Report type: Weekly Strategy

A P/B Ratio Revolution, Footsteps of an Approaching Inflation Era and Delayed Inbound Tourism Stocks

The appointment of the successors to the Bank of Japan’s governor and deputy governors were presented to the Diet on the 14th. It appears that the market has taken the stance of observing with bated breath on the remarks that will be made at the House of Representatives’ opinion hearing on the 24th by Ueda, an economist presented by the government as the next governor. The stock market is also growing increasingly at a standstill. Regarding the “Nikkei Average Volatility Index (Nikkei Average VI)”, which is also known as the Japanese version’s fear indicator reflecting investor sentiment on Japanese stocks, its closing price on the 16th fell to 14.71, the lowest level since Jan 2021. This indicates that the incorporation of short-term positive factors leads to a dissipating sense of caution regarding a stock market decline. In this situation, it can be said that there is a polarization in supply and demand where the range of increase regarding positive factors tend to become smaller while there tends to be extreme reaction to negative factors.

To that extent, there is increasing vividness of a diagram where relatively risk-adverse capital gathers in value stocks. Its driving force is the TSE (Tokyo Stock Exchange). In the “TSE’s measures for the future based on a summary of issues” announced on 30/1, it is said to be proceeding with measures by separating ① a clarification on the end of transitional measures (approving provisional listing of enterprises that have not met criteria to maintain listing) and ② motivation for initiatives towards improving mid-term corporate value. Out of which, ②’s purpose is “to promote initiatives for improvement by encouraging literacy improvement and a reform in awareness towards stock price / market capitalization as well as the capital cost of listed companies”. It also said that they are “strongly calling on disclosure for companies having a continuous P/B ratio of less than 10%” and that its period of implementation would be Spring ’23. For Dai Nippon Printing (7912), which declared on the 9th that they would be strengthening shareholder return towards improving capital efficiency, there is a possibility that their stock price surge on the 10th would be viewed retrospectively as an epoch-making event in the Japanese stock market this year.

According to the Monthly Labor Survey (flash report) for December last year announced on the 7th, although there were temporary factors for the high rate of increase in bonuses, nominal wages saw high growth since 25 years and 11 months ago at a 4.8% increase compared to the same period the previous year. Real wages excluding the impact of price fluctuation also secured a positive at a 0.1% increase compared to the same period the previous year. It signaled the possibility of the beginning of an inflation era where there is an increase in both wages and prices. In an inflation era, there is an increase in the importance of the value of real assets as opposed to cash. If the current market price is significantly cheaper than the book value per share value of an enterprise owning many real assets, it would likely tend to have significant room for a corresponding review.

The estimated number of foreign visitors to Japan in January announced on the 15th by the Japan National Tourism Organization was 1,497,300, which recovered to the level of a little over 50% compared to January 2019 before the COVID-19 pandemic. It seems that the recovery in demand related to foreign visitors to Japan (inbound) will continue. China also partially lifted its ban on group tours abroad from the 6th. Amongst railway stocks related to inbound tourism, occasionally there are those with their recent stock price under the low of Spring ’20 mainly due to margin trading supply and demand that is unrelated to business performance. Although it may require some time until a stable level is reached in improving the margin balance ratio, it could be a good investment opportunity.

In the 20/2 issue, we will be covering Oji Holdings (3861), Nippon Sheet Glass (5202), Toppan (7911), and Kyoritsu Maintenance (9616).

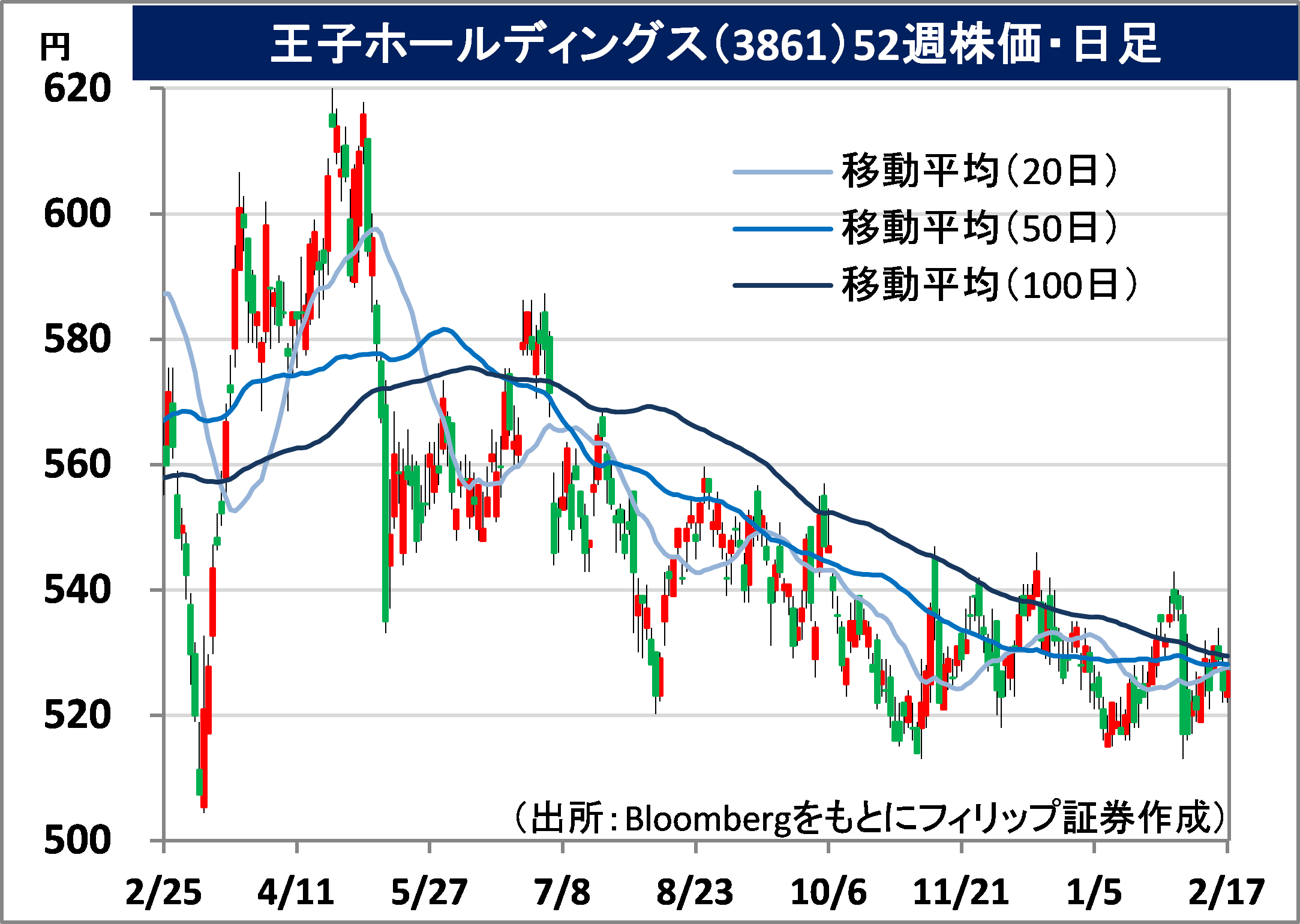

Oji Holdings Corporation (3861) 527 yen (17/2 closing price)

・Started as Tomakomai Paper in 1949 after its founding in 1873. Its main businesses are the lifestyle industrial materials (corrugated paper and packaging paper, etc.), functional materials (special paper, etc.), resource and environment business (pulp, etc.) and print information media (newspapers, etc.).

・For 9M (Apr-Dec) results of FY2023/3 announced on 3/2, net sales increased by 19.4% to 1.2967 trillion yen compared to the same period the previous year and operating income decreased by 37.5% to 59.5 billion yen. A recovery in paper demand, an increase in the pulp market condition and retail price hikes contributed to an increase in revenue. There was a decrease in operating income due to the impact of skyrocketing raw material and fuel prices. For 3Q (Oct-Dec), net sales increased by 22% and operating income decreased by 40%.

・For its full year plan, net sales is expected to increase by 22.4% to 1.8 trillion yen compared to the previous year, operating income to decrease by 12.6% to 105 billion yen and annual dividend to have a 2 yen dividend increase to 16 yen. The company is the top private enterprise to have a forest ownership area in Japan of 188,000 ha (hectares). 2nd is Nippon Paper Industries (3863) at 90,000 ha and 3rd is Sumitomo Forestry (1911) at 44,000 ha. The company’s P/B ratio (price-to-book ratio) at the closing price on the 16th was 0.54 times. We can likely expect a review in the value of assets able to contribute to decarbonization.

Nippon Sheet Glass Co., Ltd. (5202) 678 yen (17/2 closing price)

・A manufacturer specialising in glass under the Sumitomo Group that established in Osaka City in 1918. Converted the British Pilkington to a wholly-owned subsidiary in 2006 and expands globally. Mainly operates the construction glass business, automobile glass business and high-performance glass business.

・For 9M (Apr-Dec) results of FY2023/3 announced on 9/2, net sales increased by 27.8% to 566.2 billion yen compared to the same period the previous year and operating income increased by 66.3% to 24.1 billion yen. For the construction glass business which includes glass for solar cell panels, net sales increased by 33% to 275.6 billion yen and operating income increased by 28% to 26.1 billion yen, which grew. For overall 3Q (Oct-Dec), operating income increased by 5.3 times.

・Company revised its full year plan upwards. Net sales is expected to increase by 24.9% to 750 billion yen (original plan 740 billion yen), operating income to increase by 40.1% to 28 billion yen (original plan 18 billion yen) and net income to fall into a deficit from 41 billion yen the previous year to (37) billion yen (original plan (41) billion yen). In addition to the aspect of resolving longstanding issues in recording impairment loss of assets involving the automobile glass business in Europe, benefits can be anticipated from movements by the U.S. government in domestic production of solar panels.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: