|

Report type: Weekly Strategy |

“An Appreciation of the Dollar Against the Yen Since 24 Years Ago and a Currency Crisis, Strong Performance of the Financial Statements Statistics of Corporations by Industry”

The appreciation of the dollar against the yen in the dollar/yen exchange rate has accelerated, exceeding 140 yen/dollar on the 1st last since 24 years ago in August 1998. Judging from the U.S. Dollar Index which indexes the value of the U.S. dollar against multiple major currencies, such as the euro, yen, pound and Swiss franc, after stopping at the first half of the 100 point mark in ’98, it rose to over 120 points in 2001-02. Following the further increase in the U.S. dollar index to 109.59 points at the closing price on the 1st, it appears that there is still a possibility of a further rise in the dollar/yen exchange rate.

Let us look back 24 years ago. In 1998, the “Asian financial crisis”, which occurred mainly in Thailand from July a year before and extended to Latin America which then extended to the Russian financial crisis in August of the said year, etc., was a period where the currencies of developing countries, where their exchange rates were in effect linked to the U.S. dollar, were being sold off drastically. A major hedge fund (Long-Term Capital Management) went bankrupt as a result of the Russian financial crisis. In that August, the dollar/yen exchange rate advanced to an appreciation of the dollar against the yen until the 147 yen/dollar mark.

Even in Japan, the Long-Term Credit Bank of Japan and the Nippon Credit Bank fell into bankruptcy, and based on the Act on Emergency Measures for the Revitalisation of the Financial Functions and the Act on Emergency Measures for Early Strengthening of Financial Functions, which were passed and formed in October by the finance Diet, both banks were nationalised as special public management banks. In the midst of this, 3 months after the dollar/yen exchange rate marked the high of the 147 yen mark, the dollar fell sharply and the yen rose sharply to around 110 yen.

If there is rapid progression in the appreciation of the dollar against the yen and in the rise of the U.S. dollar interest rate, it would bring about financial difficulties in developing countries which have procured large funds of debts in U.S. dollars, which will suggest a greater possibility of them falling into a currency crisis. In Europe as well, there is a possibility that a significant increase in interest rate of 0.75% points will be carried out by the European Central Bank (ECB) on the 8th to curb inflation. In that case, linking the increase in the disparity (market segmentation) between Germany’s government bonds and southern European countries’ government bonds, such as Italy, also leaves a risk of exposing the structural vulnerability of the euro.

The environment surrounding Japanese enterprises as of late is not bad. According to the Financial Statements Statistics of Corporations by Industry for the Apr-Jun period announced on the 1st by the Japanese Ministry of Finance, capital investment (excluding seasonal fluctuation) increased since 2 quarters ago by 3.9% compared to the previous quarter. In particular, there are plans for proactive investment in the manufacturing industry in FY22 focusing on large enterprises, such as growth by a 7.6% increase. Ordinary income renewed its record high by a 17.6% increase to 28.3183 trillion yen compared to the same period the previous year. Net sales also had an increase in revenue for 5 consecutive quarters with a 7.2% increase.

The Tokyo International Conference on African Development (TICAD) was held in Tunisia on 27-28/8 and Prime Minister Kishida expressed online a policy of contributing a scale of a total of 30 billion dollars in the public and private sectors in the next 3 years “in Africa, which is said to account for 1 of 4 of the world’s population in 2050 and is a continent that is young and full of hope in which dynamic growth can be anticipated”. Also, rapid progress in the “frozen food economy”, such as the recent increase in floor space of the household frozen food section, etc., could turn into an investment chance.

In the 5/9 issue, we will be covering Nichirei (2871), NPC (6255), NSK (6471), and Yamaha Motor (7272).

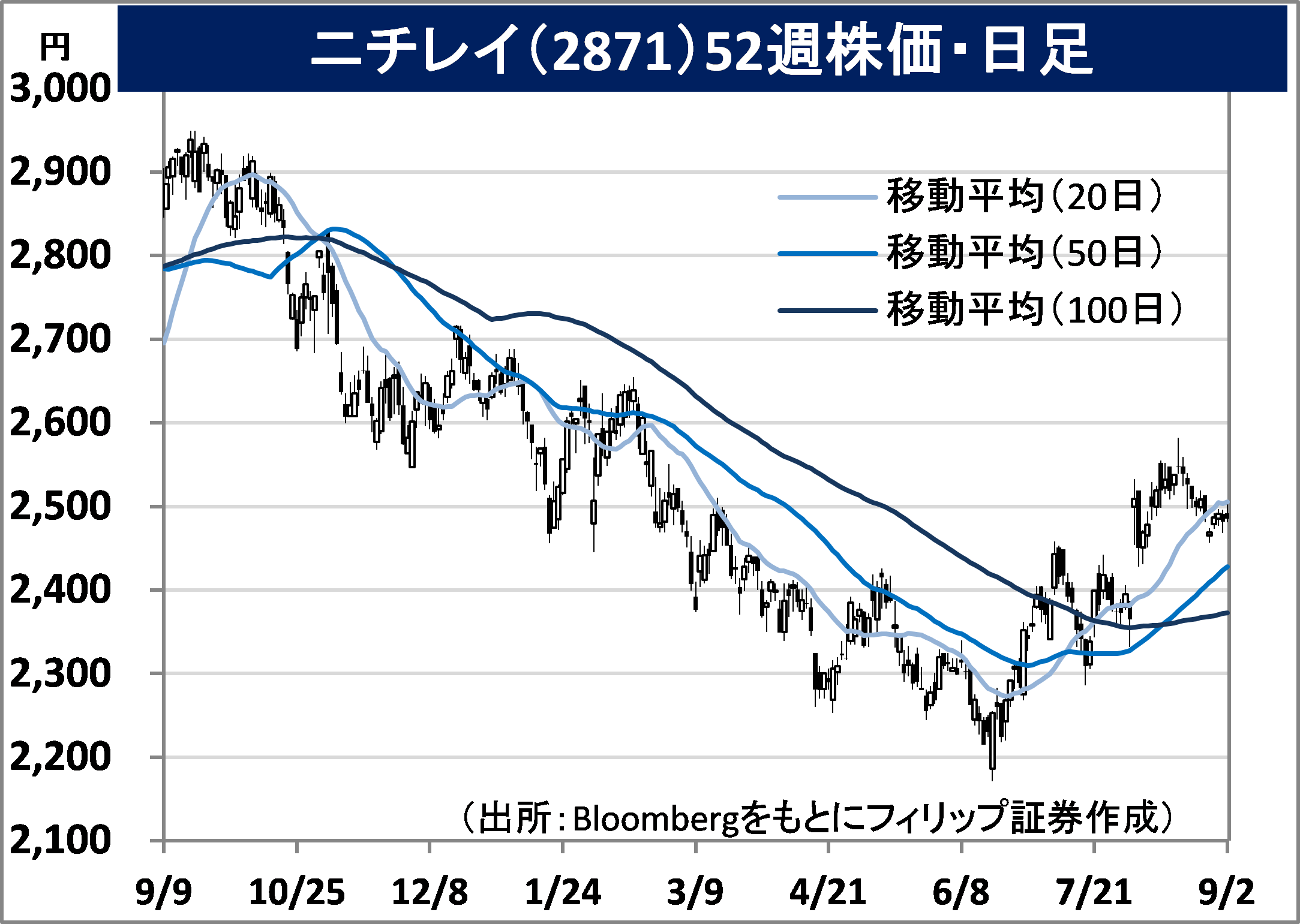

・Established based on the fisheries control ordinance in 1942. Mainly operates the processed food business, fisheries business, livestock business, low temperature distribution business and the real estate business. In addition to them being the top in cold storage warehouses and frozen food, they are currently expanding low temperature distribution with a focus on Europe.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 2/8, net sales increased by 8.6% to 156.057 billion yen compared to the same period the previous year and operating income decreased by 5.3% to 6.677 billion yen. While their mainstay processed food business had a 11.9% revenue increase and the low temperature distribution business had a 7.5% revenue increase which contributed to an overall increase in net sales, skyrocketing electric power costs and raw material and supply costs, etc. have affected, which led to a decrease in operating income.

・Its full year plan was revised upwards. Net sales is expected to increase by 5.0% to 633 billion yen compared to the previous year (original plan 618 billion yen). Operating income is to increase by 0.3% to 31.5 billion yen and annual dividend to remain unchanged with a 2 yen dividend increase to 52 yen. With the company having its strengths in croquettes and fried rice in household frozen food, for production volume in Japan by item in ’21, they were 2nd for croquettes (1.1% increase compared to the previous year) and 3rd in fried rice (1.1% increase). There have been movements one after another on the expansion of floor space for the household frozen food section in supermarkets.

