The Positives

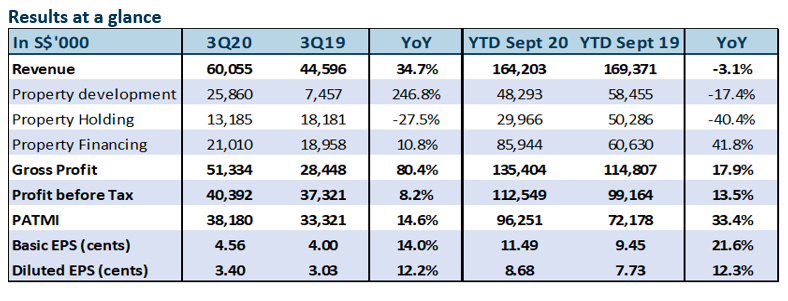

+ Robust 3Q20, notwithstanding Covid-19. 3Q20 revenue rose 34.7% YoY, led by more carpark lots sold at its Millennium Waterfront project (Plot A: 1091; Plot C: 882) which have zero carrying book costs. 9M20 topline held up, largely due to a 41.8% YoY increase in property financing revenue. The increase was aided by one-off loan restructuring income of S$15.5mn and establishment fees from its new development venture in Australia.

+ Better-than-expected property holdings. Its two Wenjiang hotels made a combined gross operating profit of RMB6.7m during the quarter, up 39% YoY. European hotels were mixed. While most of its non-core-city Bilderberg hotels and Bilderberg Bellevue Hotel Dresden in Germany benefited from local leisure demand during summer, its two core-city Bilderberg hotels in Amsterdam and Rotterdam were hit by low corporate demand. Nevertheless, the European hotels made a gross operating profit of €3.9 mn for 3Q20 vis-à-vis -€3.6mn in 1H20.

+ 14.8% YoY DPS growth registered in FY20e. In lieu of a final dividend, FSG has announced a second interim cash DPS of 2.0c for FY20, bringing total DPS declared YTD to 3.1c. This is 14.8% higher than the FY19 full year DPS of 2.7 cents. FSG will work towards a stable dividend payout with a steady growth when appropriate, subject to prevailing market conditions.

The Negatives

– Financial subsidies from governments which cushioned hotel losses to taper off. FSG’s European hotels are being supported by subsidies from the German and Dutch governments, which provided a €4.9mn cushion to the hotels’ gross operating profits. The Dutch government recently announced Temporary Emergency Measure for the Preservation of Jobs (NOW) 3, which is less generous than NOW 1 and 2. NOW 1 and 2 allowed claims of up to 90% of a company’s wage bill, depending on loss of turnover. Under NOW 3, the wage claim is capped at 80% and will be decreased every three months: from 80% to 70% and to 60%.

Mixed outlook due to European hotels

Dongguan still vibrant. The Dongguan property market continues to see overwhelming demand for the residential properties and unwavering strength in the selling prices. Most inventories at FSG’s existing projects that were eligible for presales – Star of East River, Emerald of the Orient and the Pinnacle – were sold as of 3Q20. Some properties that are ineligible for presales have also been pre-booked 2-5 years in advance with upfront cash deposits. According to FSG, over 7,000 interested applicants have registered for the presales of 830 units at its upcoming Skyline Garden project. Presales are expected to commence next month. FSG is confident that the units at Skyline Garden will see good buying interest.

Humen TOD project to be the key project from FY21 onwards. Construction work has begun for the first sector of its newly-acquired Humen transit-oriented development project. Sector 1 has a land area of c.46,300 sqm and constitutes c.231,500 sqm of the 1mn sqm GFA project. We are expecting completion of this sector to bring in c.S$220-230mn of gross development value upon handover in 2022/2023 as the progressive launch of this project is expected to commence in the second half of 2021.

Possible Plot E Sale. The company announced it has been approached by an independent third party with regard to Plot E of the Chengdu Millennium Waterfront project. Plot E is expected to

comprise three blocks of approximately 2,900 SOHO units and an elder care centre of total 304,300 sq m (includes a hospital building of 69,500 sqm), 91,800 sqm of commercial / retail space

and 3,200 underground carpark lots. Upon completion, we are expecting the handover to bring in c.S$630-640mn of gross development value.

Property financing is stable. With regards to FSG’s property financing business, its PRC loan book remained steady at RMB2295.3mn. While FSG continues to receive requests for loans, it remains selective as it is looking to pace its loan growth with its property development business.

Hotel woes. As the number of Covid-19 cases in Europe continues to spike, we are less optimistic on its European hotels, even for the ones located away from cities. 3Q20 occupancy at its Bilderberg Bellevue Hotel Dresden was in the mid-70s to high 90s everyday, as it benefitted from being in the countryside. These numbers have since tumbled to the low 60s-70s. At its key Amsterdam and Rotterdam hotels, occupancy was low teens on good days and low single digits on other days. These hotels would be affected when subsidies from the government dwindle in the coming months. We expect some mark-downs in the fair value of the hotels at year end. A 3% decline in hotel investment properties implies a c.S$1.8mn impact on revenue (FY19 hotel revenue: S$60.8m).

Covid-19 has driven more hotels into liquidation. Some lessees are also looking to return their operating leases. With cash of S$474.9mn and low net gearing of 0.12x, FSG has the balance-sheet strength to pursue opportunities. In October, it successfully refinanced S$50.5mn worth of debt and upsized its revolving credit facilities by S$124.5mn. Coupled with undrawn facilities and potential equity infusions from the exercise of outstanding warrants, FSG is exploring new business opportunities.

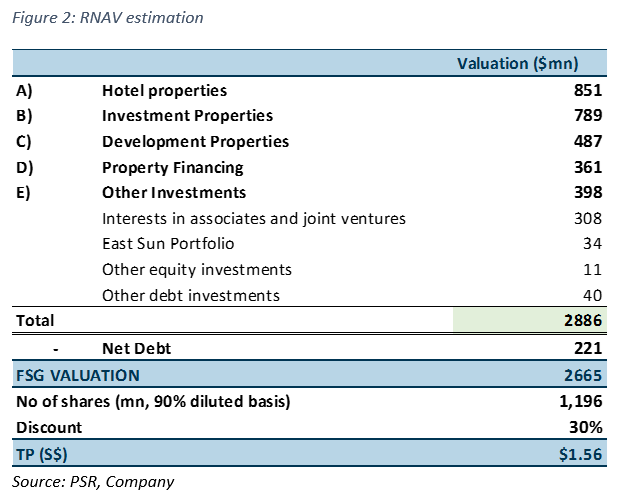

Maintain BUY with revised TP of S$1.56. Our target price implies a total potential return of 24.3% and dividend yield of 2.4%. It remains based on a 30% discount to FSG’s diluted RNAV per share. Our new TP is based on its enlarged share base after its 1:4 bonus warrant issue announced on 23 July, factored on a 90% diluted basis (1196mn) from 100% previously. Unexercised warrants total 416mn, which increase issued ordinary shares to 1,329mn on a fully diluted basis (1H20: 1,102mn). Based on its current 912mn shares, our TP is S$2.04.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: