Company Overview

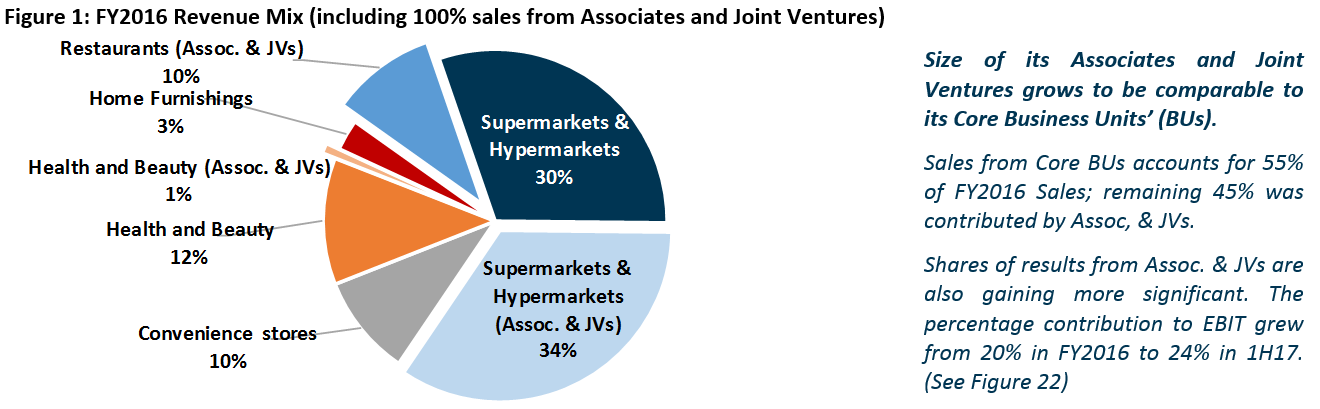

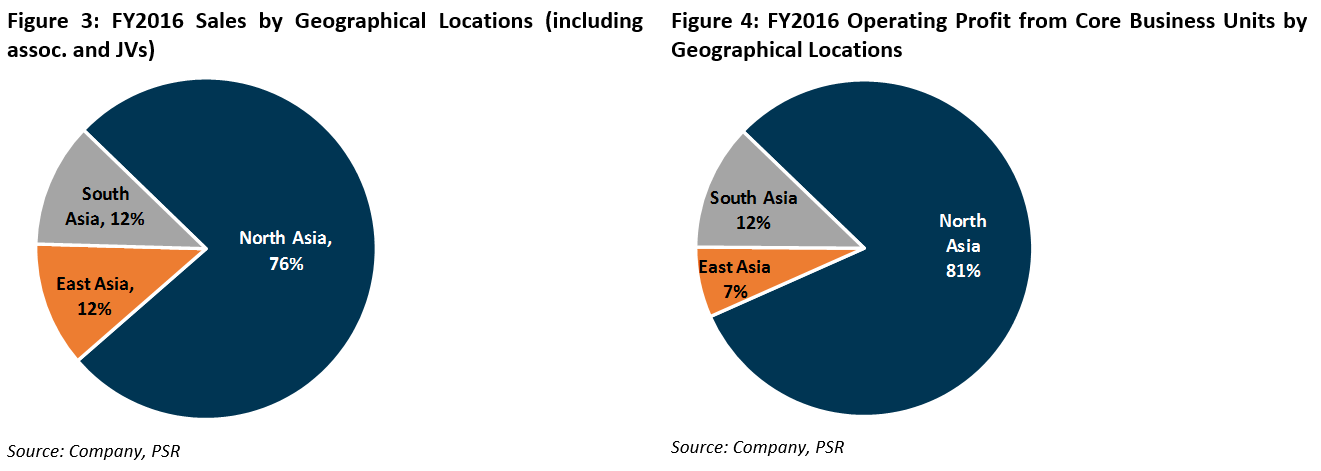

Dairy Farm International Holdings Limited (“Dairy Farm”) is a leading Pan-Asian retailer. The Group, together with its associates and joint ventures, operated over 6,600 outlets across 12 markets, with FY2016 total sales* exceeding US$20bn.

* Total sales include 100% revenue of its associates and joint ventures

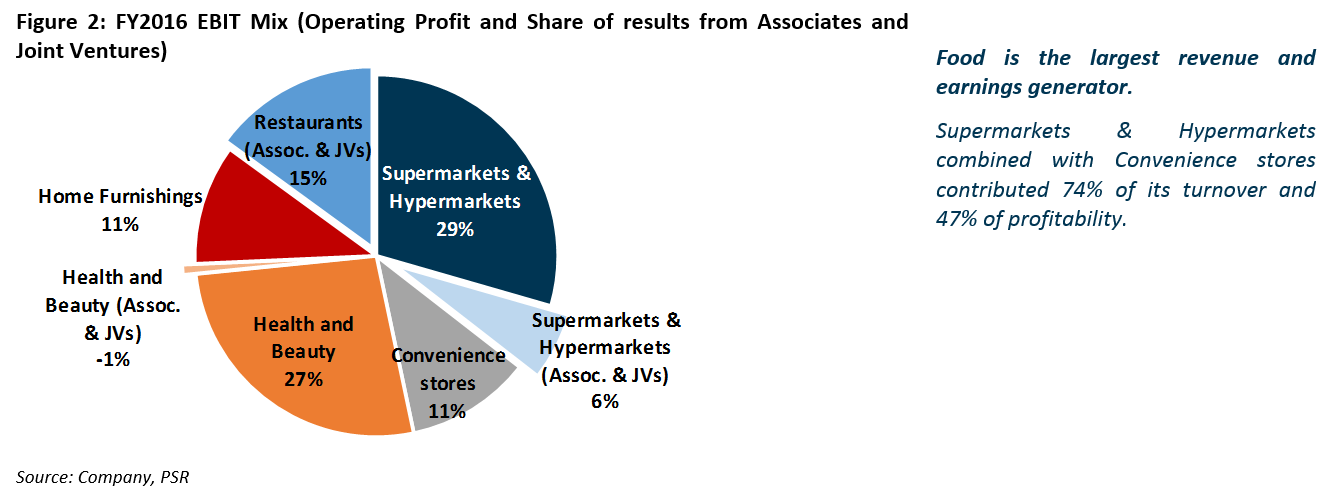

Its four divisions include: 1) Food (Supermarkets, Hypermarkets and Convenience Stores); 2) Health and Beauty; 3) Home Furnishings (IKEA businesses); and 4) Restaurants (Maxim’s, a leading Hong Kong restaurant chain).

Dairy Farm is incorporated in Bermuda and has a standard listing on the London Stock Exchange, with secondary listings in Bermuda and Singapore. It is a member of the Jardine Matheson Group.

Investment Thesis

Key Investment Risks

Business Overview

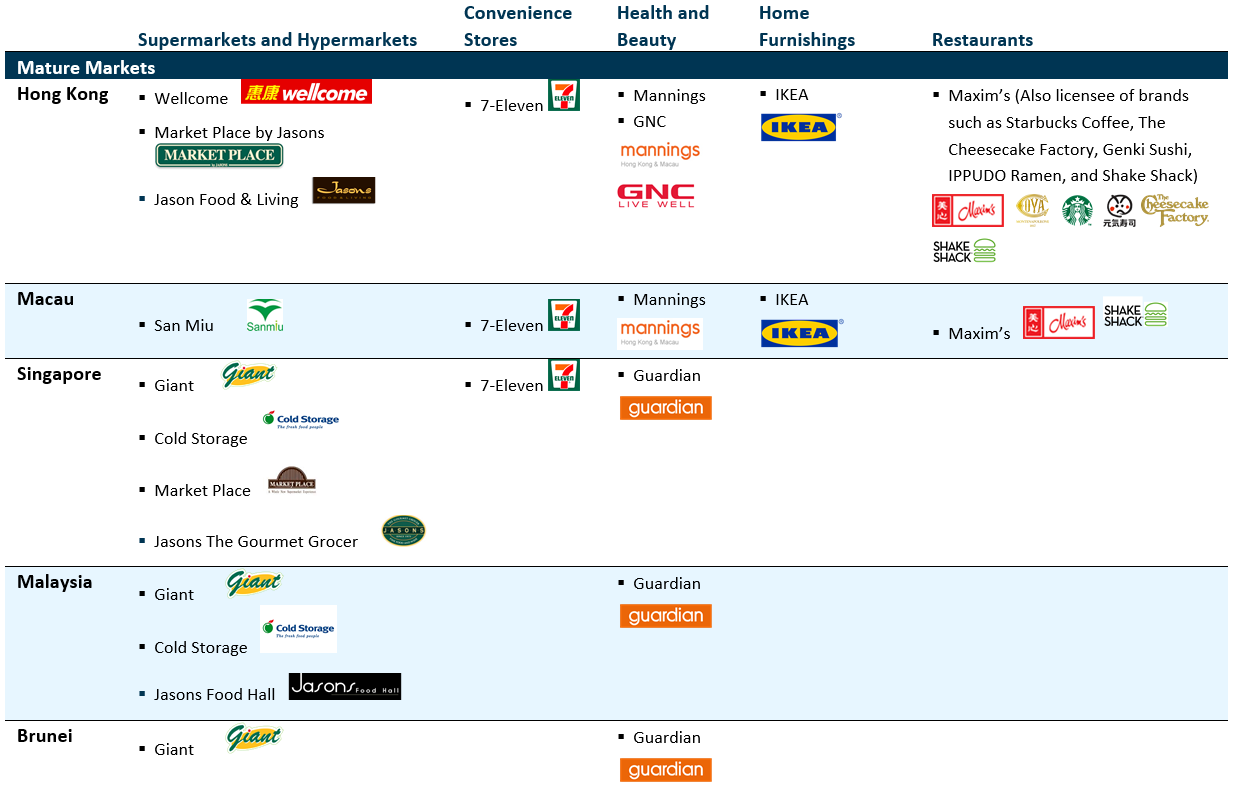

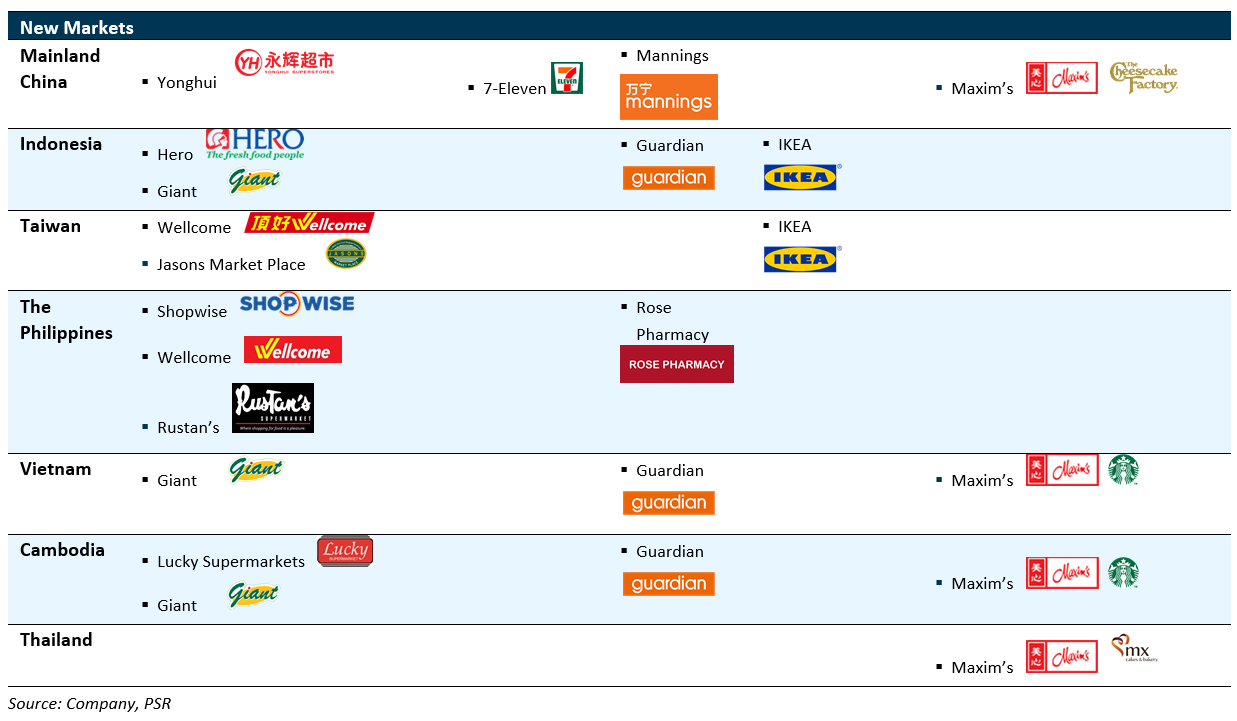

At 30 Jun-17, Dairy Farm and its associates and joint ventures operated over 6,600 outlets across 12 markets, and employed over 180,000 people.

The Group operates under a number of well-known brands across four divisions, namely Food, Health and Beauty, Home Furnishings, and Restaurants.

Figure 5: Regional Footprint and Principal Brands

Investment Thesis

Margin gains and store expansion plan to fuel medium-term growth

Dairy Farm is constantly investing to enhance its competitive position, increase customer convenience and adapt to emerging consumer trends. We think that the Group is poised to ride the macro tailwind in Asia’s developing markets.

1. Margin enhancement on the back of (a) better sales mix of higher margin products, and (b) improving economies of scale

a) Increase Fresh participation and moving into upscale market

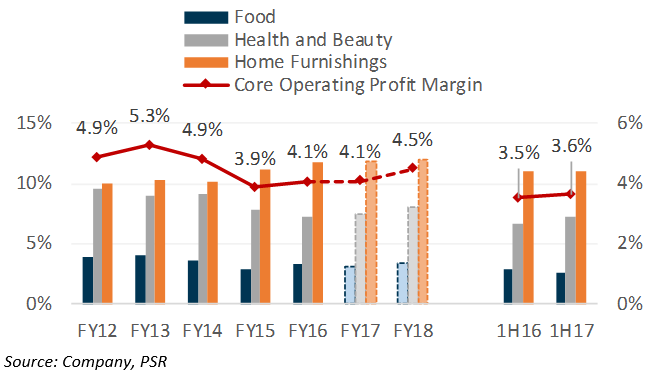

Figure 6: The better gross margins will lift Core EBIT margin to 4.5% by end-FY18e

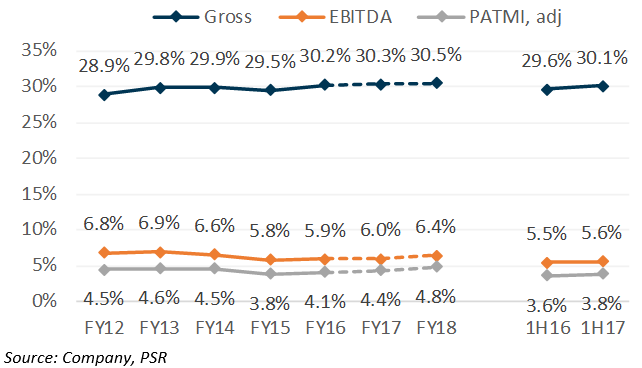

Figure 7: Stronger contribution from its Associates and Joint Ventures will prop up another 20bps p.a. at net margin level in FY17-18e

Over the past three years, the Group has integrated Fresh Production Centre and the Dry Distribution Centre in Taiwan (2014); opened three distribution centre hubs in Indonesia (2014); and commenced a new Fresh Food Distribution Centre in Singapore (May-16). These translate to a higher Fresh penetration, which increased by over 20 bps in the FY2013-16.

Management shared that its Fresh participation rate is still lagging behind NTUC Fairprice and Sheng Siong, despite being the second largest retailer in Singapore. Nonetheless, the new 75k sqft fresh food distribution centre in Singapore should level its playing field with NTUC Fairprice and Sheng Siong, and bode well with its plan to increase fresh participation. Management shared that lead time from farm to shelf in Singapore has shorten by 50%. The additional capacity also enables higher value food production – such as processing of fresh products.

We expect the two additional new fresh distribution centres that will commence operations this year – Philippines (opened in May-17) and Malaysia (target to open in 2H17), to further improve Food margins.

We also expect the Group to benefit from its plan to increase its ownership in Rustan’s to 100% with the acquisition of the remaining 34% interest from its joint venture partner.

b) Capitalizing on convenience via Ready-to-Eat products and enhanced service offerings in Convenience Stores

Ready-to-Eat (RTE) food offerings continue to gained traction. Sales of RTE products grew over 10% YoY in FY16, double the rate of overall growth in Convenience Store. It has also revamped store format to incorporate a small dining in or seating area.

To draw higher footfall, it has also introduced enhanced service offers, such as establishing pick-up points and e-lockers services to complement the booming e-commerce industry, as well as cash withdrawal services, bill payment facilities, courier services, and prepaid card top-ups services over the counter.

c) Higher penetration of Corporate Brand in both Food and Health& Beauty segments

Corporate Brand (a.k.a. private labels) not only provide customers alternatives, but also enhance business profitability. The Group has over 10,000 SKUs (stock keeping units) under its Corporate Brands across Food and Health and Beauty segments. However, the penetration rate lags at mid-single digit percentage for Dairy Farm, as compared to mainstream retailers’ 25% to 50%.

This also implies that there is more scope for growth and margin expansion. In particular, its Health and Beauty division in New Markets. In 2016, over 900 new products were launched. More than 450 of these Corporate Brand products were introduced into the developing markets of Vietnam, Cambodia, Indonesia and the Philippines, which recording an impressive 117% sales growth in 2016.

Figure 10: More SKUs and new Corporate brands launched under its grocery segment

d) Strengthening and streamlining supply chain and boosting stock management capability

Establishing advanced infrastructure across the region. These centralized distribution centres could:

Efficient inventory management via technology. Its Group-wide newly implemented SAP merchandising system will reduce handling costs, strengthen key processes in the supply chain and enhance business analytics.

Shortening supply chain via direct sourcing. Leveraging on each other’s operating scale and sharing of know-how, would propel greater synergies and collaboration across the Group as well as with partners.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Lin Sin has been an investment analyst in Phillip Securities Research since June 2014, where she started as an economist, focusing on China and ASEAN macroeconomics. Currently, she covers primarily the Consumers and Healthcare sectors in Singapore equities market.

She graduated with a Bachelor of Science in Mathematics and Economics from NTU.