The Trump administration announced that it would invoke the third round of additional tariffs on imported goods from China equivalent to 200 billion dollars on 9/24. However, the additional tax rate was reduced from the originally expected 25% to 10% for the rest of the year (planning to increase to 25% by year-end). For the time being, pessimistic scenarios are retreating as pressure on China is expected to be reduced.

Meanwhile, China announced that it would impose retaliatory additional tariffs with effect from 12.01pm on 9/24 on imported goods originating from the US equivalent to 60 billion dollars. However, China is expected to impose lower additional tax rates on many items such as LNG, compared to those announced on 8/3. In addition, the Chinese government has raised the rate of reimbursement of export value-added tax for certain items since 9/15. This appears to be a measure to mitigate the impact of the trade friction on companies exporting from China.

Furthermore, according to some reports, China is planning to lower average tariff rates on imports from most trading partners from October. This is expected to reduce the burden on Chinese consumers and foreign companies. While the impact on goods imported from the US is not clear, this action can be considered as an effort by China to open up its market, and also as a move toward relaxation of trade friction. It seems like a message to maintain the “reform and open-door policy” geared towards both the domestic and overseas audience. On top of the tariff reduction and with the trade friction with the US intensifying, on 9/19, Premier Li Keqiang said that “the RMB will not be devalued for the purpose of improved export competitiveness”, denying that there were deliberate manipulations of the forex. He explained that “unilateral depreciation will only bring more harm rather than benefits to the Chinese economy”. We believe this is indeed comforting news for market participants.

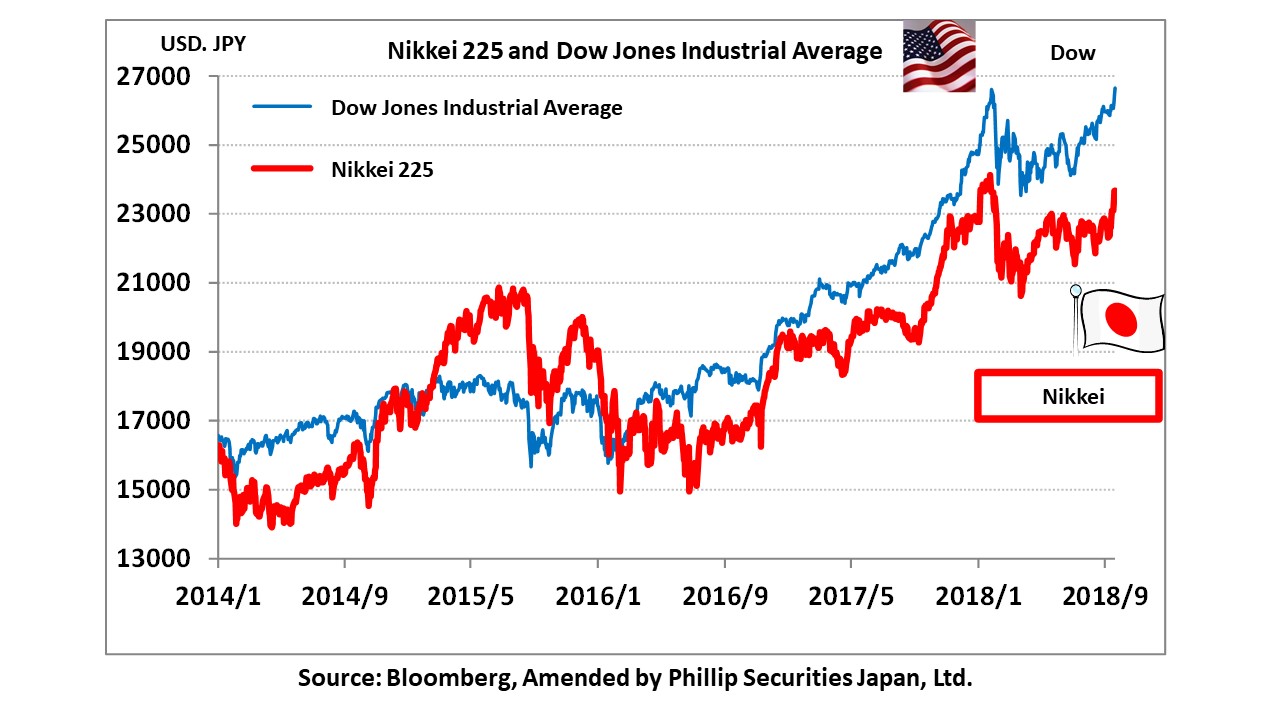

In the US, the prices of stocks connected with China, such as Caterpillar (CAT), which had suffered sell-offs since the beginning of the year, have lately been rising continuously, and the NY Dow and S&P500 have both been achieving new highs.

Stock prices of Yaskawa Electric (6506), Hitachi Construction Machinery (6305) and Komatsu (6301), which had been heavily sold since the beginning of the year, had also increased sharply. The Nikkei average had 6 continuous winning streaks as of 9/21, rising 1,265 points (5.6% rise) during the period. However, this optimistic scenario seems to be losing steam, and there is also a feeling of overheating in the market from the RSI and Up-down ratios. There is no denying the possibility of negative outcomes from the US-China, US-Canada NAFTA and US-Japan (FFR) trade negotiations. Consider this as an opportunity to accumulate funds for the assumed upcoming Christmas rally by averaging through investing over different time periods and taking profits regularly from a portion of your portfolio.

In the 9/25 issue, we will be covering Star Mica (3230), Kusuri No Aoki (3549), Needs Well (3992), Japan Material (6055), Sony (6758) and NF Corp (6864).

Selected Stocks

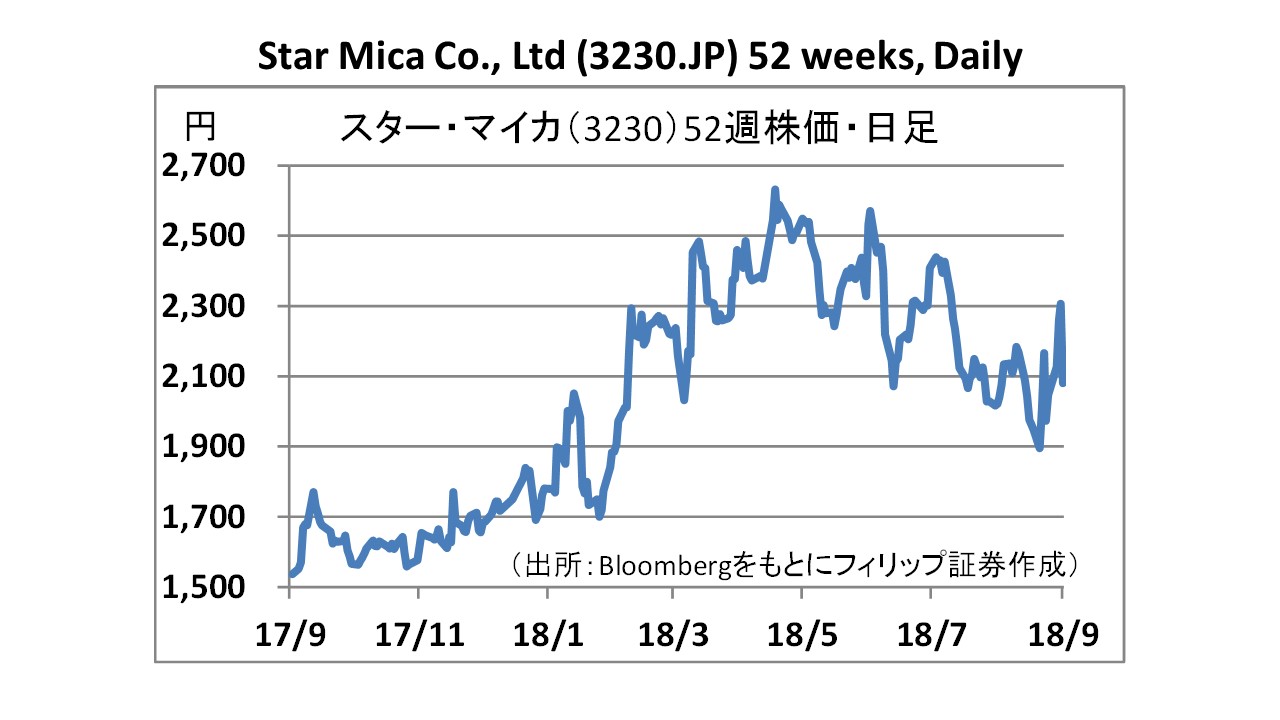

Star Mica Co., Ltd. (3230)

・Established in 2001. Plans and sells pre-owned condominiums after turning them into renovated condominiums. Actively acquires “owner-change properties” (properties under lease contracts) so as to improve the marketability of condominiums under lease contracts that have limited buyers in the market. In addition, also renovates condominiums vacated by tenants and sells these as “new homes” to home buyers.

・For 1H (2017/12-2018/5) of FY2018/11, net sales increased by 42.7% to 17.554 billion yen compared to the same period the previous year, operating income increased by 31.2% to 2.981 billion yen, and net income increased by 34.3% to 1.817 billion yen. In addition to the increase in rental revenue as the number of properties held increased, higher value-add of properties sold has also contributed. The sale of some properties held had also pushed up profits.

・Because of expected increase in rental revenue with increase in purchase of pre-owned condominiums, company has revised its 2018/11 plan upwards. Net sales is expected to increase by 30.0% to 30.007 billion yen compared to the previous year (original plan 26.059 billion yen), operating income to increase by 9.9% to 3.928 billion yen (original plan 3.669 billion yen), and net income to increase by 8.8% to 2.25 billion yen (original plan2.144 billion yen).

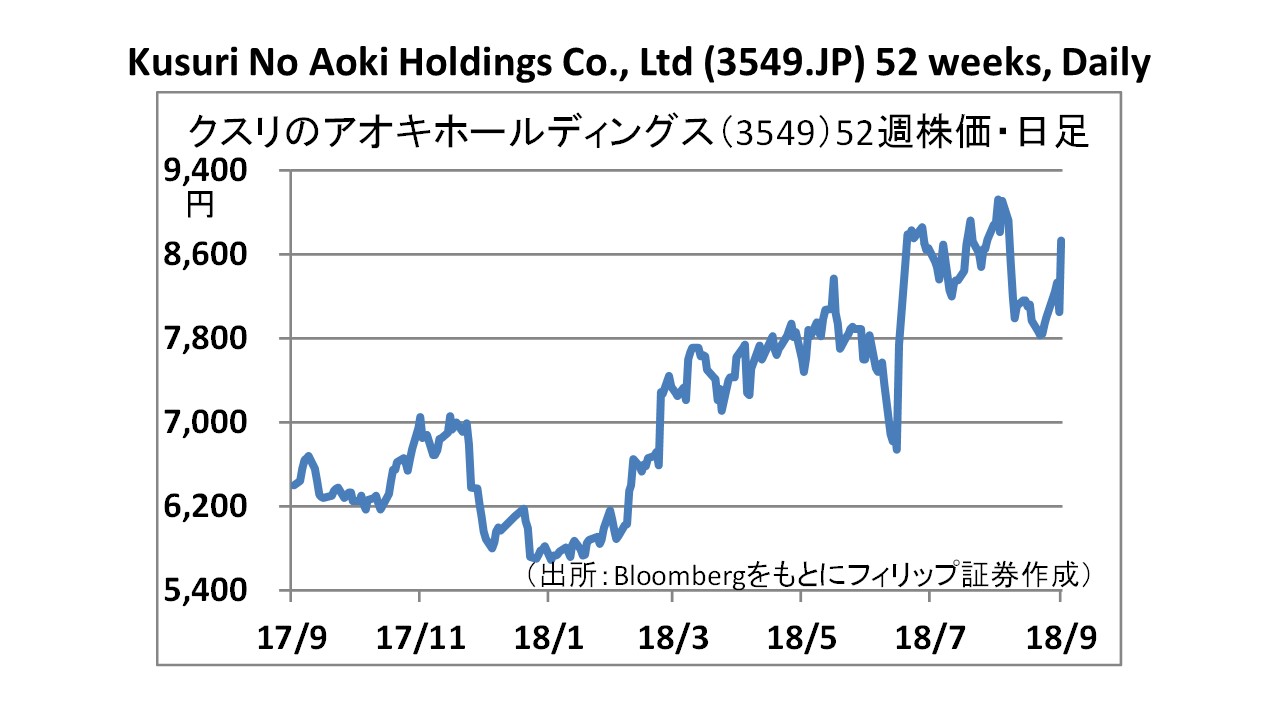

Kusuri No Aoki Holdings Co., Ltd. (3549)

・Founded in 1869. Operating drugstore chain, “Kusuri-no-Aoki” and dispensing pharmacies. While focusing on medicines and cosmetics as core products for the drugstores, company is also providing daily necessities such as everyday sundries, goods and small items of clothing in its emphasis to provide more convenience for consumers. Besides three prefectures in the Hokuriku region, company also has stores in Shin-Etsu, Kita-Kanto, Tokai and Kinki regions.

・For 1Q (June-Aug) of FY2019/5, net sales increased by 13.4% to 61.712 billion yen compared to the same period the previous year, operating income increased by 7.6% to 3.523 billion yen, and net income increased by 6.6% to 2.499 billion yen. Besides opening 16 new drugstores and 8 drugstore-cum-pharmacy stores, company has also completely renovated 5 existing stores. Sales of anti-perspirants and drinks had increased at existing stores.

・For FY2019/5 plan, net sales is expected to increase by 16.1% to 257.0 billion yen compared to the previous year, operating income to increase by 10.6% to 13.124 billion yen, and net income to increase by 5.4% to 9.3 billion yen. Company is planning to open 80 drugstores and 40 drugstore-cum-pharmacies. Company is also planning to revitalize existing stores by reviewing assortment of products and carrying out complete renovations.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: