Report type: Weekly Strategy

“An Unexpectedly Strong Backdrop Involving the Japanese Stock Market and Abundant Source Material for Stocks to Buy”

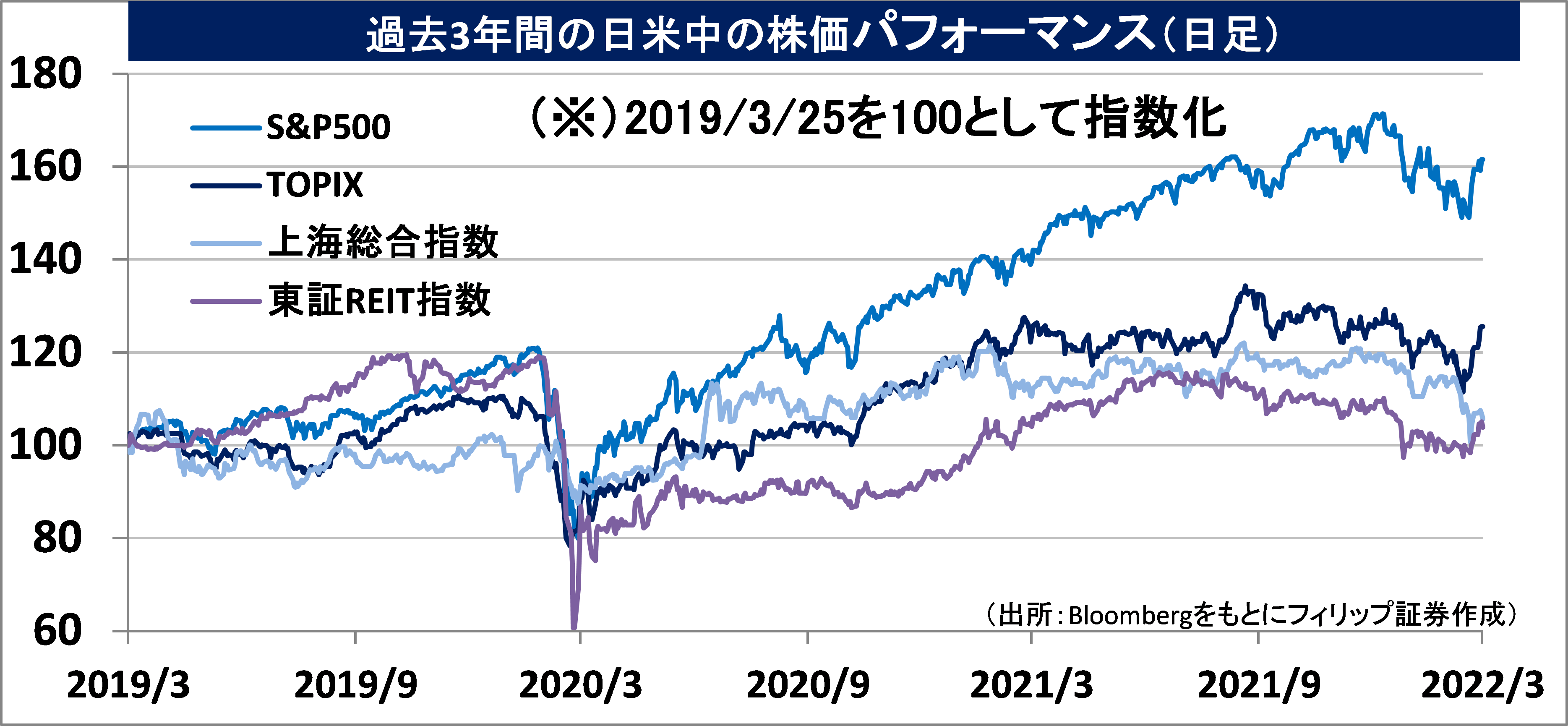

With there being no improvement in the situation involving Russia’s invasion of Ukraine, the Nikkei average reached 8 consecutive white candlesticks up to 15-24/3 (consecutive daily where the closing price is higher than the opening price), which was an increasing price range of 3,657 points in 12 business days from the low of 24,681 points since November 2020 that was marked on the 9th up to 28,338 points on the 25th. This was a strong change last since the record of the increasing price range of 3,841 points in 18 business days between 20/8 to 14/9 last year ahead of the Liberal Democratic Party’s Presidency.

A major factor for this was that various positive circumstances had aligned, such as expectations of economic normalisation after the end of the semi-emergency coronavirus measures to handle COVID-19, an improvement in demand right after the final date involving margin transactions at the high price in September last year, and to receive dividend rights before the end March settlement date. What ought to be highlighted amongst these is the increasing relative appeal of the Japanese stock market that has low inflation and a consistent quantitative easing policy by the Bank of Japan. We can consider the backdrop for it to be the U.S. FRB deciding to increase the interest rate by 0.25 points on 16/3 and an increase in opinions in the market that predict monetary tightening and increased interest rates of a hawkish pace that will greatly exceed the interest rate increases in 3 years from December 2015 the previous round based on the perspective of reinforced inflation curbs. We can say that this is a turn of market events which was mentioned exactly in the “inflation-evasion money Japan buying”, which is perceived to be the biggest factor for a rise in stock prices in the “2022 Stock Market Forecast” in the 27th December 2021 (year-end special) issue of our weekly report.

In actuality, from the perspective of global stock investment, while considering the possibility of European and Chinese stocks having a higher priority as investment targets aside from U.S. stocks, Europe has had a drop in priority based on concerns of losses related to Russia and skyrocketing energy prices following the drawn-out and worsening Ukraine situation. China, which also has expectations of monetary and regulation easing, has gone against global trends of opening borders and ending COVID-19 restrictions that are supported by a decrease in risks of infection severity due to vaccination being commonplace, and is continuing to enforce a strict “zero COVID-19 policy”. Based on delays in economic normalisation, their priority appears to have fallen. Thus, through the method of elimination, it is likely more apt to say that Japan has risen in priority.

In terms of Japanese stocks to buy, we can consider the expectations on those related to inbound demand from economic resumption which follow the “opening of Japan”; those related to plants, such as natural gases, energy and fertilisers, etc. which will be recipients of the demand involving alternatives from exiting Russia; the call on stable power supply, such as the resumption of operation of nuclear power due to a cut in thermal power from the earthquake that had its epicentre in offshore Fukushima; and those related to nuclear bomb shelter works as a result of North Korea’s ICBM (intercontinental ballistic missile) firing tests. Also, with regard to the Revision on the Law Concerning the Preservation of National Tax Records in Electronic Form (with a 2-year grace period) enforced in January this year, an increase in demand is also expected for cloud accounting software companies, such as OBIC Business Consultants (4733), which was covered in last week’s “Selected Stocks”.

In the 28/3 issue, we will be covering Sourcenext (4344), The Japan Steel Works (5631), Toyo Engineering (6330) and Dai-ichi Life Holdings (8750).

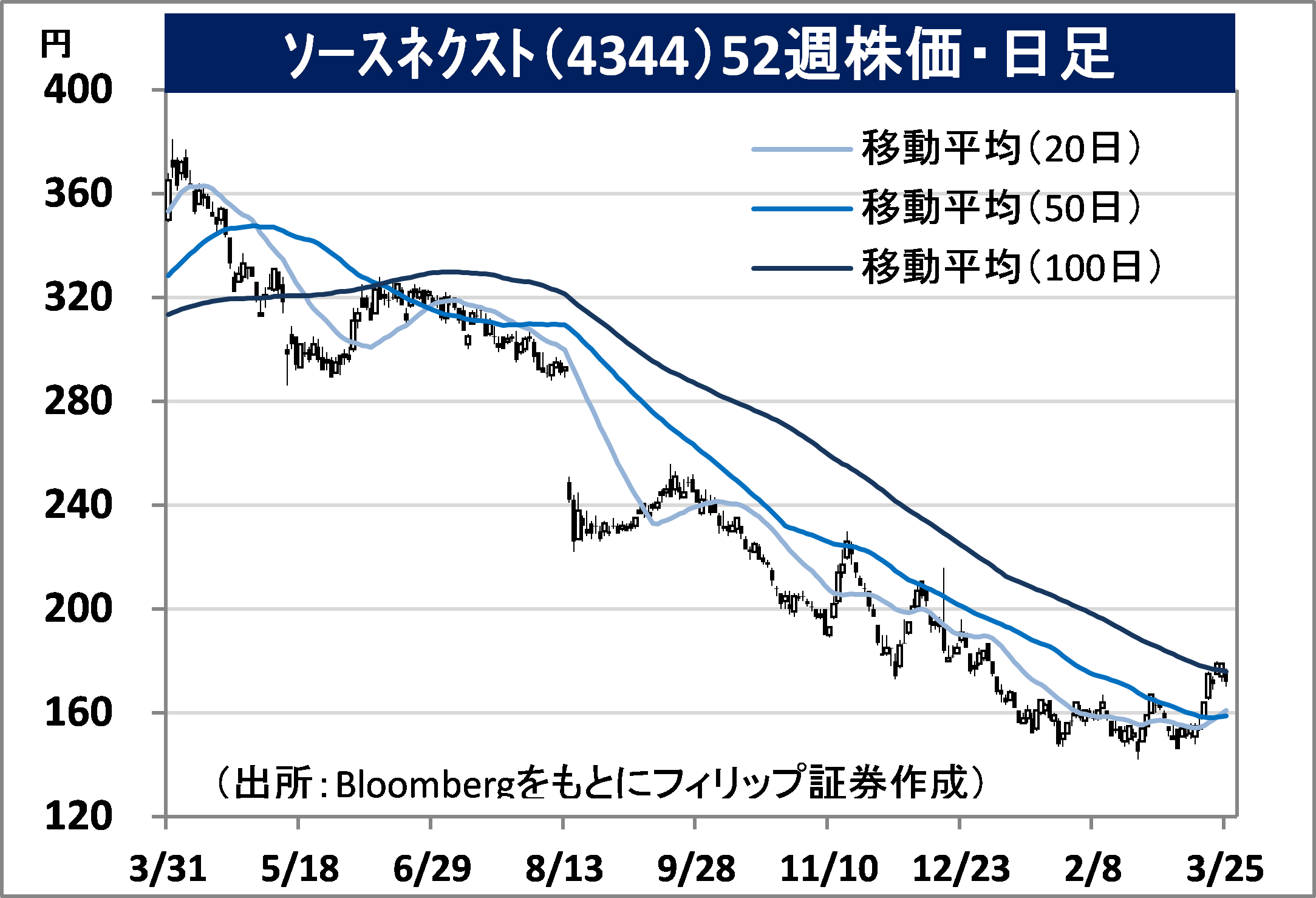

・A PC software, smartphone app and hardware development and retail corporation that established in 1996. In addition to their mainstay machine translation “Pocketalk”, they are famous for the “ZERO” series security measures software and postcard software, such as “Fudemame” and “Fudeo”.

・For 9M (Apr-Dec) results of FY2022/3 announced on 14/2, net sales decreased by 18.0% to 7.8 billion yen compared to the same period the previous year and operating income fell into a deficit from 446 million yen the same period last year to (920) million yen. For their mainstay Pocketalk, despite a 3.5 times increase in retail units in the U.S., an extinguished demand for inbound business operators and foreign travellers in Japan following the COVID-19 disaster have affected.

・Company revised its full year plan downwards. Net sales is expected to decrease by 18.4% to 10.492 billion yen compared to the previous year (original plan 15.05 billion yen) and operating income to fall into a deficit from 540 million yen the previous year to (1.769) billion yen (original plan +104 million yen). Although there has been a revision to their original plan of a recovery in inbound and overseas travel demand from December onwards, their policy is to strengthen development investment. With inbound demand recovery holding the key to business performance, they launched “Pocketalk Subtitles” in September last year, which instantaneously translates and displays in remote meetings.

・Established in 1907. Their main businesses are the “industrial machines business”, such as resin manufacture / processing machines and moulding machines, and the “processed materials and engineering business”, such as cast and forged steel products, clad steel plates and steel pipes, etc. They are a global cast and forged steel giant for thermal and nuclear power.

・For 9M (Apr-Dec) results of FY2022/3 announced on 7/2, net sales increased by 5.2% to 147.041 billion yen compared to the same period the previous year and operating income increased by 15.9% to 10.13 billion yen. In addition to sustained recovery in facility investment focusing on home appliances and electric vehicles (EV) in the industrial machines business, it has performed strongly for the most part in the processed materials and engineering business, such as sustained stable demand in cast and forged steel products.

・Company revised its full year plan downwards on 22/3. Net sales is expected to increase by 9.0% to 216 billion yen compared to the previous year (original plan 216 billion yen) and operating income to increase by 46.7% to 15 billion yen (original plan 16 billion yen). Impact from the semiconductor supply shortage and a delay in facility investment recovery in the automobile field is predicted. On the other hand, annual dividend has increased by 20 yen to 55 yen (original plan 45 yen). The company’s cast and forged steel products boast a staggering share in nuclear reactor pressure vessels, and they are expected to benefit during the resumption of operation of nuclear power.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: