Report type: Weekly Strategy

A Turn of Events Where Stock Prices Rise Furiously Despite Increasing Risks

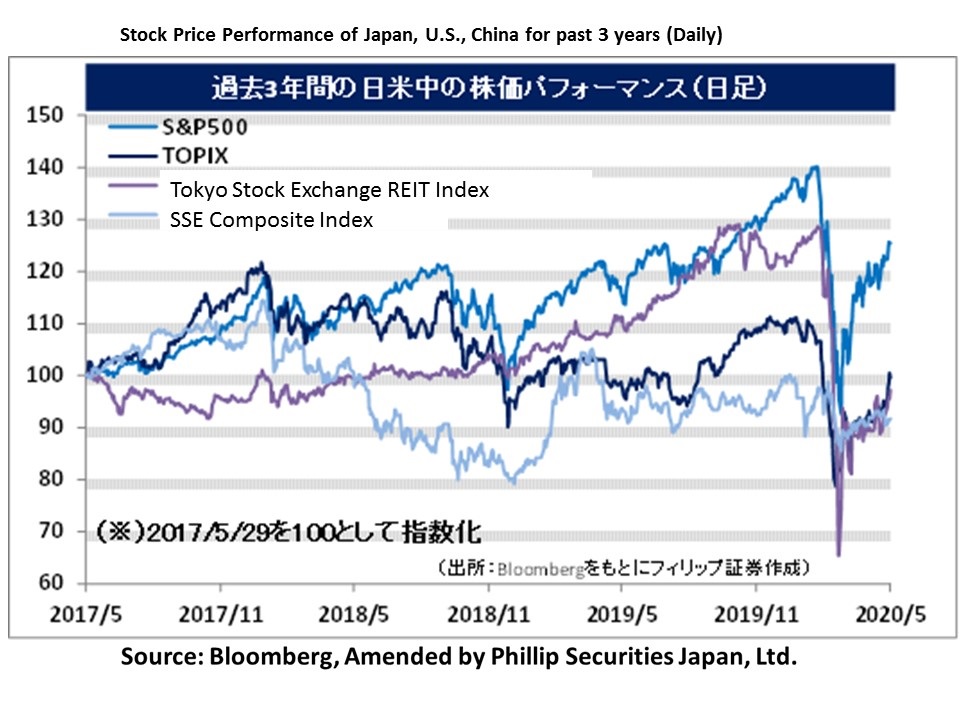

The state of emergency was lifted for all prefectures on 26/5, and on 27/5 the government made a cabinet decision on the secondary supplementary budget with an additional expenditure for this fiscal year’s general accounts amounting to a total of about 32 trillion yen. In response to this, the Nikkei average saw a growing increasing trend from the beginning of the week on 25/5 and closed at the end of the week at 21,877 points, up 1,489 points from the end of last week. As mentioned in the 18th May issue of this weekly report on “A Reevaluation of Japanese Stocks and A New Way of Life”, by sharing the sense of crisis felt by its citizens with regard to the unprecedented crisis of the Japanese economy and the lifestyles of its citizens, the increasing mood of “doing everything possible”, “implementing in large-scale” and “paying out quickly” seems to be reflected in the stock market as well. Also, regarding trends to look out for, as mentioned in the 25th May issue on “Breaking Away From “PBR Shakeup” and Low PBR Stocks”, there have been prominent stock price level adjustments of delayed low PBR stocks in addition to steel stocks.

On 25/5, the government clarified the policy to issue coupons from late July onwards, which can be used for domestic travel and restaurants, and announced ongoing preparations to roll out the “Go To Campaign” nationwide from August, a support measure for the tourism and F&B industry which would include movement extending across prefectures. In response to these movements, stock prices of tourism-related industries greatly affected by the spread of COVID-19, such as Japan Airlines (9201), have performed strongly. In addition to the rise in expectations towards a resumption of economic activities, there has also been increasing activity in rising stock price movements involving COVID-19 treatment / vaccine development. Due to the unfolding of a global neck-to-neck race to develop the vaccine, among biotech ventures, some corporations have seen a short-term increase in their stock prices until the market capitalisation of biotechnology corporations listed on the U.S. NASDAQ balances out.

With good stock market material in an uproar, on 28/5, the up-down ratio (indicator observing the sense of overheating of the market based on the ratio of the number of stocks having a price increase to the number of stocks having a price decrease) of the TSE Section 1 reached 136%, and there are concerns of short-term overheating. In addition, on 28/5, China via the National People’s Congress adopted the policy to enact the “Hong Kong national security law”, which prohibits anti-establishment activities. In response, U.S. President Trump intends to hold a press conference on 29/5, which hints at the possibility of imposing sanctions on China. In response to the U.S. Senate passing the bill that took Chinese corporations into consideration in delisting foreign corporations who refused auditing, there have been simmering observations in the market that China would come up with methods to expose risk to U.S. investors through shares of Chinese corporations listed in the U.S. or debts in U.S. dollar issued by Chinese corporations overseas. However, even if the intensification of the U.S.-China conflict is a source of material to cause a short-term drop in stock prices, perhaps this would encourage the money, etc. of Hong Kong’s wealthy to be directed towards Japanese stocks or Japanese real estate in the mid- and long-term.

In the 1/6 issue, we will be covering Matsuoka Corporation (3611), Maxell Holdings (6810), Nishi-Nippon Railroad (9031), and INES (9742).

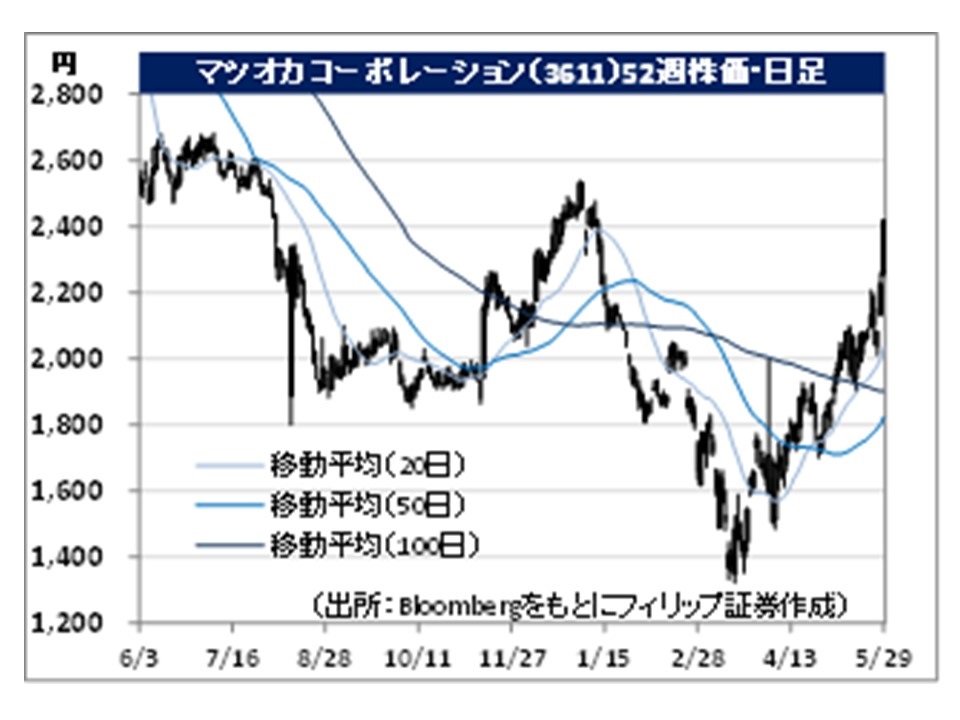

・Founded in 1956 as Matsuoka Gofukuten (kimono shop). In addition to planning, manufacturing and distribution, the company operates an “Apparel OEM Business” which manufactures clothing under consignor brands by receiving orders from apparel manufacturers, trading companies and mass retailers.

・For FY2020/3 results announced on 22/5, net sales decreased by 9.9% to 57.112 billion yen compared to the previous year and operating income decreased by 22.6% to 2.603 billion yen. Despite an increase in orders received mainly in casual wear for major SPA in the latter half, changes to the distribution policies of clients and production adjustments in the apparel industry following climate factors in the first half have affected, which lead to a decrease in sales and income.

・Their FY2021/3 plan is undecided due to uncertain effects from the spread of COVID-19. Company was chosen as one of the 5 suppliers for the cloth masks currently being distributed by the government, and the absence of problems faced in their collection has raised their rating. In addition, UNIQLO, which is under Fast Retailing (9983), will enter the mask business this summer, and the production and retail of cloth masks made from breathable material which prevent stuffiness when worn is also likely to benefit the company’s performance.

・Established in 1966. After becoming a wholly-owned subsidiary of Hitachi, Ltd. (6501) in 2010, they were relisted in 2014 and went independent from Hitachi Group. Mainly carries out the manufacture and retail of energy, industrial parts and materials as well as electrical and consumer products.

・For FY2020/3 results announced on 14/5, net sales decreased by 3.7% to 145.041 billion yen compared to the previous year and operating income fell into the red from 5.424 billion yen in the previous year to (137) million yen. In addition to a decrease in revenue in projectors and semiconductor-related embedded systems, a decline in the occupancy rate of their factory in China and a decrease in sales of optical components for the automobile market and in health / electrical personal appliances have affected.

・For its FY2021/3 plan, net sales is expected to decrease by 3.5% to 140 billion yen compared to the previous year and operating income to return to profit from (137) million yen the previous year to 500 million yen. With increasing awareness in hygiene due to the spread of COVID-19, there has been growth in sales of batteries for thermometers used for measuring temperature as well as the sterilising and deodorising machine for corporate and the general consumer. In addition to the sterilising and deodorising machine being used in the offices of Japanese corporations, orders for them appear to be increasing in Asian regions, such as in China.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: