Report type: Weekly Strategy

”20 Times Forecast PER Hurdle”, Partnership With US Companies

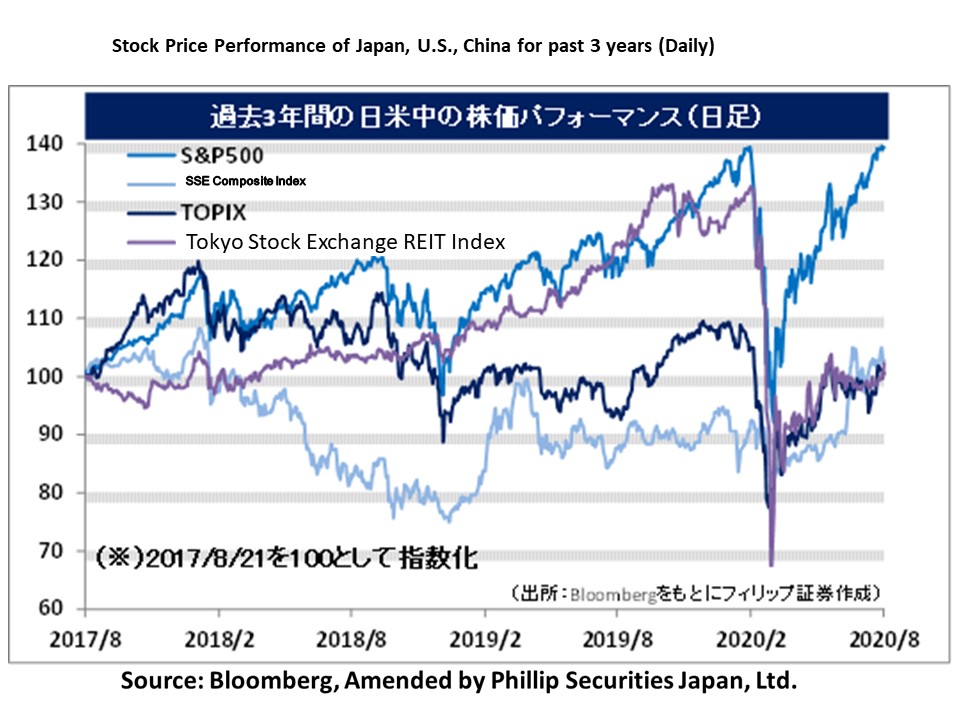

Both Japan and US companies have completed the April-June financial results announcements. Perhaps due to lack of reasons for active trading, transactions of the First Section of the TSE have been below 2 trillion yen since 17/8, and it seems that the Nikkei Average is losing momentum whenever it exceeds 23,000 points. The closing price of 22,880 points on 20/8 was 21.75 times the weighted average forecast PER (Price-to-Earnings Ratio), and 1.09 times the weighted average PBR (Price-to-Book Ratio) based on those announced in the Nihon Keizai Shimbun. The weighted average forecast PER has been below 20 times since the end of April 2013, when BOJ Governor Kuroda announced the “Kuroda Bazooka” quantitative and qualitative monetary easing measures. However, during the period from 13/5-5/6 this year, it exceeded 20 times for the first time in seven years. This is because while companies’ outlooks for full-year results are pointing towards decreasing profits due to the effects of Covid-19, the number of newly-infected Covid-19 patients appears to be decreasing, and with the government’s lifting of its declaration of emergency, expectations for economic activity resumption have increased. These probably resulted in the Nikkei Average trending higher at a faster rate, and the PER, which is the ratio of the stock price to earnings per share, has increased.

The weighted average forecast PER was less than 20 times after 8/6, but it exceeded 20 times again after 7/8, reflecting the effect of downward revision of full-year company forecast profits in the financial results announcements. Compared with NY Dow Industrial Average (forecast PER at 20/8 closing price was 27.1 times), it seems to be relatively cheaper. However, when compared to the period between 13/5-5/6, expectations for resumption of economic activities appeared to have declined as Covid-19 infections have not subsided nationwide, and restaurants and karaoke stores in Tokyo that serve alcohol had been asked to shorten business hours. Under such circumstances, it is unlikely for PER exceeding 20 times to be sustained. If there are no significant changes in company profit outlooks by the September financial results announcement period, it will be difficult for the Nikkei Average to sustain above 23,000 points, as can be seen by this week’s market movements.

However, as mentioned in the previous week’s report, the political situation is changing ahead of the extraordinary Diet session in Autumn, as the term of office of the House of Representatives and the LDP president will expire by next year. These may potentially lead to changes in Japanese politics and economy, and could therefore be factors pushing up the forecast PER of Japanese stocks.

In the short term, there is concern whether growing US companies will be able to maintain their current share price levels. However, it can be said that Japanese companies that have close relationships with these companies have opportunities to enhance their businesses. Examples include Life Corporation (8194), which was the first domestic food supermarket to operate on Amazon’s “Prime Now” in September last year, and TerraSky (3915), a sales force consulting partner. Panasonic (6752) has also announced investments to increase production of batteries for Tesla EVs, despite discontinuing the solar cell business with Tesla. These all look promising for the future.

In the 24/8 issue, we will be covering Iwatsuka Confectionery (2221), Sumitomo Dainippon Pharma (4506), Panasonic (6752), and Fukuda Denshi (6960).

・Established in 1947 in the current Nagaoka City, Niigata Prefecture. Operating rice cracker business manufacturing senbei, arare and okaki, etc. Ranked third in Japan for rice crackers. In terms of profit, notheworthy that company is receiving dividends from Want Want Group of Taiwan, into which company has invested and injected technology.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 11/8, net sales increased by 3.1% to 5.65 billion yen compared to the same period the previous year, operating income increased by 2.7 times to 34 million yen, and ordinary income increased by 5.4 times to 61 million yen. Despite the impact of business suspensions at sales subsidiaries, company still enjoyed higher sales and profits owing to hoarding purchases as a result of stay-at-home measures arising from Covid-19.

・For its full year plan, net sales is expected to increase by 1.6% to 23.2 billion yen compared to the previous year, operating income to increase by 2.1 times to 360 million yen, and ordinary income to decrease by 6.0% to 2.4 billion yen. Stock dividend income from Want Want Group in the previous period amounted to 2.248 billion yen. While company owns only 5% of Want Want Group, the latter has become the world’s leading producer of rice crackers which are sold in 56 countries. It is also handling a wide range of beverages and has grown into a global food manufacturer.

・Osaka Pharmaceutical, established in 1897, was its predecessor. Merged with Sumitomo Pharmaceuticals in 2005/10, with Sumitomo Chemical (4005) as the parent company holding 51.6%. North America constitutes more than 50% of the sales revenue. Focusing on anti-psychotics, anti-cancer and regenerative cells.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 30/7, revenue increased by 13.9% to 133.857 billion yen compared to the same period the previous year, and core operating profit excluding non-recurring items from operating profit increased by 9.4% to 24.367 billion yen. Core segment profit decreased 29.0% year-on-year in China, but increased 21.7% in the principal markets of North America and 10.6% in Japan, contributing to the performance.

・For its full year plan, revenue is adjusted downwards, increasing by 2.5% to 495.0 billion yen compared to the previous year (original plan: 510.0 billion yen), and, with SG&A expenses expected to decrease, core operating profit is expected to differ from the original plan, decreasing by 54.2% to 33.0 billion yen. Mitsubishi Chemical Holdings (4188) has already converted Mitsubishi Tanabe Pharma into a wholly-owned subsidiary. Added to this, uncertainty over Covid-19 is causing parent companies to want to keep profits within corporate groups. There is therefore possibility of company adopting TOB to convert companies to wholly-owned subsidiaries.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: