Report type: Weekly Strategy

“A Sharp Rise in the Nikkei Average and the Age of Level 3 Autonomous Driving”

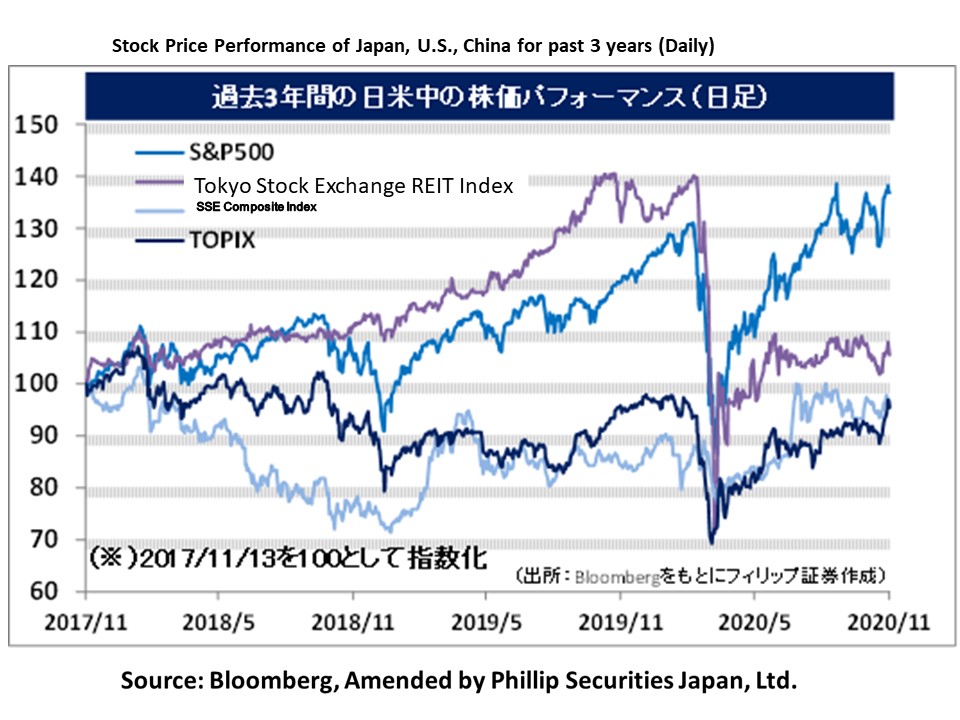

The Nikkei average, which rose to the 24,300 point level on 6/11, exceeded the high price of 24,448 points in Oct 2018 at the beginning of the week on 9/11 to become a high price that was last seen in 1992, then rose even more at one go to the high price of 25,587 points on 12/11. A sharp rise of 2,639 points played out in 8 business days since the low of 22,948 points on 31/10. With there being a couple of reasons for the rise, such as growing expectations towards the early supply of the COVID-19 vaccine as well as concerns beforehand on the prolongment of the conclusion of the U.S. presidential election being dispelled, we would like to examine the things suggested by these market movements to the future investment strategies of investors.

Firstly, based on technical analysis in terms of the chart, the bull market which started from the Nikkei average’s low (6,994 points in Oct 2018) since the bankruptcy of the Lehman Brothers in 2008, is suggested to have a greater possibility to continue in the long-term, and even if it eventually becomes a decreasing trend, we can perhaps say that the risk of it staying at a level of under 20,000 points for a long time has decreased. Next, based on a fundamentals analysis which focuses on the net asset value of corporations comprising the Nikkei average, the weighted average P/B ratio (price-to-book ratio) of the Nikkei average, which is a weighted average of market capitalisation, etc., was 1.17 times at the closing price on 12/11, and a net asset value equivalent to a weighted average P/B ratio of 1.0 would work out to be an approximate of 21,812 points. With the exception of Mar-May this year where the market was ravaged due to it being caught up in the COVID-19 pandemic, attention is likely on the fact that the Nikkei average tends to stop falling near the weighted average P/B ratio of 1.0 times. Also, based on the past 3 years, since the snap election of the House of Representatives was held in 2017, there was a time in Jan 2018 where the weighted average P/B ratio rose to around 1.4 times. If we apply this to the net asset value on 12/11, it would be possible for it to exceed 30,000 points, however, in the mid and long-term, perhaps we can expect a permissible range of the weighted average P/B ratio up to about 1.3 times.

On 11/11, Honda Motor (7267) announced that they were the world’s first to obtain the designation of the type demanded by level 3 autonomous driving from the Japanese Ministry of Land, Infrastructure, Transport and Tourism. “LEGEND”, the first luxury sedan to be equipped with it, is planned to go on sale by March 2021. In level 3, although there is a need for the driver to immediately take over in case it falls into a situation outside of its design, normally, there is no need for the driver to pay attention to their surroundings during automatic driving, and also enables them to carry out other tasks. This seems to be a perfect chance to allow us to experience an evolution in the times. From the perspective of investment strategy, perhaps we can say that there is a big opportunity for corporations involved with technology development, such as the “in-vehicle image sensor”, which captures images by converting light to electric signals, the “millimetre wave radar”, which measures distance using low frequency radio waves, and “LiDAR”, which measures distance based on laser reflection, etc.

In the 16/11 issue, we will be covering Nisshinbo Holdings (3105), Komeda Holdings (3543), Maxell Holdings (6810), and Chino (6850).

Nisshinbo Holdings Inc. (3105) 720 yen (13/11 closing price)

・Established in 1907. Is a conglomerate comprised of wireless and communications, micro devices, brakes, precision devices, chemicals, fibres, real estate and other business segments. They are aiming to be an “environment and energy company”.

・For 9M (Jan-Sep) results of FY2020/12 announced on 12/11, net sales decreased by 10.5% to 335.977 billion yen compared to the same period the previous year and operating income saw an expansion in deficit from (589) million yen the same period the previous year to (696) million yen. It was affected by the slump in demand due to the COVID-19 catastrophe. On the other hand, net income increased by 45.2% to 5.924 billion yen due to investment securities, gain on sale of fixed assets and revenue from subsidies.

・For its full year plan, net sales is expected to decrease by 9.4% to 462 billion yen compared to the previous year and operating income to fall into the red from 6.4 billion yen the previous year to (4) billion yen. In addition to their subsidiary, JRC Mobility, buying out 2 German in-vehicle equipment development companies in end April this year, they presented the technology of simultaneously detecting 3D positional information and speed information by combining the data from camera images and millimetre wave radar at the home appliance and IT fair, “CEATEC”. It appears that preparations for the age of autonomous car driving are progressing smoothly.

・Originated from the opening of a coffee shop in Nagoya in 1968. Expands the FC business nationwide by owning the brands “Komeda’s Coffee” in addition to “Okagean”, “Yawaraka Shirocoppe”, “Komeda’s Stand” and “Bakery Ademok”.

・For 1H (Mar-Aug) results of FY2021/2 announced on 14/10, sales revenue decreased by 12.1% to 13.479 billion yen compared to the same period the previous year and operating income decreased by 38.9% to 2.404 billion yen. Despite growth in takeaway sales including deliveries in their stores, the COVID-19 catastrophe influenced the decrease in revenue. Impairment loss involving some directly managed stores and sales support to FC member stores influenced03 the decrease in profit.

・For its full year plan, sales revenue is expected to decrease by 11.6% to 27.6 billion yen compared to the previous year and operating income to decrease by 32.3% to 5.33 billion yen. For wholesale sales for existing FC member stores compared to the same period the previous year, although it decreased by 19.0% in the first half (1H), an improvement in business performance was indicated with the 1.0% increase in the single month of September and the 1.6% increase in the single month of October. For a total of 896 stores at the end of August this year, the company is aiming to build a system of 1,000 stores. They are predicting an accelerated speed of advancement by aiming for 50 stores in Taiwan by 2022.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: