What were the key takeaways from DBS Investor Day?

DBS’ Investor Day main theme was digital strategy and how it is applied to different markets to drive the bank forward.

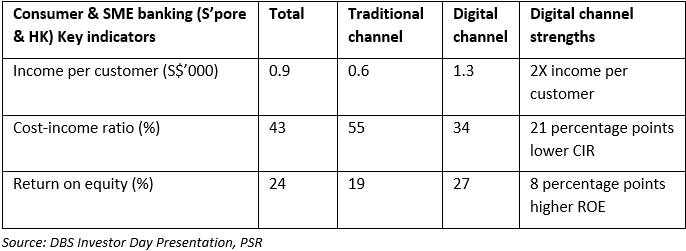

Digital strategy 1: Consumer/SME banking in Singapore and Hong Kong. DBS is adopting the digital platform approach to engage their customers and digitising their banking processes. The aim is to pre-empt new digital disruptors in the legacy markets where DBS is an incumbent. The digital process reduced the cost to income ratio from 49% in 2015 to 43% in 2017 as income growth outpaced cost growth and ROE improved from 22% in 2015 to 24% in 2017. DBS aspires to improve the cost-income ratio further to less than 40%.

Digital strategy 2: Consumer/SME banking in growth markets including India and Indonesia. DBS is using the digital approach to acquire clients at a low cost and achieve scale in product distribution. The aim is to disrupt the banking incumbents in the growth markets that have large swathes of physical branches. Fighting head on with physical branches in these growth markets would be uneconomical and less effective. Income from Consumer & SME banking in growth markets including India and Indonesia is expected to grow 20% CAGR.

Digital strategy 3: Corporate banking, Private banking, Markets and Others at group level. Private banking and cash management have experienced higher transaction turnover as digital platforms keep clients engaged and client-initiated transactions increase.

What is our outlook?

We have increased our DBS ROE expectation for FY18e from previous estimate of 12.1% to 13.1% as the economies in DBS’ main markets of Hong Kong and Singapore remain vibrant. In particular, Singapore 3Q GDP growth surpassed expectations with a 5.2% increase YoY. Our revised ROE estimate is due to our expectation that the strong economy continues to be supportive of stronger pass-through of higher interest rates. As a result we increased our FY18e total income estimate by 4.5% and PATMI estimate by 8.4%. The high double digit growth in FY18e PATMI is mainly due to absence of lumpy provision expense in FY17

Investment Actions

Maintain “BUY” rating with a higher target price of S$29.30 (previous TP S$26.83) based on Gordon Growth Model

Details on the key takeaways

Consumer & SME banking (Singapore and Hong Kong) income grew 11% CAGR from 2015 to 2017 because of the growth from digital channel. The digital channel grew 23% CAGR from 2015 to2017 compared to the -2% CAGR growth at the traditional channel. The digital channel also produced a higher ROE of 27% than the 19% ROE at the traditional channel. By 2017, the digital channel contributed to 60% of the Consumer & SME banking (Singapore and Hong Kong) income, an increase from 49% contribution in 2015.

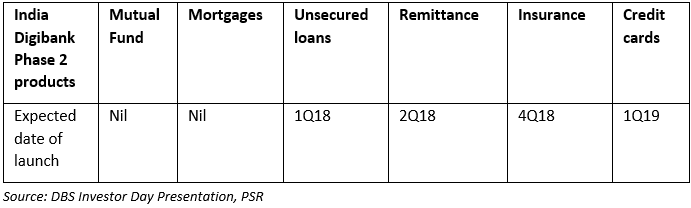

Consumer banking in India is gaining traction. Though it is still loss-making (losses undisclosed), we expect to see profit growth by end of 2018. Since the launch of digibank India in April 2016, DBS has been rolling out its phase 1 products which are savings accounts and time deposits and electronic payment services. By Oct 2017, the pace of client acquisition had almost trebled to a 3 month moving average of c.40,000 from c.15,000 in Aug 2016. Cumulatively, digibank India has 1.5 million customers as of Oct 2017. The value of transactions per month has increased 11 fold from Aug 2016 to reach c.S$160mn in Oct 2017. However, the profit drivers will be coming from the phase 2 products. Phase 2 products will roll out gradually, starting as early as 1Q 2018. DBS launched the digibank Indonesia in Aug 2017 with the intention of replicating the digibank India strategy but with some changes tailored to the culture and social norms of the Indonesian people.

DBS’ SME banking in India has found a strong local partner. Presently, the number of small SME (valued at S$1mn to S$5mn) in DBS’ India portfolio is 2.5mn. With the partnership with Tally, a leading ERP company in India, we expect DBS to gain access to customers in Tally’s portfolio amounting to 8mn customers. Tally has 70% market share in India’s SME space. DBS’ value proposition to Tally is the provision of banking products and services to Tally’s customers to create in integrated ERP plus banking platform. In return, DBS will be able to leverage on Tally’s extensive distribution network of more than 2,000 certified channel partners and 30,000 sales agents to scale up client acquisition. DBS is also a leader in technology as it has developed standardised ERP API for easy integration, user-friendly mobile applications and has the highest encrypted security standards. Therefore even as the partnership is not exclusive, we believe DBS’ value proposition is sufficiently robust to fend off competing banks.

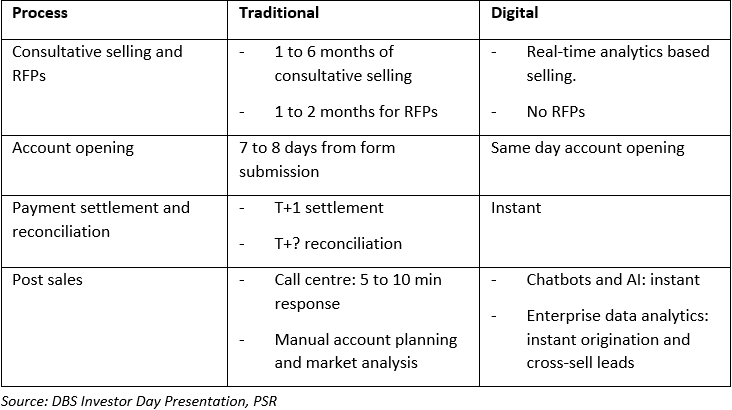

Cash management transactions turnover increased because digital capabilities reduced duration of sales cycle, client onboarding, payment settlement & reconciliation and post sales services.

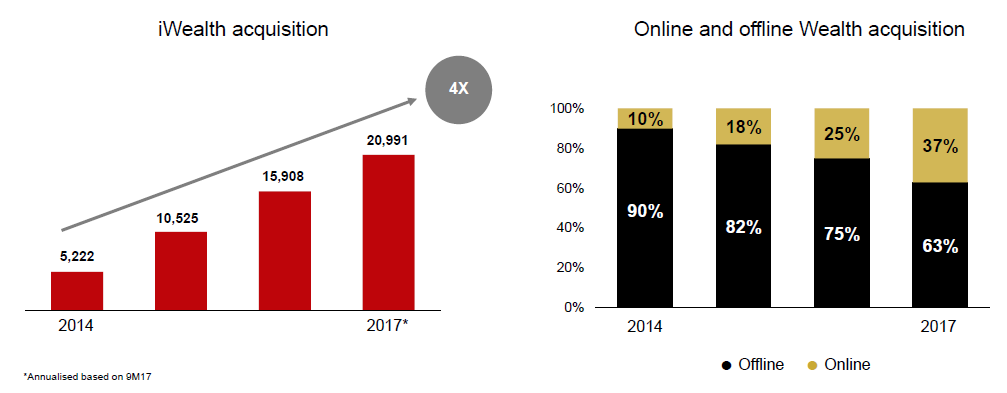

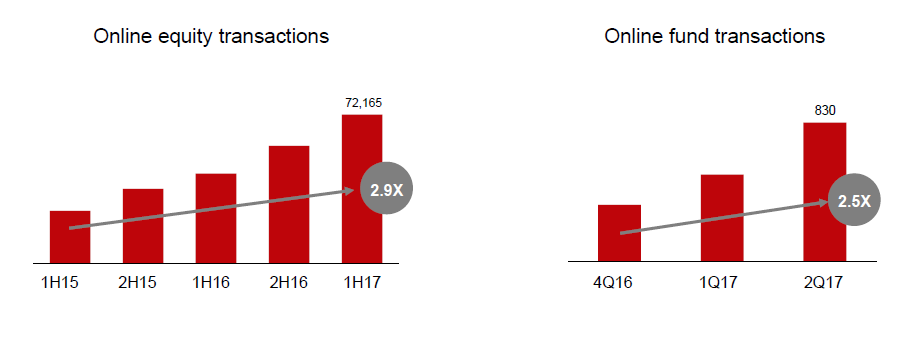

Digital capabilities improve WM client transaction turnover, client acquisition and client engagement. The digital capabilities allow clients to execute straight-through transactions especially in higher margin structured products. Time for client acquisition has shortened because of the digital onboarding process. Client engagement has also become more efficient as client’s data is integrated into the digital platform for easy access.

Figure 1: WM client acquisition increased 4 times since 2014 with the online acquisition channel becoming more dominant.

Figure 2: WM digital transactions growth has accelerated in the last 2 years

Source: DBS Investor Day presentation

Figure 3: Digitally engaged WM clients are multiple times more profitable and more active compared to non-digitally engaged clients.

What do we think of the digibank strategy?

We are excited about the digital push into the growth markets (namely in India and Indonesia) and also because the execution of phase 2 projects in India is imminent. Presently, the growth markets are still loss-making at the net profit line but the expectation is for growth market’s total income to grow more than 20% CAGR in the next 5 years. Growth markets total income as of 1H17 is about 4% of group total income so it has the potential to contribute up to 10% of DBS group total income and its ROE is also expected to exceed 10% in 5 years.

We think that the conditions are particularly favourable for digital push into India because of the mandatory Aadhaar system to all the residents of India and the ongoing banknote de-monetisation in India. The Aadhaar system is a 12-digit unique identification number that is linked to the resident’s basic demographic and biometric information such as photograph, fingerprints, iris scans which are stored in a centralised database. With the advanced and comprehensive digital identification infrastructure and expected increase in digital payments as a result of the banknote de-monetisation, it is highly plausible for DBS to successfully acquire clients digitally at partnering retail outlets where consumers make purchases of goods and services – a strategy that DBS is already carrying out.

We are also cautiously optimistic that digibank India could outperform management’s expectations because DBS, being a leader in digital banking technology, has a first mover advantage into a large Indian population that is young and IT savvy.

Jeremy covers primarily the Banking and Finance sector. He has 6 years’ experience in equities related dealing and research roles.

He graduated with Bachelors of Mechanical Engineering from Nanyang Technological University.