full year plan, net sales is expected to increase by 29.0% to 260 billion yen compared to the previous year, operating income to return to profit from (21) million yen the same period the previous year to 1 billion yen and annual dividend to have a 30 yen dividend decrease to 20 yen. Skyrocketing raw material prices due to the depreciation of the yen and the sharp drop in the export of sunflower oil and rapeseed following Russia’s invasion of Ukraine will be absorbed by revised retail prices. In addition to a decline in raw material costs from Ukraine’s recovery, we can likely expect sales expansion of high value-added products involving plant-based PBF (plant-based foods).

・Established in 1990. Operates accounting services, such as accounting agency for small-scale enterprises and sole proprietors, etc., general consulting for small and medium-sized enterprises, support in obtaining ISO certification and tax and finance consulting (TAXHOUSE), etc.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 29/7, net sales increased by 31.2% to 2.753 billion yen compared to the same period the previous year and operating income increased by 83.7% to 484 million yen. For revenue by business segment, there was growth with accounting services increasing by 6% to 790 million yen, consulting increasing by 43% to 1.411 billion yen and business solutions increasing by 62% to 468 million yen.

・For its full year plan, net sales is expected to increase by 18.7% to 12.911 billion yen compared to the previous year, operating income to increase by 19.4% to 2.677 billion yen and annual dividend to have a 4 yen dividend increase to 34 yen. With telecommuting becoming the norm, the ban on the transfer of salaries via digital money using smartphone apps, etc. is predicted to be lifted in Spring ’23. With the burden involved with the work in issuing payslips in corporate labour and general affairs sections becoming an issue in corporate management, there will likely be attention on the company’s web payslips, the “office station payslips”.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: