|

Report type: Weekly Strategy

|

”An Increased Shift From Growth to Value”

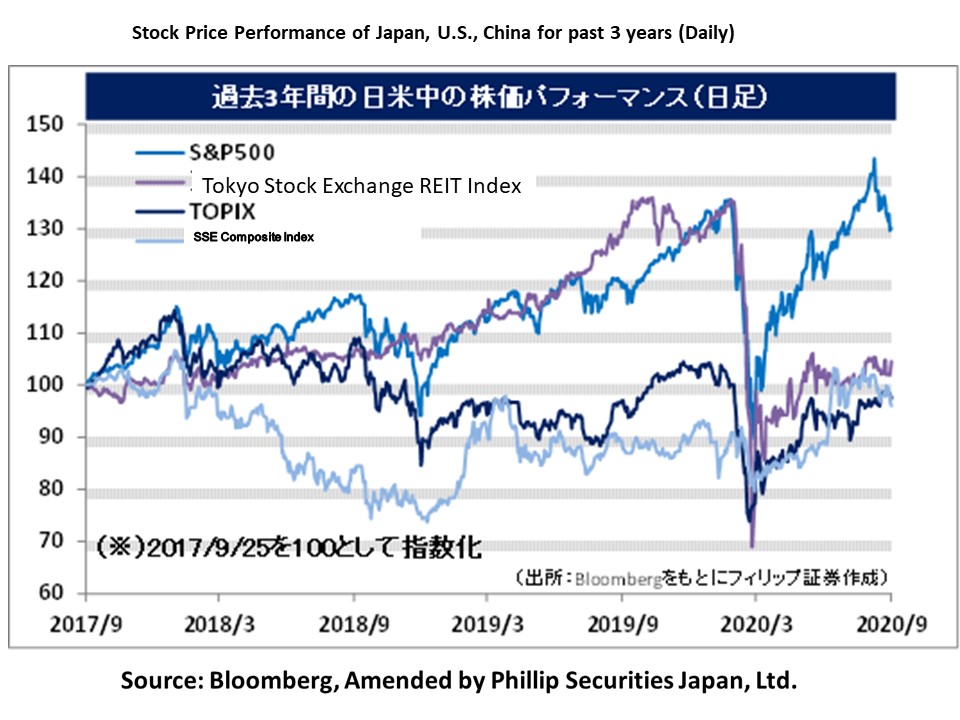

In the 23rd September 2020 issue of our weekly report, we mentioned about the possibility of buyback pressure weakening before the new selling date settlements for system margin trading as a result of the end of 4-day holiday having passed the half year mark since the Nikkei Stock Average’s year low on 19/3, however, Japanese stocks outstripped the bearish U.S. stock market with the Nikkei Stock Average remaining strong without falling under 23,000 points. This is thought to be largely due to the fact that it was supported by the purchasing demand towards the last day before the ex-dividend date that had its base date in end September.

However, this does not always mean that stocks with high company forecasted dividend yield are always bought. Even amongst stocks with top forecasted dividend yield in the Nikkei Average High Dividend Yield Stock 50 Index, the stocks bought on 23/9 were those from industries such as trading companies, insurance, electrical equipment and communications, whereas stocks such as Japan Tobacco (2914), which had the top forecasted dividend yield, and those from industries such as banking and petroleum fell compared to the previous day. While there are movements across the world of a start of a portfolio shift from growth stocks mainly involving major high-tech stocks to undervalued value stocks, on the other hand, there are also movements where there is a particular avoidance for deep value stocks that are undervalued. Deep value stocks are regarded as stocks that fall under mature industries, such as energy or the conventional type of banks, etc. It is likely that attention will be on the fact that distinctive movements are growing stronger even amongst stocks that have high forecasted dividend yield.

UBS Asset Management predicts that the emergency approval for 1-3 types of COVID-19 vaccines would be obtained within the next few months, and the vaccine announcement will result in greater forecasts of a recovery in earnings in corporations other than those benefitting from work from home, such as high-tech stocks. They also indicated that the anticipation of the vaccine will encourage investment in other sectors or regions that easily benefit from a normalisation of the economic cycle. Also, regarding the Tokyo Olympics which is being postponed to next year, John Coates, the Coordination Committee Chairman of the International Olympic Committee (IOC) expressed on 7/9 that “the Olympics will likely be held regardless of whether there is a spread of COVID-19. It will be opening on 23rd July next year”, in addition, based on the fact that international sports meets were held in North America, which was faced with a severe spread of the virus, President Bach displayed confidence that the Olympics would be held, saying that “it can be safely held even without a vaccine”. The anticipation of the Olympics being held is related to the expectation of a climate boost in the Japanese economy, and at the same time, can also turn out to be strong factor that would push the shift from growth to value.

However, regarding the immediate global economy, even by looking at the change in various commodity prices, there is a need to be careful of the possibility of it hitting a peak in the temporary recovery of the economy up to August, in addition to the fact that it is becoming difficult to see further improvement in the economy for the time being due to the resurgence of a spread of COVID-19 in Europe.

In the 28/9 issue, we will be covering Fujifilm Holdings (4901), Bunka Shutter (5930), Nissha (7915), and Sankyo Frontier (9639).

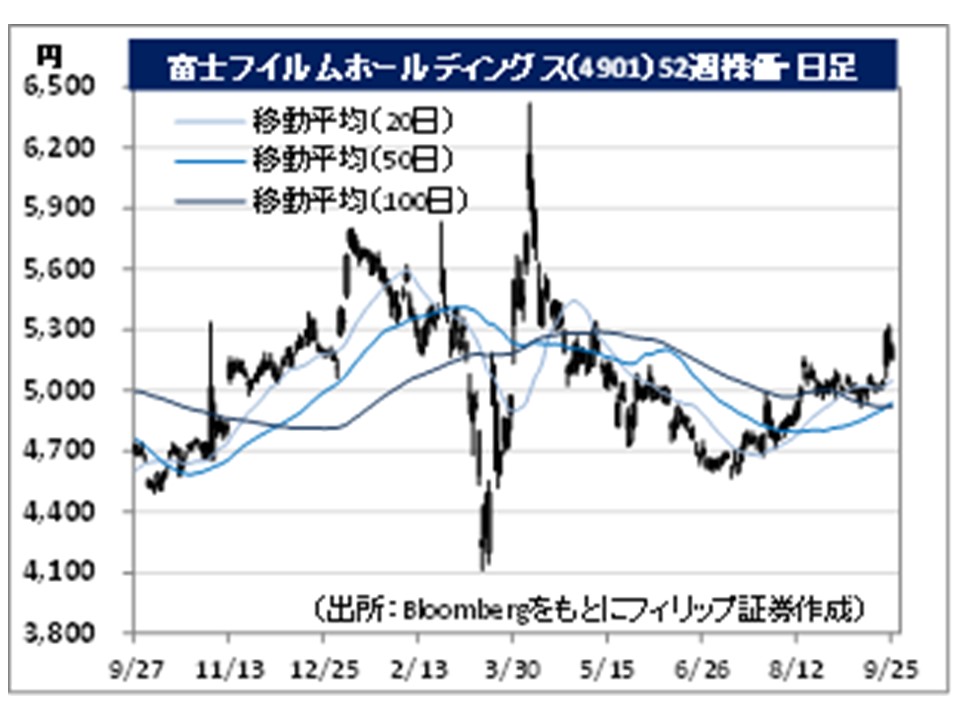

・Established in 1934. Expands 3 businesses, which are imaging solutions involving photographs and images, healthcare & material solutions involving the health of people (prevention, diagnosis and treatment) and document solutions.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 13/8, net sales decreased by 14.8% to 456.27 billion yen compared to the same period the previous year and operating income decreased by 45.1% to 20.39 billion yen. Due to the impact of the regulations on going outdoors and the closure of stores following the COVID-19 catastrophe, the decrease in sales, such as camera products, etc. had affected. Due to the conversion of Fuji Xerox to a wholly-owned subsidiary, net income increased by 87.6% to 27.501 billion yen.

・For its full year plan, net sales is expected to decrease by 5.0% to 2.2 trillion yen compared to the previous year and operating income to decrease by 25.0% to 140 billion yen. Excluding the impact from the COVID-19 catastrophe and foreign exchange as well as temporary expenses for a structural reform, there has been an increase in income and profit compared to the previous year. Their subsidiary, FUJIFILM Toyama Chemical, achieved the primary endpoint in phase III domestic clinical trials for Avigan, a candidate for the cure for COVID-19. Attention is on the application for the approval to manufacture and sell Avigan that is planned for mid-October

・Established in 1955. Their main business content involves the manufacture and retail as well as the maintenance/inspection and repair of building materials for buildings and housing, shutters, and housing renovation. Company is currently strengthening their water stop business which handles facilities for flood prevention as a countermeasure for guerrilla rainstorms.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 4/8, net sales increased by 1.3% to 37.197 billion yen compared to the previous period and operating income increased by 6.0 times to 410 million yen. A revenue increase in their mainstay shutter-related products and building materials-related products businesses, as well as the operating profit or loss for the building materials-related products business coming out of deficit from (380) million yen the same period the previous year have contributed to their business performance.

・Their full year plan is undecided due to the present difficulty in reasonably calculating the impact of COVID-19. Apr-Jun net sales for their “other businesses”, which include their water stop business that handles flood prevention facilities, increased by 1.5% compared to the same period the previous year. With concerns of flood damage, such as from the occurrence of the heavy rain in Kyushu in July this year and the extremely large-scale and strong Typhoon Haishen which approached Kyushu in Sep, there will likely be expectations for an increase in the social reputation of the company’s businesses

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: