|

Report type: Weekly Strategy |

■ 4 Risk Factors That Will Pull the Rug Out From Under the Japanese Stock Market

The environment concerning Japanese stocks of late has been gradually worsening. Developments that push up the Japanese stock market have been gradually fading, such as expectations on the Kishida administration after the House of Councillors’ election and expectations on inbound travel consumption from the resumption of accepting foreign tourists visiting Japan. The following 4 points can be considered to be main factors for this.

The first factor is doubts on the Bank of Japan’s monetary policies. With major countries of Europe and the U.S. reinforcing monetary tightening towards curbing inflation, the maintenance of monetary easing policies by the Bank of Japan is encouraging a depreciation of the yen. There are also benefits of the depreciation of the yen, such as pushing up corporate profits via export and it easily becoming an advantage for blue chip stocks which have high contribution to the Nikkei average. However, the term of office of the governor and vice governor of the Bank of Japan is until April next year, and depending on the intentions of the Kishida administration after the election, perhaps doubts will likely grow stronger in the market regarding the Bank of Japan also being forced to change its policies from “dovish” to “hawkish” similar to the Swiss National Bank as of late.

The second factor is the sudden worsening of the recent Japanese economic climate. The Indices of Industrial Production for May worsened significantly with a 7.2% decline compared to the previous month. The Japanese Ministry of Economy, Trade and Industry’s overall economic assessment for production went from “being at a standstill” to “bearish”. It appears that the negative impact from strict restrictions in going out in May in China have surfaced. Since the Purchasing Managers’ Index (PMI) for June announced by the National Bureau of Statistics in China increased from 49.6 in May to 50.2, Japan’s Indices of Industrial Production for June is expected to have a high possibility of rebounding as well, however, there is a lack of power in the range of increase in the said PMI and it is considered to be inadequate in order to push up the Japanese stock market.

The third factor is that the number of new COVID-19 infections is shifting towards an increase again. For Tokyo, at the infection status monitoring meeting on 30/6, it was said that the cautionary level, which is determined based on 4 levels, was raised by 1 level to the 2nd highest. There is a similar trend of an increase in new infections in the U.S. as well and the Omicron variants “BA.4” and “BA.5” have become the main. The U.S. FDA (Food and Drug Administration) has advised manufacturers to manufacture a vaccine to combat the variants and is leaning towards a viewpoint of making it mandatory to receive the 4th vaccination from this autumn onwards. In Japan, although Prime Minister Kishida has decided to establish a “Cabinet Infectious Diseases Crisis Management Agency”, a damper has been placed on travel and leisure, department stores and F&B outlets which have shown signs of recovery as of late, and concerns have emerged on the possibility of inbound travel consumption falling through as well.

The fourth factor is concerns of an intensification in the strained energy supply and demand. With the official announcement of a “warning of tight electricity supply and demand” due to record-level heat waves, regarding the Far East petroleum and natural gas development project “Sakhalin 2” which Mitsui & Co. (8031) has invested 12.5% and Mitsubishi (8058) has invested 10%, on 1/7, Russia’s President Putin signed a decree dictating a change to a Russian enterprise which will newly establish a business entity. It is concerning that risks have emerged on Japan’s entire natural gas supply losing approx. 10% as a result of this.

In the 4/7 issue, we will be covering Komehyo Holdings (2780), Tokyu Fudosan Holdings (3289), Weathernews (4825), Giken (6289) and 7-Eleven Malaysia Holdings (SEM).

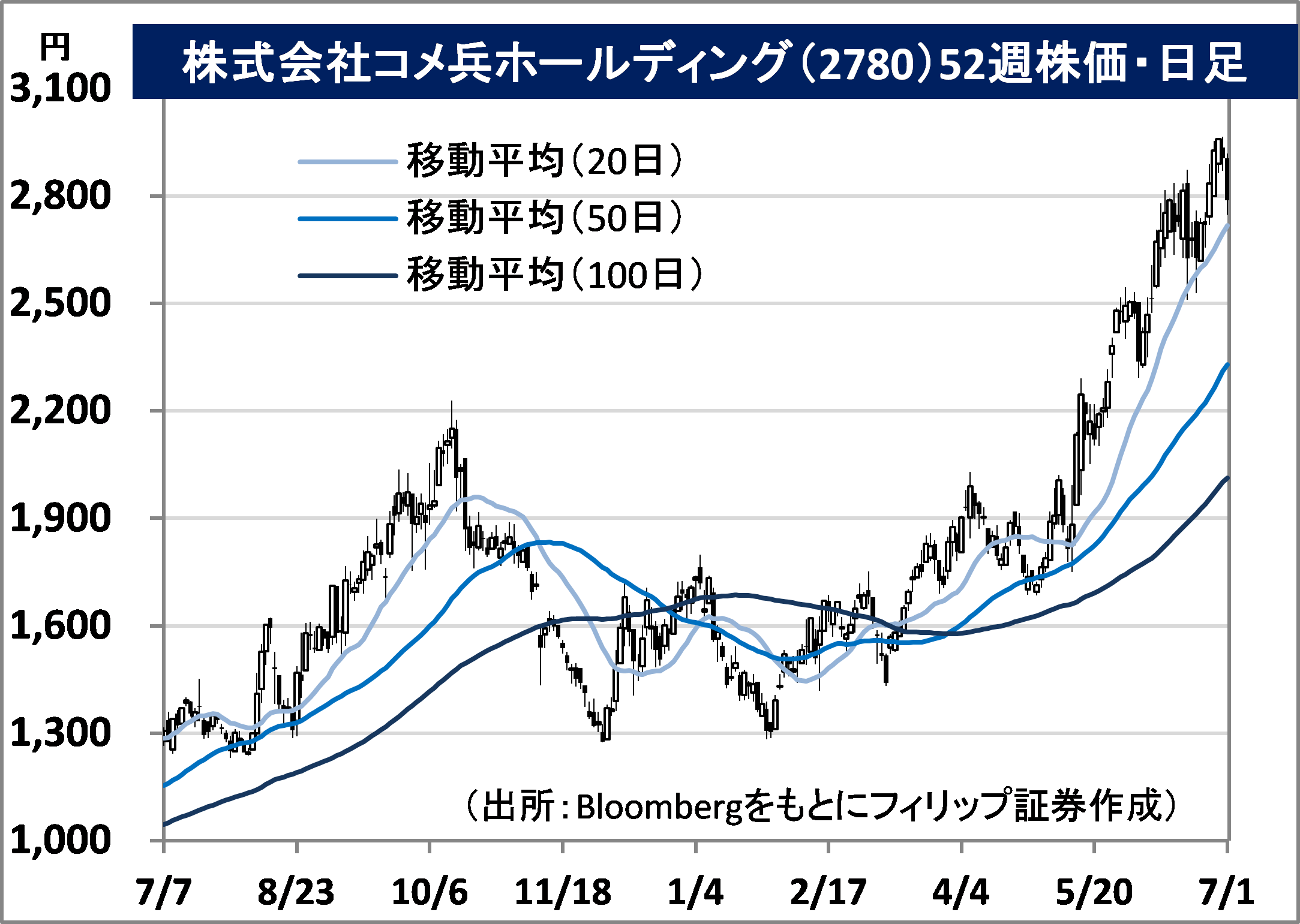

Komehyo Holdings Co., Ltd. (2780) 2,788 yen (1/7 closing price)

Founded a secondhand clothing store in 1947 in Osu, Nagoya City. Expanded to deal with secondhand items, such as gemstones, precious metals, watches, cameras and musical instruments. Operates the designer fashion business in Japan and overseas as well as the tyre / wheel business.

For FY2022/3 results announced on 13/5, net sales was 71.148 billion yen (50.723 billion yen in the previous year before the application of the accounting standard for revenue recognition) and operating income increased by 6.3 times to 3.714 billion yen. There has been success in reinforcing online auctions for corporations as well as online stores and events to secure merchandise in order to reinforce individual purchases after ensuring safety involving COVID-19 infection.

For its FY2023/3 plan, net sales is expected to increase by 9.6% to 78 billion yen compared to the previous year, operating income to increase by 1.8% to 3.78 billion yen and annual dividend to have a 12 yen dividend increase to 44 yen. With the market price of gold shifting within a high price, due to an increase in the sales distribution ratio of gemstones and precious metals, there was a continuous increase in revenue with monthly net sales for May having increased by 40.5% year-on-year. On the 28th, the U.S. Biden administration announced a ban on Russian-made gold. Russia’s gold is a mainstay export item after petroleum and natural gas.

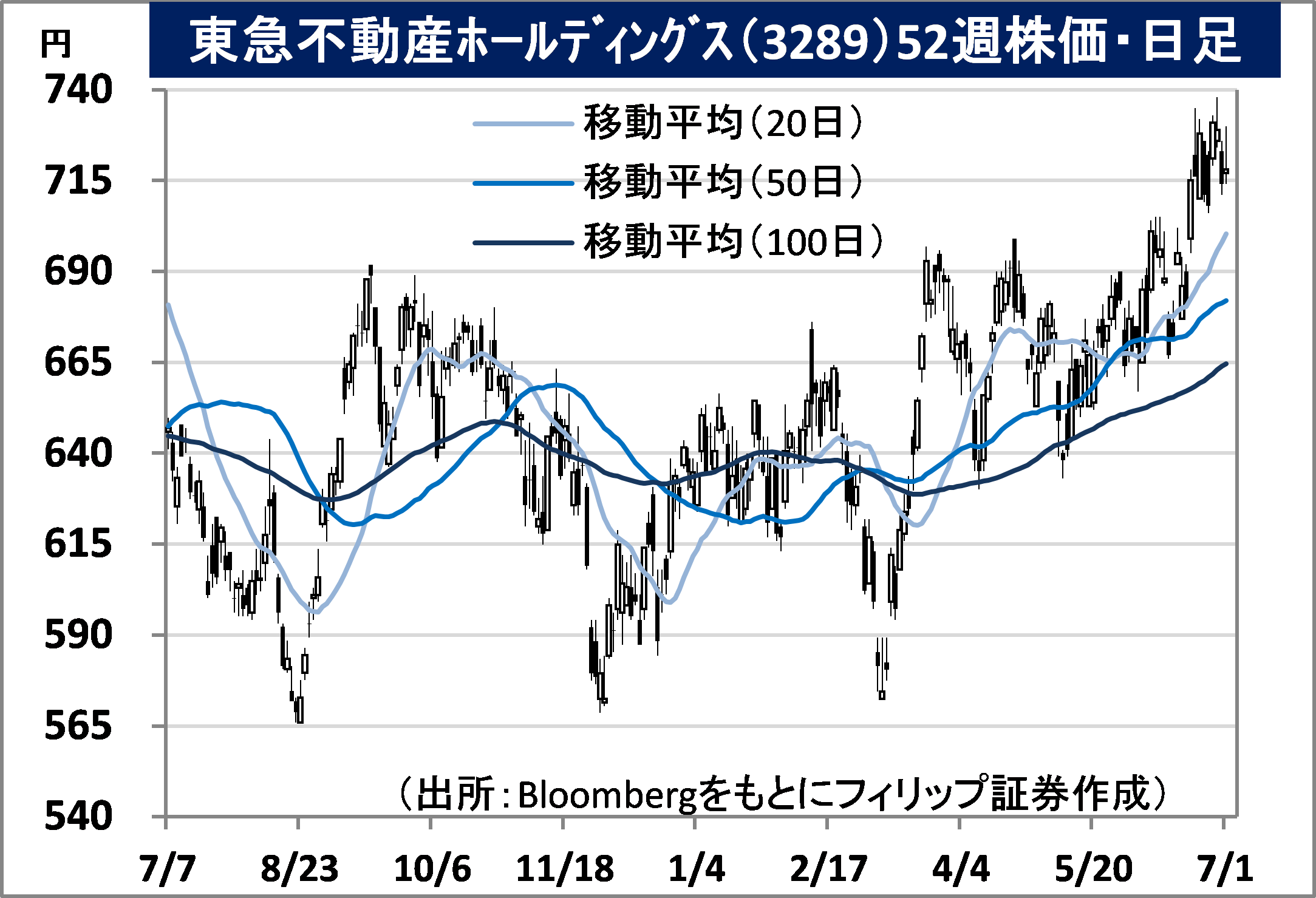

Tokyu Fudosan Holdings Corporation (3289) 718 yen (1/7 closing price)

A general real estate company under the Tokyu (9005) group. Tokyu Real Estate went independent from Tokyu in 1953. Due to the joint share transfer method in 2013, it was established as a wholly owning parent company of Tokyu Livable, Tokyu Community and Tokyu Land.

For FY2022/3 results announced on 11/5, net sales increased by 9.0% to 989.049 billion yen compared to the previous year and operating income increased by 48.3% to 83.817 billion yen. A declaration of a state of emergency was issued in response to the spread of COVID-19 in the previous year and there was an increase in income and profit from a reaction which had limited impact compared to significant limitations on businesses that arose from the reduction of operating hours and the suspension of businesses of commercial facilities, etc.

For its FY2023/3 plan, net sales is expected to increase by 1.1% to 1 trillion yen compared to the previous year, operating income to increase by 7.4% to 90 billion yen and annual dividend to have a dividend increase by 1 yen to 18 yen. Foreign tourists have begun to be accepted following the easing of entry restrictions to Japan from 10/6. There is expected recovery, such as in “hotels” and “leisure” in the operation management business. The company owns multiple hotels and ski resorts in Niseko, Hokkaido. They will likely gain attention if Sapporo is chosen as the city for hosting the 2030 Winter Olympics and Paralympics.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: