|

Report type: Weekly Strategy

|

”A Political Situation Starting to Stir and Economic Measures That Are Required”

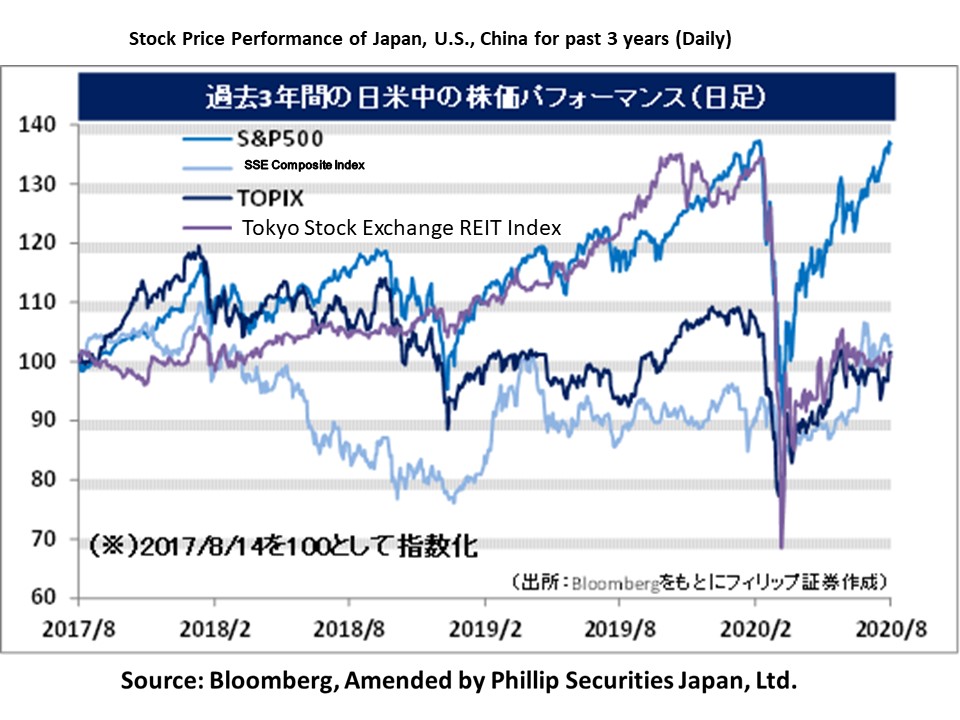

As mentioned in the 3rd August issue of our weekly report, “Is It the Time to Estimate the Point Where the Correction Phase Ends?”, 7/8 seems to have been a day which was an important turning point. The increase in U.S. nonfarm payrolls in the U.S. employment statistics for July announced on 7/8 exceeded market expectations, suggesting that movements of a recovery in the U.S. economy was not stagnating, and the U.S. long-term interest rate also shifted to an upward trend. For the Nikkei average, after falling to 22,204 points on 7/8, it shifted towards an increase, marking 23,338 points on 14/8. Although trends involving U.S. economic indicators and the U.S. long-term interest rate are considered important for Japanese stocks for the time being, Japan’s Apr-Jun GDP will be announced on 17/8. Although market focus appears to have already shifted towards the Jul-Sep GDP, even if the figures turn out to be bad, there is likely room to take it positively as an opportunity for the government to feel a sense of crisis and work on economic measures.

With there being about another 2.5 months until the U.S. presidential election in early November, following U.S. President Trump’s executive order to ban U.S. residents from carrying out transactions involving the Chinese video publishing app “TikTok” and the communications app “WeChat”, he has been coming up with strong policies in the economy and foreign policy towards the reelection, such as signing the executive order to implement additional COVID-19 economic policies, etc. However, the growing importance of the political situation towards an election is the same for Japan. On 13/8, the Democratic Party for the People agreed to split effectively and merge with the Constitutional Democratic Party of Japan. Being aware of the possibility of a dissolution of the House of Representatives and a general election within the year, this appears to have been related to movements of a new party formation. Especially when considering the schedule of the expiry of the Liberal Democratic Party’s presidency term in September and the Jul-Aug Olympics and Paralympics, this is thought to be highly possible. Even if it were to dissolve within the year, there is the expectation of a high likelihood of the government being aware of the election and implementing even stronger

economic policies, which we can likely expect an influx of funds into the Japanese stock market.

However, if it comes to the situation where the spread of COVID-19 increases again and there is an official announcement to declare a state of emergency again, from the viewpoint of avoiding the “3 proximities”, there is a high chance that the election will be postponed. In particular, there is global concern regarding chaos from being infected with both influenza and COVID-19 from autumn onwards, hence, it is crucial that they as a government first prioritise measures to prevent influenza. Even if the election does not take place and the impact from the spread of COVID-19 persists, there will likely be a demand to raise the pace of increasing government spending, such as the COVID-19 sustained payouts, etc. In that sense, we can consider that a positive situation for the stock market is highly likely to result regardless whether the snap election will take place this year or not. For the time being, matters of concern which may influence the stock market are likely to be on the rebound from short-term over-buying of the stock prices of key U.S. IT corporations.

In the 17/8 issue, we will be covering Meiji Holdings (2269), Japan Electronic Materials (6855), Canon Marketing Japan (8060), and Chilled & Frozen Logistics Holdings (9099).

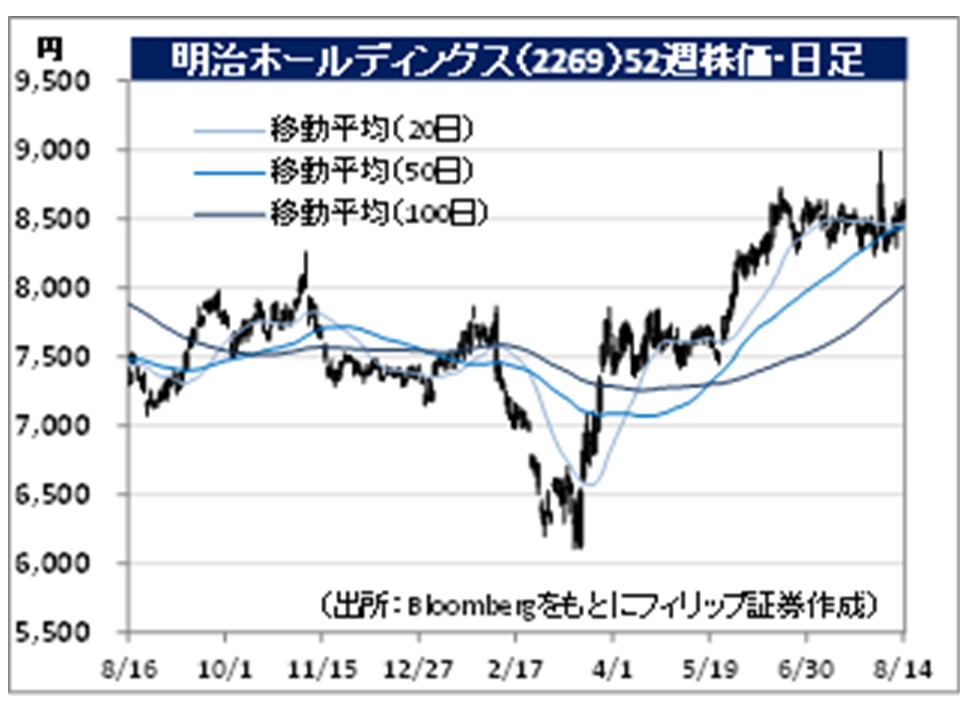

・Established in 2009 from a merger between Meika Seika and Meiji Dairies. Manages two business segments, which are foodstuff and pharmaceuticals. KM Biologics, who inherited the pharmaceutical business, the Chemo-Sero-Therapeutic Research Institute (Chemo-Sero-Research), became their consolidated subsidiary in 2018.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 12/8, net sales decreased by 5.9% to 281.167 billion yen compared to the same period the previous year and operating income increased by 12.2% to 23.161 billion yen. Despite an overall revenue decrease from a decrease in revenue in their confectionery business and 3 companies being excluded from consolidation due to the share transfer, a revenue increase such as in yoghurt, etc. and cost management, such as sales promotion expenses, etc. have contributed to a profit increase.

・For its full year plan, net sales is expected to remain unchanged at 1.253 trillion yen compared to the previous year and operating income to increase by 7.1% to 111 billion yen. With the predicted increase in demand for influenza prevention vaccinations across the world from the possibility of severe symptoms appearing when infected with both influenza and COVID-19, we can expect net sales to turn out better than the forecast (15.7% increase to 30.2 billion yen compared to the previous year) for the influenza vaccine handled by KM Biologics.

・Established in 1960. Carries out the development, manufacture and retail of semiconductor inspection components and electron tube components. Their mainstay probe card (circuit board with probes) for semiconductor inspection is used in the wafer test, which is an early process in semiconductor production.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 6/8, net sales increased by 31.2% to 4.188 billion yen compared to the same period the previous year and operating income increased by 6.6 times to 804 million yen. As a response to the recovery of the semiconductor market which was supported by data centre-related investments, progress in sales promotion of products for memory IC, whose demand increased for PCs and servers, have led to an increase in their mainstay probe card.

・For its full year plan, net sales is expected to increase by 8.5% to 17 billion yen compared to the previous year and operating income to increase by 2.3 times to 2.3 billion yen. With attention on the miniaturisation of the circuit line width to 7 nanometres (nm) (a nano is 1/1 billion) in cutting-edge semiconductor technology, we can also expect a rise in the standard of technology requested for probe cards, which are essential in the process of the “wafer test” (quality goods test for manufactured IC chips) in semiconductor device production, hence, demand for the company’s technology is also likely to increase.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: