Investment Merits

Since the completion of its end-of-Phase 2 meeting with the US Food and Drugs Administration (FDA) in December 2019, iX Biopharma has been talking to potential out-licensing partners to undertake Phase 3 development trials for acute moderate to severe pain. Successful out-licensing agreements are expected to generate licensing fees for the company, including upfront licensing fees. This is expected to turn iX Biopharma profitable in FY21e.

Since its successful development of various specialty pharmaceutical and nutraceutical drugs, iX Biopharma has begun commercialising them. It has planned a six-fold increase in production capacity by 2H21 to cater to anticipated demand growth of 252% for its products. Further expansion is planned for FY22. This should support sales growth of 270% YoY in FY21-22e.

Potential for incorporating WaferiX in off-patent drugs opens opportunities to iX Biopharma for future drug development, given the advantages for the WaferiX technology to be incorporated with various pharmaceutical drugs. When WaferiX is incorporated in a drug with tested and proven clinical effects, the result is a new product with patented intellectual property. This is thanks to its unique formulation which has identical active drug components as traditional formulations.

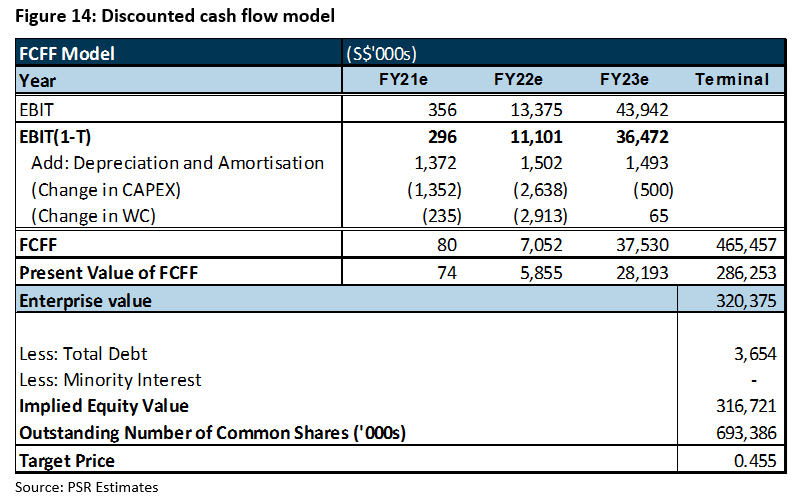

We initiate coverage with a BUY rating. Our target price of S$0.455 is derived from DCF valuation with a weighted average cost of capital (WACC) of 10.0% and terminal growth rate of 2%. It implies 12.0x FY22e PE, which we believe is not demanding given an industry average of 40x.

WaferiX – The Technology

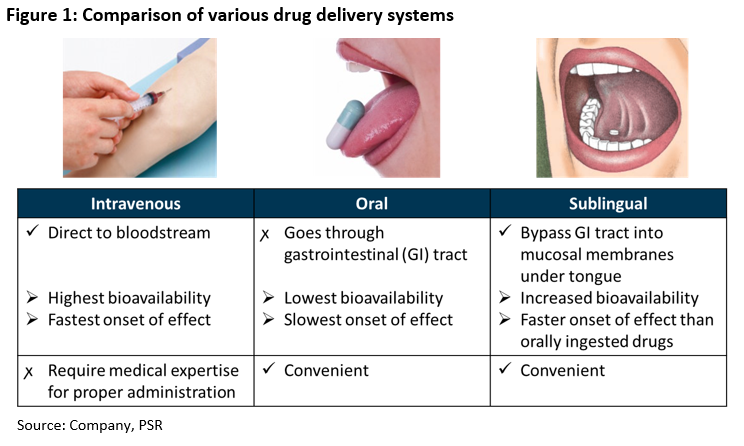

WaferiX is the company’s patented sublingual delivery system, which allows for the delivery of active drug compounds through a person’s rich supply of blood vessels under the tongue. This promotes rapid absorption of the active compounds in the bloodstream. Drugs that are delivered sublingually avoid challenges faced by drugs that are delivered intravenously or orally (Figure 1).

Drugs that are delivered intravenously can get into the human system the fastest. However, they are invasive and often require medical expertise for proper administration, which requires patients to be in a medical facility to receive the drugs. This results in greater inconvenience and higher costs.

While orally-ingested drugs are more convenient and inexpensive, certain active compounds are less effective as the drugs first have to pass through the digestive system. This results in slower and lower absorption as active compounds have to be broken down (i.e. low bioavailability).

In contrast, sublingual drugs are administered directly under the tongue. This offers convenience as well as higher bioavailability of the drugs. These two features are especially important for drugs that require a quick onset of action, such as for pain management.

The patents granted to iX Biopharma’s WaferiX formulation testifies to the uniqueness of its technology as well as WaferiX’s efficacy in facilitating the sublingual delivery of drugs. This differentiates WaferiX from other sublingual formulations in the market. Apart from its patented formulation, WaferiX’s proprietary freeze-drying production procedure also confers intellectual-property protection for the technology, further enhancing its appeal.

Business Model

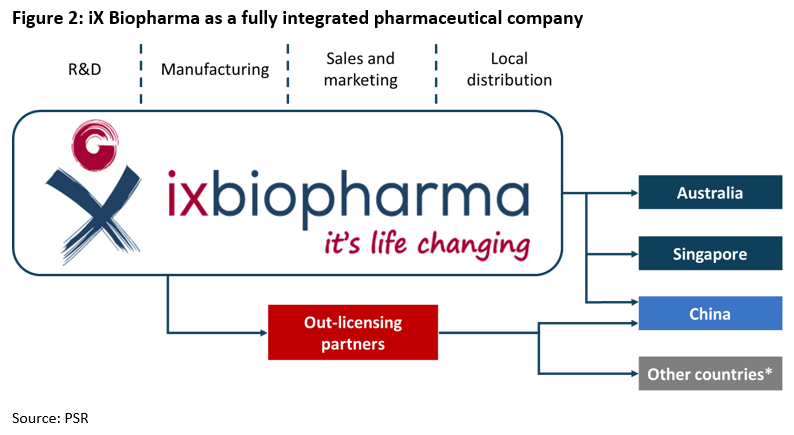

iX Biopharma is primarily a drug developer. It undertakes intensive research and development to incorporate its patented WaferiX in various pharmaceutical drugs. It also operates its own manufacturing and testing facility so as to retain proprietary production procedures. Products are sold to markets such as Australia, China and Singapore through various channels.

It sells its specialty pharmaceutical products in Australia as both registered medicines (Wafesil and Silcap) and unregistered medicine (Wafermine and BnoX) under Schedule 5A of Australia’s TGA. This schedule stipulates that therapeutic goods may be supplied to hospitals and clinics and bypass extensive developmental procedures, provided the drugs are manufactured in Australia and there are no listed or registered products in the market that are substantially similar.

The company’s range of nutraceutical products are sold directly in Australia through retail channels and in China and Singapore on e-commerce platforms, Tmall Global and JD Worldwide (Figure 2).

Out-licensing*: iX Biopharma is pursuing an out-licensing model for its products to penetrate more markets. Out-licensing will allow iX Biopharma to tap the expertise of its licensing partners throughout the developmental and commercialisation phases of a drug, thereby reducing costs and other associated risks.

An out-licensing deal will entail permission to use its trademarks, patents or technology under conditions spelt out in the deal. In return, the licensor will receive recurring milestone payments and royalty payments.

iX Biopharma has inked an out-licensing deal for Wafesil with China-listed Yiling Pharmaceutical (SZSE: 002603, Not Rated). Containing the active compound of sildenafil, Wafesil is a sublingual wafer used for treating MED. Yiling Pharmaceutical will have the rights to sell Wafesil post-product registration in China, while bearing the costs to bring the product to market.

iX Biopharma is also pursuing an out-licensing deal for Wafermine, its sublingual ketamine, for Phase 3 clinical development to treat acute moderate to severe pain. Due to a global need for effective non-opioid treatment of pain, a licensing deal for Wafermine, which will be the world’s first ketamine drug for pain is expected to dwarf its Wafesil out-licensing deal in licensing fees.

Business Segments

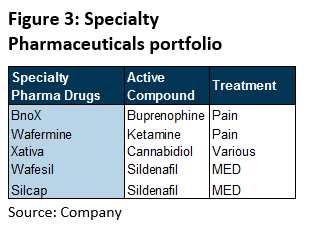

Specialty Pharmaceuticals: iX Biopharma manages five products under its specialty pharmaceuticals (Figure 3), targeted at the treatment of pain and MED as WaferiX is able to address the needs of patients conveniently with its quick onset of effects and other conditions with its medicinal cannabis product (see Appendix A for details).

Nutraceuticals: The company launched its nutraceuticals portfolio in FY18 which consists of health supplements marketed under Entity Health. Unlike traditional supplements which focus on specific ingredients such as vitamins or trace minerals, Entity nutraceutical products are formulated with the treatment of specific conditions in mind. They also benefit from the incorporation of WaferiX which provides for higher bioavailability than traditional health supplements (see Appendix A).

Investment Thesis

i. Out-licensing of Wafermine for Phase 3 clinical trials offers potential for multi-million-dollar licensing fees.

iX Biopharma successfully completed end-of-Phase 2 meetings with the US FDA for Wafermine in December 2019. It is pursuing an out-licensing agreement to see through Phase 3 studies and commercialise Wafermine.

Based on Wafermine’s demonstration of safety and efficacy in Phase 2b clinical trials, we believe its Phase 3 development – which will largely consist of replicating Phase 2b results on a larger scale – has a high probability of success.

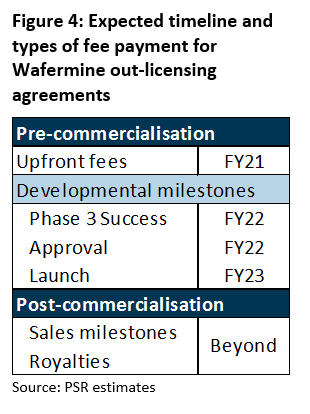

iX Biopharma is prospecting potential out-licensing partners. A successful deal will see the company license out the right to develop and sell Wafermine to other markets in return for licensing fees. Typically, fees include upfront and milestone fees. In the case of Wafermine, its fee schedule will include payments at several developmental milestones before commercialisation. Upon commercialisation, the company is also expected to receive royalty fees from sales plus additional payments upon certain sales milestones reached by its licence partners.

The company is currently in talks with prospective partners for an out-licensing deal. The expected cost of the Phase 3 development of Wafermine is US$25mn. We estimate that any out-licensing deal could be worth multiple times the cost of US$25mn, staggered over the entirety of the licensing agreement.

In addition, Wafermine is ready for Phase 2 clinical trials for the treatment of depression. This may boost the valuation of any deal with out-licensing partners should Wafermine be out-licensed for the development of both treatments.

ii. Planned production capacity by 2H21 to optimise operational efficiency and support sales.

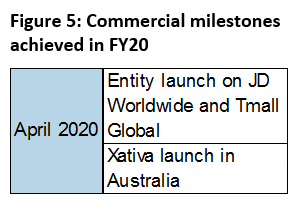

iX Biopharma’s revenue grew 47% y-o-y in FY20 as it shifted towards commercialisation of its products (Figure 5). It launched Entity flagship stores on two of China’s largest e-commerce platforms, JD Worldwide and Tmall Global, in April 2020. Its nutraceutical products, LumeniX and RestoriX, were sold out in less than three weeks of launch. Xativa, the first sublingual medicinal cannabis wafer in Australia as an unregistered medicine, also met with strong demand, with its initial production run selling out shortly after its launch in April.

As a result, 4Q20 revenue was S$0.56mn, up 327% QoQ. This contributed 57% to FY20 revenue. As current production capacity may hamper growth, the company plans to increase capacity by six-fold by 2H21. This is expected to support sales and turn the company profitable in FY22e.

iii. Clinical experience of working with drugs under development in Australia to accelerate commercialisation.

Many of the drugs that are in the development stage are already being supplied to the Australian market via Schedule 5A of its TGR. Under the regulation, drugs that are manufactured in Australia may be supplied to hospitals as unregistered medicine as long as there are no comparable substitutes in the market. This has allowed iX Biopharma to gather sufficient clinical evidence on the effects of its pharmaceutical drugs under development, including Wafermine and BnoX.

iX Biopharma is pursuing an out-licensing agreement to undertake Phase 3 development of Wafermine for the treatment of acute pain, while also ready for Phase 2 developmental studies for the treatment of depression. If it out-licenses the study of Wafermine concurrently for depression and acute pain, we see the potential for boosting the valuation of any out-licensing deal for Wafermine.

The company’s sildenafil wafer, Wafesil, is used for the treatment of MED. This has been out-licensed to Chinese pharmaceutical company, Yiling Pharmaceutical, for distribution in China. It is also being registered in the EU for sale and registration outcome is expected by 2H21. The product is pending registration in China and all costs to bring Wafesil to commercialisation in China will be borne by Yiling Pharmaceutical. iX Biopharma will only be responsible for manufacturing the drug after commercialisation.

iv. Novelty in WaferiX technology offers potential for future drug development.

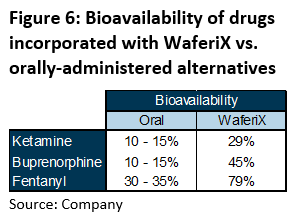

Apart from increased bioavailability when WaferiX is incorporated with drugs (Figure 6), WaferiX possesses high potency for application to active compounds in other drugs. As such, we see ample opportunities for iX Biopharma to incorporate WaferiX in off-patent drugs for the creation of new products in the market. Development risks and costs could be lowered as their active ingredient would have been well-studied for previous formulations.

Apart from WaferiX’s formulation, the company’s proprietary manufacturing procedures also confer intellectual-property protection. Patents that continue to be granted across the globe for this technology testifies to its novelty. Together with its potency for application in other pharmaceutical drugs, we believe the WaferiX technology will underpin income generation from future drugs development.

Financial Highlights and Forecasts

Revenue: Between FY18 and FY20, revenue grew at a CAGR of 100%. 4Q20 revenue of S$0.56mn accounted for 57% of FY20 revenue. As the company continues to push towards commercialisation, we forecast revenue of S$3.47mn for FY21e. This would be supported by a six-fold increase in production capacity by 2H21 and further expansion in FY22 (Figure 7).

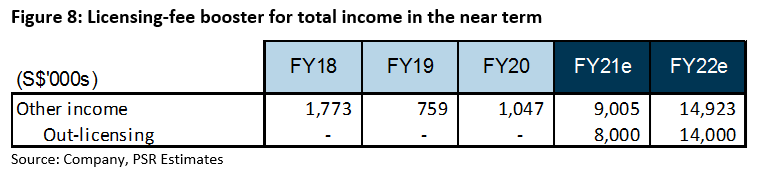

Licensing fees: A successful out-licensing deal to undertake Phase 3 development trials for Wafermine could mean licensing fees on top of other product sales. Estimated costs for the trials that will last between 12 – 18 months are around US$25mn, which will be borne by its out-licensing partner. Assuming the completion of a deal, we estimate licensing fees of S$8mn in upfront fees to be collected in FY21e. Our estimates are captured under ‘Other income’ in our financial estimates (Figure 8).

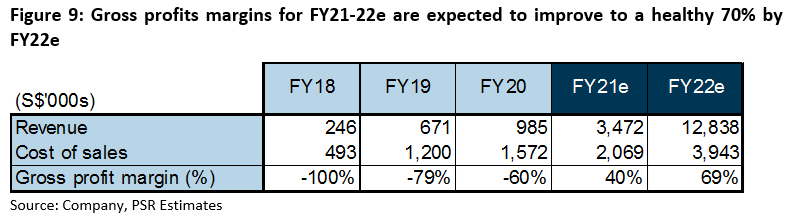

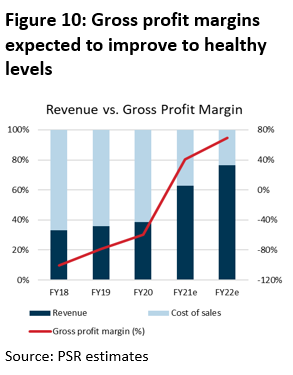

Margins: Gross margins were negative in the past three years due to the company’s high cost of sales. Cost of sales was high because of an overweight of fixed overheads to variable costs arising from low production capacity. The industry average for variable costs hovers at 20% of drug sales. Based on this, we estimate fixed overheads and staff costs of S$1.5mn per annum.

As iX Biopharma begins to ramp up production capacity for commercialisation, its gross margins have improved by around 20% per annum since FY18 (Figure 9).

FY21e margins are forecast at 40% to reflect the installation of additional freeze dryers, which would add 500% to production capacity and improve economies of scale. As operations stabilise, we expect margins to further improve to 69% in FY22e, which is on the conservative side in an industry whose margins hover between 80 – 85%.

Expenses:

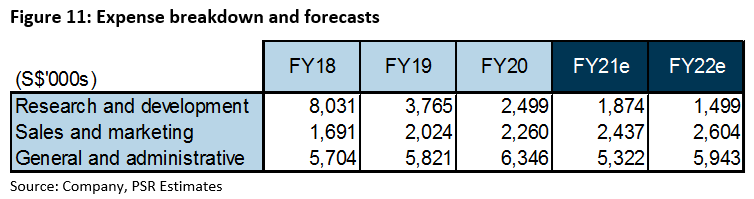

Research and development: Over the past three years, as the company actively developed Wafermine, R&D (Figure 11) formed the bulk of its expenses, at 35% of all expenses incurred between FY18 – FY20. With completion of Phase 2 development trials, R&D expenses are likely to taper off. As the success of Phase 2 trials testifies to the potency of the WaferiX technology, future out-licensing partnerships may involve cost-sharing of trials. This has the potential to reduce R&D expenses further. We conservatively forecast baseline R&D expenses of S$1.5mn for the next 2 years as we believe R&D will remain an integral part of its business in unlocking value from its patented WaferiX technology.

Sales and marketing: We expect sales and marketing expenses to continue to rise in proportion to its revenue, especially as Entity Health steps up its sales efforts on Tmall Global and JD Worldwide for nutraceutical products in China.

General and administrative: One-off expenses totaling S$0.53mn were incurred in FY20 in relation to its end-of-Phase 2 meetings with the US FDA. Stripping this out, general and administrative expenses would have been similar to previous years. We expect general and administrative expenses to normalise to previous levels in FY21-22e.

Balance Sheet:

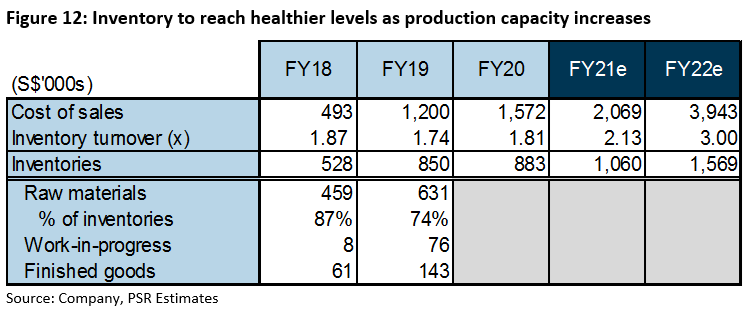

Inventories: iX Biopharma typically maintains high inventories, with more than 70% held as raw materials (Figure 12). Raw materials are typically bought in bulk for cost efficiency in the drug manufacturing industry. This, coupled with low production capacity, contributed to its low inventory turnover of below two times in the past three years.

However, as production capacity ramps up, we expect inventory turnover to improve and inventories to normalise in relation to cost of sales.

Investment Risks

Delays in out-licensing agreements may defer licensing fees and timeline to profitability. Due to the Covid-19 pandemic, time and resources in the global pharmaceutical industry have been channelled to the development of viable vaccines. This may delay iX Biopharma’s licensing timeline as potential licensing partners may give priority to the development of Covid-19 vaccines. iX Biopharma may thus book losses in FY21e instead of profits, as we currently forecast.

Sustained demand for products. Due to its high proportion of fixed overheads and R&D costs, profitability will hinge on the sustained success of its products in various markets. Excluding licensing fees for products under development, achieving breakeven sales in its current market holds the key to its profitability.

Currency translation risks. As iX Biopharma sells primarily in Australia, it is exposed to currency risks. Its FX exposure is likely to increase with further expansion in China, the EU etc.

Valuation

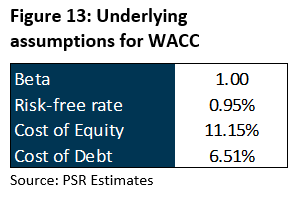

We initiate coverage of iX Biopharma with a BUY rating and target price of S$0.455, derived from DCF valuation. We assume:

DCF valuation was applied to forecasts for the next three years as we believe FY23 will be the year of completion and commercialisation of Wafermine. This is when income could become more normalised.

Our target price implies a forward PE ratio of 288.3x, which we believe is not demanding as we expect iX Biopharma to break even in FY21e. If there is any favourable out-licensing deal and if sales normalise by FY22, our target price will translate into 12.0x FY22e PE for a ROE of 40%. Further development of novelty drugs is expected to provide earnings upside beyond FY22.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: