The Positives

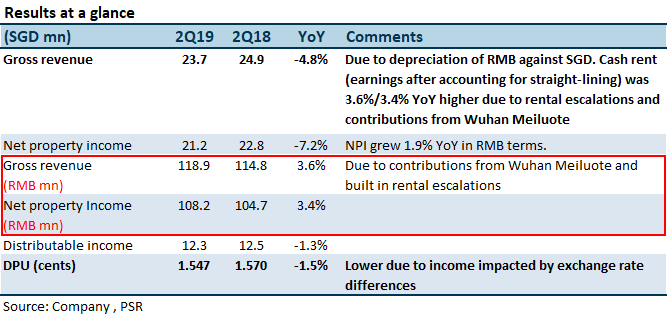

+ High income visibility due to portfolio occupancy of 99% (63% of NPI underpinned by master leases), and WALE by GRI of 4.6 years. Including the newly-acquired Fuzhou E-commerce asset (acquisition to be completed by August 2019), 63% of NPI will be secured by master leases to the Sponsor. Hengde Logistics, the specialised logistic asset customised and leased to a state-owned tobacco company, contributes c.15% to NPI. Due to the state-ownership, we view the tenant quality at Hengde as high and will not pose any risk to revenues. All assets are at 100% occupancy except Wuhan Meiluote (85.8%).

The Negatives

– Cost of borrowing for 2Q19 increased by 40bps from 4.1% to 4.5%. The quantum of the standby letter of credit (SBLC) facility was raised to S$120mn from S$50mn a year ago. Interest rates were also higher (2Q19: 1.9%-2.6%, 1Q19: 1.1%).

– Occupancy at Wuhan Meiluote fell 13.8pps QoQ due to non-renewals. This asset contributes only c.S$0.7mn (1.7%) towards NPI. It consists of a warehouse, auxiliary office building and a dormitory. Around 6,000 sqm of warehouse space was vacated in 2Q19. There are encouraging enquiries to fill up space in this asset.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.

Outlook

ECW successfully refinanced all the onshore and offshore loans maturing in July 2019. This represents 100% of ECW’s existing borrowings. The quantum of loans has been increased from c.S$402mn to c.S$640mn (of which S$547mn has been drawn down). The higher loan quantum comprises acquisition financing for the Fuzhou E-commerce asset. While the interest rate was not disclosed, the cost of borrowing could be similar to the previous quarters (1Q19: 4.1%). The proportion of onshore and offshore loans has been altered, from 50:50 to 66:33 in favour of SGD loans. This will help to maintain the cost of borrowing given the increase in interest rates on RMB denominated loans vis-a-vis the lower interest on SGD denominated loans. ECW’s cost of borrowing in SGD/RMB was 4.1%/5.4% p.a. for the quarter ended June 2019.

Two leases with below market rents will expire in 2020 and 2021 – one lease at the Hengde facility and the second lease to one of the anchor tenants at Wuhan Meiluote, which is c.25% below market rent. Renewal at market rents represents a positive reversionary potential for the REIT.

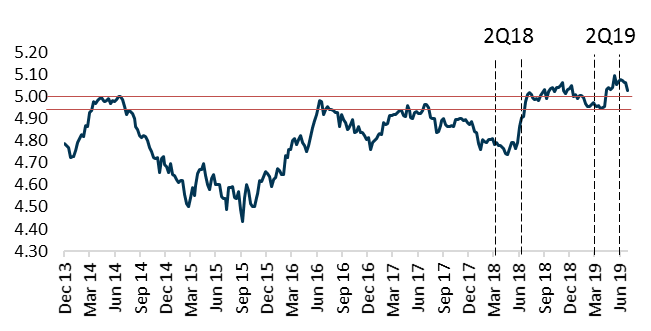

A tail risk to our valuation remains the weakening of the RMB. The fresh bout of trade war tension these past few days saw the RMB crossing the psychological level of 7.0 against the USD. Despite the headlines, SGDRMB pair was only down 2.1% YoY.

Figure 1: SGDRMB currency pair – RMB has depreciated 2.1% YoY against SGD

Source: Bloomberg, PSR

Figure 1 shows the prices that the SGDRMB pair has been trading at, with emphasis on the 2Q18 and 2Q19. The area between the red lines indicates the put spread hedge for the quarter ended June 2019. ECW hedges 75% of distributable income on a 6-month rolling hedge using put spreads. The hedging strategy employed means that the REIT will accept the FX fluctuations within a collar and remain protected when the SGDRMB pair moves strongly against (as well as in favour of) them. The cost of implementing the put spread strategy is 50% the cost of the forward hedge strategy. Conversely, it takes away the upside potential when the currency moves in favour of them. The management is re-evaluating their FX hedging strategy in light of the increased FX volatility.

Maintain Buy with unchanged higher TP of S$0.87.

We maintain our BUY call with an unchanged TP of S$0.87. ECW currently trades at an attractive yield of 8.7% and a FY19e P/NAV of 0.87x.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: