The Positives

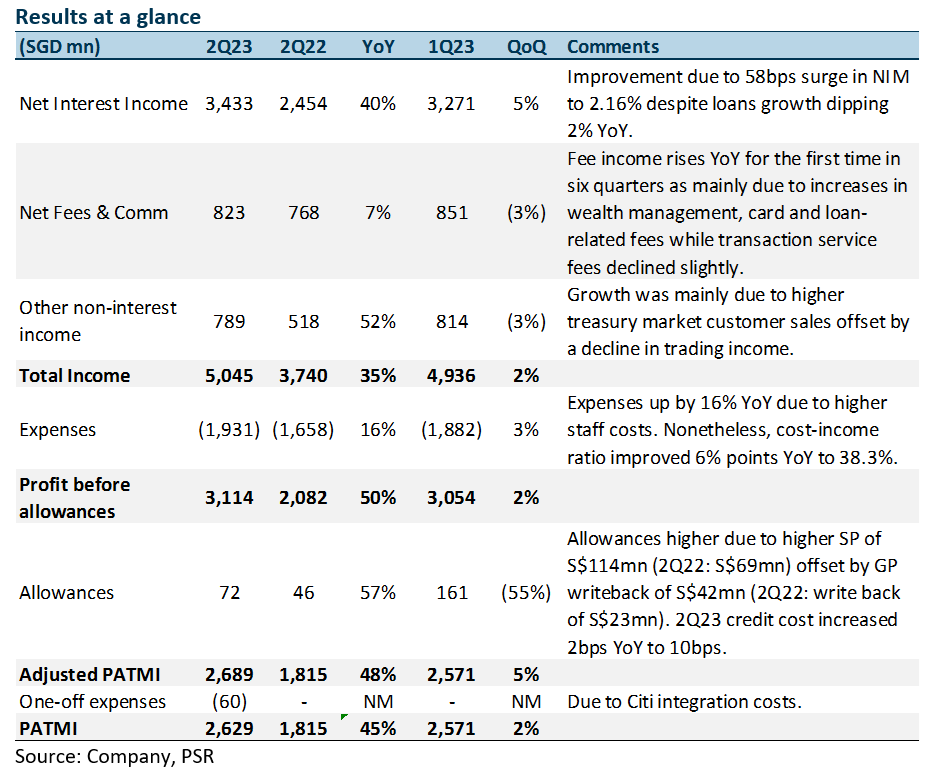

+ NIM and NII continue to increase. NII spiked 40% YoY to S$3.43bn due to a NIM surge of 58bps YoY to 2.16% (3Q22: +32bps, 4Q22: +15bps, 1Q23: +7bps, 2Q23: +4bps) despite loan growth dipping 2% YoY. Increases in non-trade corporate loans were offset by lower trade loans. Housing loans were stable, while wealth management loans declined modestly. Management spoke of an upside bias to NIM from its current levels and indicated that NIM will likely peak in 2H23.

+ Fee income rose 7% YoY, first in 6 quarters. Fee income increased 7% YoY, the first YoY increase in six quarters. WM fees increased 12% YoY to S$377mn from higher bancassurance and investment product sales. Card fees grew 17% YoY to S$237mn from higher spending including for travel while loan-related fees rose 17% YoY to S$133mn. These increases were moderated by a 5% YoY decline in transaction service fees led by trade finance.

+ Other non-interest income rose 52% YoY. Other non-interest income rose 52% YoY mainly due to an increase in net trading income from higher trading gains and an increase in treasury customer sales to both wealth management and corporate customers. Additionally, gains from investment securities more than doubled due to improved market opportunities.

The Negatives

– Allowances rose 57% YoY. 2Q23 total allowances were higher 57% YoY due to an increase in SP to S$114mn (2Q22: S$69mn) offset by higher GP write-back of S$42mn for the quarter (2Q22: write-back of S$23mn). Resultantly, 2Q23 credit costs rose by 2bps YoY to 10bps. Nonetheless, the NPL ratio declined to 1.1% (2Q22: 1.3%) as new NPA formation fell by 39% YoY. GP reserves rose slightly to S$3.80bn, with NPA reserves at 127% and unsecured NPA reserves at 224%.

– CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 14.9% points YoY to 51.5%, mainly due to the high interest rate environment and a continued move towards fixed deposits (FDs). Resultantly, total customer deposits fell 2% YoY to S$520bn as the decline in CASA deposits were partially offset by growth in FDs.

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.