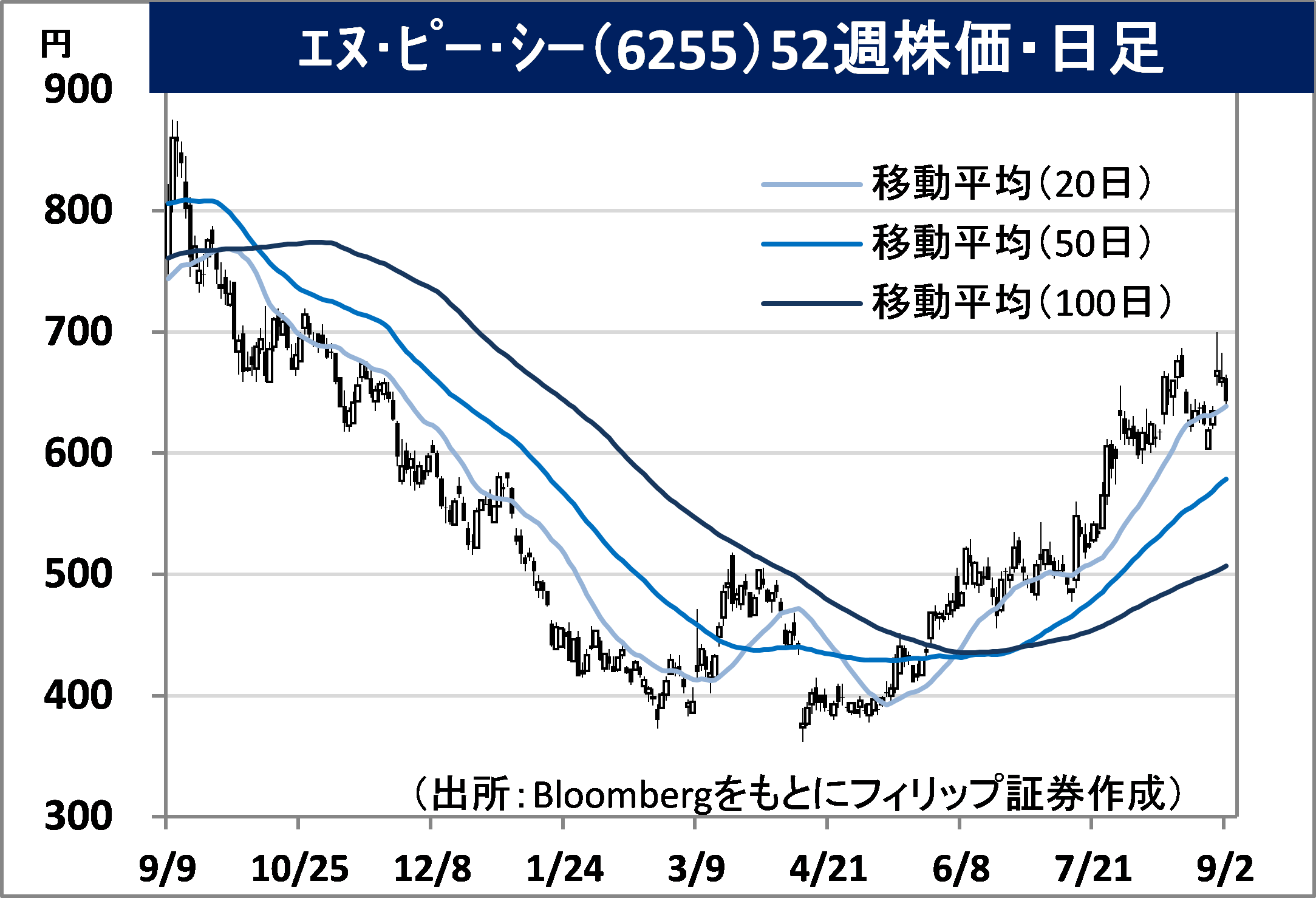

・Established in 1992 based on the vacuum packaging machine business. Currently manages the device-related business involving FA devices geared towards the solar cell / automobile / display / electronic components industries, etc., and the environmental-related business which includes solar panel inspection to disposal.

・For 9M (Sep-May) results of FY2022/8 announced on 13/7, net sales decreased by 43.7% to 4.045 billion yen compared to the same period the previous year and operating income decreased by 60.9% to 510 million yen. In addition to a postponement in the record of sales following the change to long delivery times and component shortages, such as in electrical components, machine components and processed goods, etc., its overlap with the change in on-site work schedules due to the full operation of client factories, etc. have affected.

・For its full year plan, net sales is expected to be 4.454 billion yen (5.217 billion yen the previous year before the application of the accounting standard for revenue recognition), operating income to be 368 million yen (691 million yen the previous year) and annual dividend to remain unchanged compared to the previous year at 2 yen. A downward revision was announced on 12/4. In response to the conclusion of the “expenditure and revenue act” in the U.S. which incorporates incentives in renewable energy, the company’s key client, the American solar panel manufacturer First Solar (FSLR), announced an investment of up to 1.2 billion dollars in new factory construction.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: