The Positive

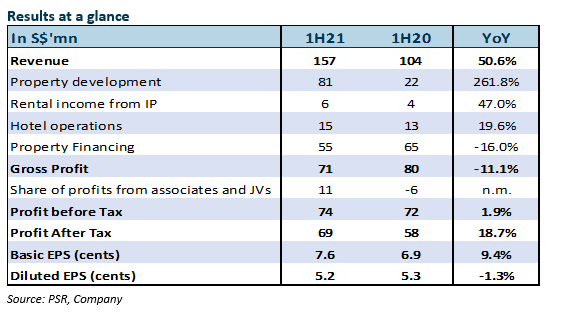

+ Strong property development revenue. Group revenue increased 50.6% YoY from a 262% YoY jump in property development. This was largely attributable to the handover of 619 SOHO loft units at Plot F of its Millennium Waterfront project. Hotel revenue was up 19.6% as a result of a relaxation of Covid-19 travel and lockdown restrictions in the PRC, Netherlands and Germany. This was offset by lower property-financing revenue following an absence of a S$15.8mn one-off loan-restructuring income arising from the refinancing of loans to 33%-owned FSMC last year. As such, gross profit came in lower, as property financing has the highest gross margins. 1H21 profit after tax increased 18.7% YoY, capturing a higher share of profits from associates and JVs and lower tax expenses.

The Negative

– Tenant exploited loopholes. In May 2021, TVHG Budget Amsterdam II B.V. (TVHG), the tenant of two hotels at the Arena Towers in Amsterdam Southeast, commenced preliminary relief proceedings against FSG’s wholly-owned subsidiary for partial rent suspension until such time when Covid-19 restrictions are lifted or the hotels’ turnover returns to pre-Covid-19 levels. On 9 June 2021, an Amsterdam preliminary relief judge issued a ruling in favour of FSG, rejecting all of TVHG’s claims. While the deadline for TVHG’s appeal has expired, there is no assurance it will not pursue further legal action to seek rent discounts. FSG, however, has a 3-month bankers’ guarantee and a clause to terminate its contract with TVHG should the tenant default on its lease obligations. Given this, FSG believes that TVHG will continue to pay its rents in the meantime.

|

Outlook Dongguan residential market remains hot. Despite cooling measures by the Dongguan municipality, Dongguan’s residential units are still well-sought by developers and buyers alike. In 1H21, there was a tender for a plot of land in Dongguan. Bidders were required to employ at least a certain number of employees to ensure that they were not paper companies and place RMB1bn as deposits. Even though its location pales in comparison with Humen, residential prices are still transacted at around RMB30,000 psm ppr in the region. The authorities received over RMB200bn of deposits. Simply put, there were over 200 bidders for the project. Underscoring the area’s popularity, FSG has divested equity interests in some of the properties in East Sun Wan Li portfolio at 100-219% premiums over their book value.

1H21 development sales yet to be recognised amounted to S$559mn. FSG’s share of GDV yet to be unlocked from existing projects was S$3.4bn. This included its new Humen Boyong project which is expected to add S$310mn to its gross development pipeline, excluding the renamed Bolong Bay Garden (formerly New Humen) and City Tattersalls projects. Both are expected to contribute more to property financing.

On 28 July 2021, the group set up a JV to acquire and redevelop two adjacent plots of mixed-use land in Humen, Dongguan. The project will have saleable GFA of 110,000 sqm, comprising 75% of residential GFA and 25% of commercial GFA. All-in land cost is estimated at RMB15,000 psm ppr. This marks the group’s fourth acquisition in the Greater Bay Area this year. Construction and presales are expected to commence in 4Q21 and 3Q22 respectively. FSG has an effective stake of 48% in the JV.

European hotels expected to pick up. As Covid-19 infection rates have dwindled from their recent high, lockdown measures in the Netherlands have been eased once again. From 27 July 2021, all vaccinated European citizens from the European Economic Area and Schengen Zone are allowed to enter the country, regardless of their countries’ infection rates. The change follows successful vaccination campaigns in these countries, where about 50% of their populations have been vaccinated. We anticipate a greater recovery for FSG’s hotels in the coming quarter. In particular, those located at city fringes should perform better on the back of increased leisure travel during the summer holidays.

Property financing’s PRC order book growing; auction sale of defaulted loan expected. Excluding a one-off loan-restructuring income from the refinancing of FSMC loans and establishment fee from the provision of a A$370 mn construction facility to fund the redevelopment of the City Tattersalls Club development project last year, 1H21 property financing income increased S$8.5m YoY. This was spearheaded by higher average returns from its PRC property-financing business. 1H21 average PRC loan book grew 22% HoH with the aid of more development and financing deals.

Separately, FSG had commenced legal action in November 2020 against a borrower group in a Shanghai court to recover a RMB330mn loan and associated interest under two cross-collateralised loans with an average loan-to-value ratio of 53%. In March 2021, FSG entered into a settlement with the borrower group. Principal terms of the court ruling included a repayment schedule for the loan principal and interest, including default interest. However, the borrower group failed to make its fourth instalment payment fully on 30 June 2021. On 12 July 2021, FSG filed a court application to seek an auction sale of the mortgaged assets in accordance with the court ruling. We are expecting principal and interest to be fully collected by next year, subject to court-application success. |

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: