Company Background

Clearbridge Health (CBH) began in 2010 with a focus on the medical technology industry. It made its first investment in Biolidics in 2011, listed on the Catalist in December 2018. It then co-founded Sam Lab in 2011. In 2017, CBH acquired Clearbridge Medical Group that owned two medical clinics. CBH listed on December 2017 at S$0.28 a share. 2018 was a watershed year as CBH expanded into high growth markets of Indonesia, by acquiring a renal dialysis operator, and the Philippines, by acquiring a large medical facility. There is a further proposal to acquire 12 clinical diagnostic laboratories in Indonesia.

With only two clinics during listing, CBH has expanded into a well-diversified portfolio of asset-light healthcare businesses. The focus is on healthcare segments with the fastest growth and to create an eco-system of businesses that can support each other and serve the complete lifecycle needs of a patient. We can essentially split CBH’s businesses into three key segments:

Investment Thesis

Penetrating high-growth healthcare markets in Indonesia and the Philippines. CBH has entered the fast-growing healthcare markets in Indonesia and the Philippines through two acquisitions. Both countries rank among the lowest in Asia in terms of the number of hospital beds and health professionals per capita. Healthcare spending in both countries has been growing at around 9 – 10% p.a.

Creating a recurrent revenue stream in healthcare. A key feature of its new Indonesian business is recurring revenue. Renal dialysis is a lifetime treatment, and CBH expanded from 15 hospitals at acquisition to 21 currently and another 13 under renovation.

Targeting and revitalising profitable segments. CBH acquires asset-light, fast-growing healthcare segments. After the acquisition, CBH grows the businesses through expansion in capacity, network and capabilities.

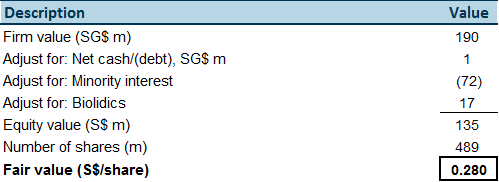

Initiate coverage with a BUY and TP of S$0.28. Initiate with a BUY recommendation and target price of S$0.28. We used DCF valuation to capture the full benefit of CBH impressive growth over the next five years.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity.

HISTORY

Clearbridge Health (CBH) began in 2010 with a focus on the medical technology industry. It made its first investment in Biolidics in 2011, listed on the Catalist in December 2018. It then co-founded Sam Lab in 2011. In 2017, CBH acquired Clearbridge Medical Group that owned two medical clinics. CBH listed on December 2017 at S$0.28 a share. 2018 was a watershed year as CBH expanded into high growth markets of Indonesia, by acquiring a renal dialysis operator, and the Philippines, by acquiring a large medical facility. There is a further proposal to acquire 12 clinical diagnostic laboratories in Indonesia.

With only two clinics during listing, CBH has expanded into a well-diversified portfolio of asset-light healthcare businesses. The focus is on healthcare segments with the fastest growth and creates an ecosystem of businesses that can support each other and serve the complete lifecycle needs of a patient. We can essentially split its business into three key segments:

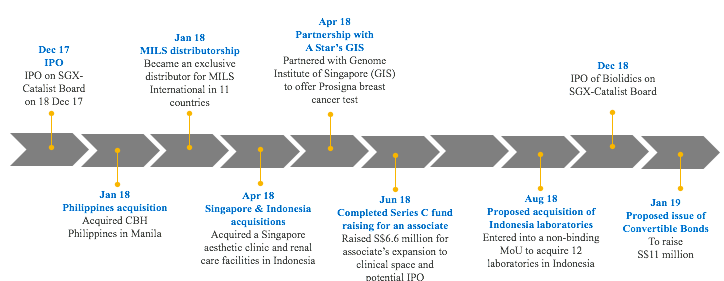

Figure 1: CBH key milestones

Source: CBH

Figure 2: Details of all acquisitions

|

Company |

Country |

Stake |

Acquisition Date |

Price (S$mn) |

Consideration |

|

Medic Laser & Surgical Pte. Ltd |

Singapore |

85% |

Jan18 |

5.5 |

Cash and shares |

|

Clearbridge Medical Philippines |

Philippines |

65% |

Jan18 |

1.9 |

Cash |

|

Tirta Medika Jaya |

Indonesia |

55% |

Apr18 |

5.5 |

Cash |

|

Indo Genesis Medika |

Indonesia |

75% |

Aug18 (Proposed) |

3.8 |

Cash |

Source: CBH, PSR

INDONESIA

CBH entered Indonesia through the acquisition of Tirta Medika Jaya (TMJ) in April 2018. The attractiveness of TMJ includes the recurrent nature of its revenue, high growth and low capex intensity.

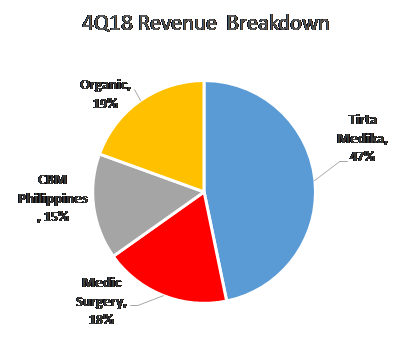

Figure 3: Tirta Medika and Medic Laser were the major revenue contributors

Source: CBH, PSR

Tirta Medika Jaya (55% stake)

Kidney Disease in Indonesia

End-stage renal disease (ESRD) is also known as kidney failure. The most common cause of ESRD is diabetes, followed by high blood pressure and hypertension. There is currently no cure for ESRD. Treatment options are either dialysis or kidney transplant.

Once the kidneys fail (defined as both kidneys functioning at only 15%), the body will be unable to process toxins and waste. Consequently, the body will be filled with excess toxins, a condition called uremia. Dialysis is an artificial process for removing waste and excess water from the blood.

According to the Indonesia Nephrology Association (PERNEFRI), 25mn Indonesians have developed chronic kidney disease, with 200,000 suffering from ESRD. Hemodialysis treatment ranks the second-largest claim covered by the Healthcare and Social Security Agency (BPJS), having already cost 7% of the agency’s total spending, or Rp2.68tr (US$195mn).

There are currently two methods of dialysis.

https://www.thejakartapost.com/life/2017/09/27/living-with-kidney-failure.html

Figure 4: Revamped dialysis facility

Source: CBH

Figure 5: Dialysis treatment equipment

Source: CBH

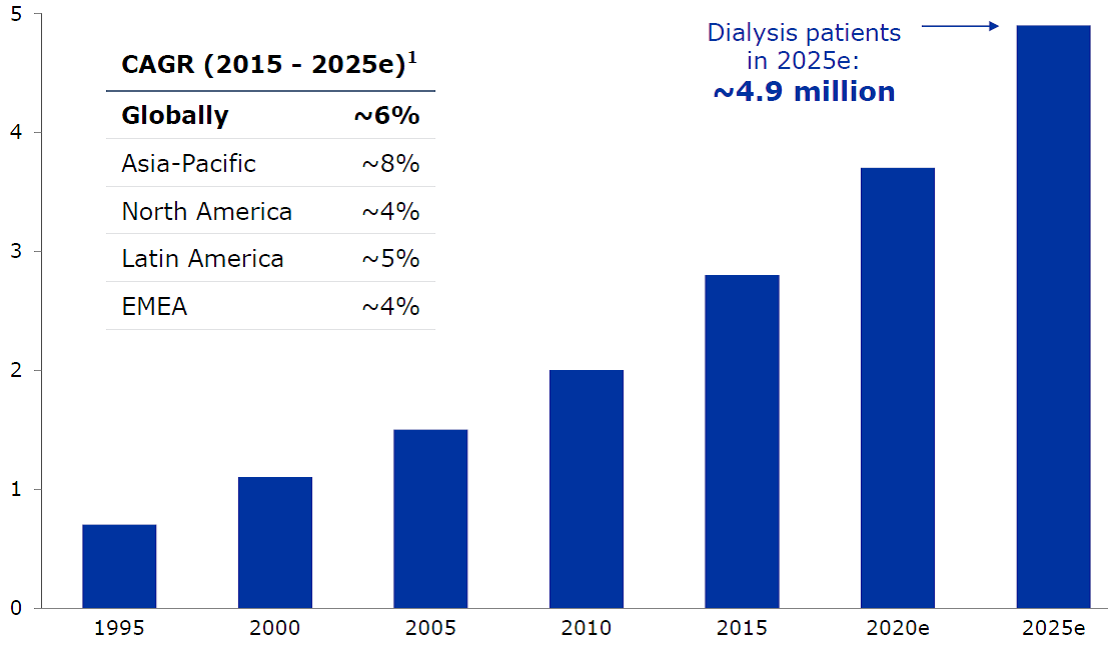

Figure 6 : Dialysis patients is rising globally at 6% p.a.

Source: Fresenius Feb2019

In August 2018, CBH entered into a non-binding memorandum of understanding to acquire 12 clinical laboratories operated by Indo Genesis Medika (IGM) in Indonesia.

Indo Genesis Medika (75% stake)

* referral hospitals mean that these grade A hospitals are referred patients from other lower grade hospitals as grade A hospitals generally have better equipment and medical resources.

Clinical laboratory testing is the use of specimens to ascertain the health of the patient. It can be generally categorized as (i) Routine tests: Fast turnaround test on the function of organs such a kidney, liver, heart, thyroid, blood, etc. The test may be for HIV, allergy, glucose, cholesterol and various substances; (ii) Esoteric test: A more specialised and higher priced test done on the tissue or cell for cancer and other diseases, such as tissue and liquid biopsy. Or testing of biological markers in hormones, protein and genes. Hospitals may conduct routine test and more esoteric or specialised test undertaken by private labs.

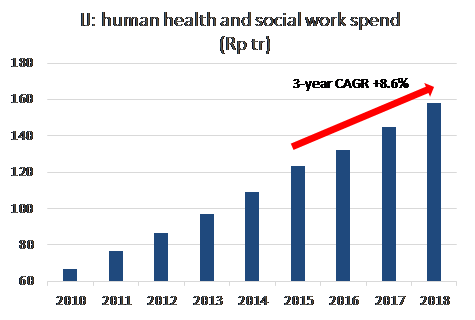

Figure 7: Healthcare spending rising almost 9% p.a. in Indonesia

Source: CEIC, PSR

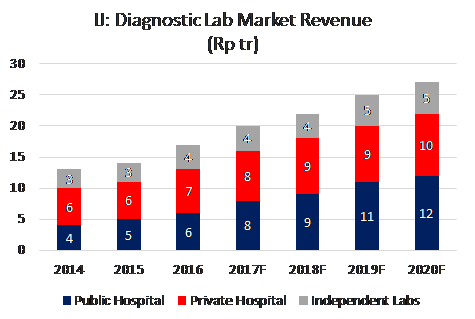

Figure 8: Diagnostic lab market in Indonesia to grow 12% CAGR (2016 to 2020e)

Source: IMS Health Analysis (2017), Prodia Widyahusada (Nov18), PSR

PHILIPPINES

CBH entered the Philippines healthcare sector in 2018 with the acquisition of Marzan Health in January 2018 (renamed Clearbridge Medical Philippines). Since taking over, CBH renovated the facility, introduced more medical services and opened three additional branches.

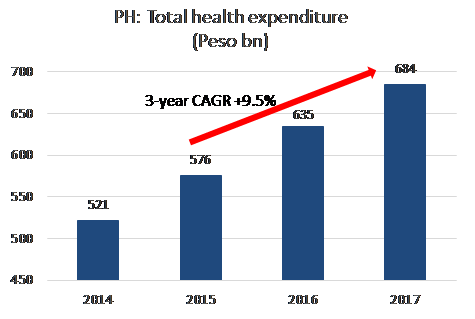

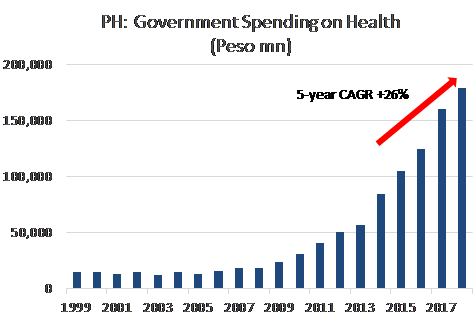

According to the Philippines statistics authority (Figure 14), total healthcare expenditure (excluding fixed capital formation) in the country grew around CAGR 9.5% p.a. over the past three years to US$13bn in 2017. A surge in government spending has been supporting growth as well. As Figure 15 suggests, the government budget for healthcare has been rising at 26% p.a. over the past five years.

Healthcare spending in the Philippines is expected to grow at a much faster pace with the introduction of universal health insurance. In February, the Universal Health Care Act was signed into law. The act is a US$4bn (P217bn) funded automatic enrollment of all citizens into the National Health Insurance Programme (NHIP) administered by PhilHealth. It is an expansion of the existing PhilHealth insurance where only 2 out of 3 Philippine citizens received coverage. Coverage will also be widened from not just hospitalization but preventive healthcare services. It will be funded by taxes on tobacco and alcohol.

Clearbridge Medical Philippines (65% stake)

Listed exposure to healthcare in the Philippines:

Figure 9: The 4-storey medical centre

Source: CBH

Figure 10: Renovated interior

Source: CBH

Figure 11: A patient waiting floor

Source: CBH

Figure 12: Facility is in Quezon City

Source: CBH

Figure 13: One branch inside a hospital in Lapulapu City, City

Source: CBH

Figure 14: Healthcare spending grew at almost 10% p.a. in the Philippines

Source: Philippine Statistics Authority (psa.gov.ph), PSR

Figure 15: Government spending will surge further with Universal Healthcare

Source: Department of Budget and Management, CEIC, PSR

SINGAPORE

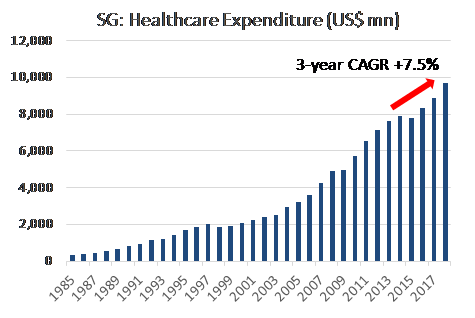

CBH has a strategy to cater to the growing needs of a consumer’s health care in Singapore with various medical touchpoints along the treatment journey. It owns a medical clinic, aesthetic and clinical laboratory in Singapore. This suite of services can cater to the general, lifestyle and chronic care lifecycle of a patient. The spending on healthcare in Singapore continues to escalate but competition will be intense especially from the public sector. For instance, government expenditure on health has more than doubled from S$3.9bn in 2010 to S$9.3bn in 2016. The government has built seven hospitals since 2010.

Demand for healthcare in Singapore will continue to expand as the nation faces the trifecta challenge in healthcare.

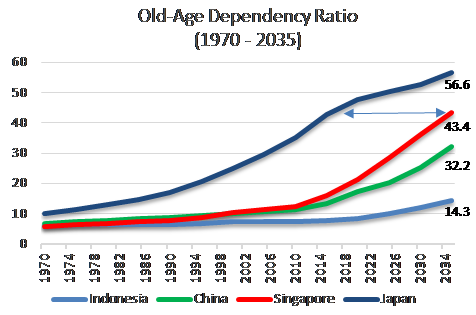

a) Ageing population (Figure 14): By 2030 and 2035, the old-age dependency ratio for Singapore will reach 36 and 43 respectively. This will be similar to Japan in 2010 and 2015. The old-age dependency ratio is the number of those aged above 65 years (defined as old age) as a share of the working age (15 to 64 years).

Figure 16: Singapore is ageing rapidly and similar to current Japan ratios by 2035

Source: UNDESA Forecast, PSR

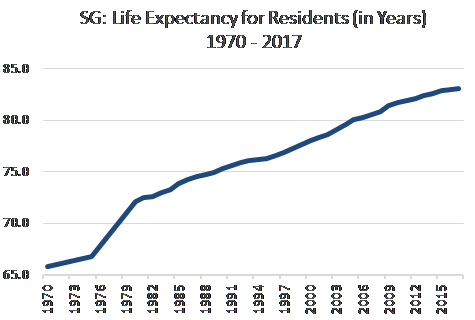

b) Longer life expectancy of the population (Figure 17): Since 1990, the life expectancy of the population has risen from 66 in 1970 to 83 in 2017. This is a rise of 17 years. However, for every ten years we live, more than one year is spent in

Figure 17: Singapore life expectancy rise 4+ years in every decade

Source: CEIC, PSR

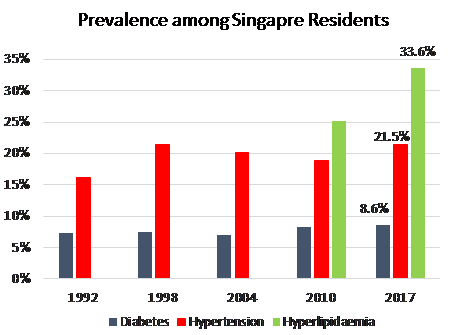

c) Less healthy lifestyles: In a recent budget speech, the Minister of Health highlighted the rising prevalence of chronic illness due to ageing and unhealthy lifestyle. From 2010 to 2017, diabetes has increased 4%, hypertension up 14% and hyperlipidaemia jumped 33% (Figure 18).

Figure 18: Rise in lifestyle illness

Source: National population health survey 2017, 1992-2010 based on National Health Survey; Survey is on residents aged 18-69 years

Sam Laboratory (100% stake) samlaboratory.com

Figure 19: New premises for Sam Lab

Source: CBH

Medic Surgery and Laser Clinic (85% stake) www.medicsurg.com

Figure 20: Clearbridge clinic in Tanjong Pagar

Source: CBH

Clearbridge Medical Group (100% stake)

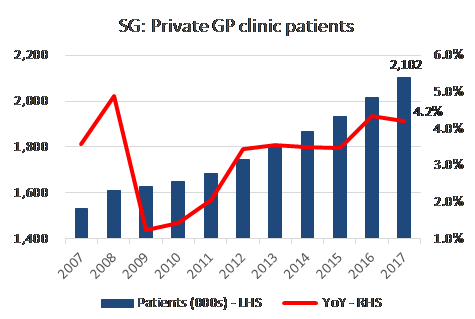

Figure 21: Still steady 4% growth in patients for private GP clinics

Source: CEIC, PSR

HONG KONG www.clearbridgemedical.com.hk

A medical clinic that started in 2017. The target patients are medical tourists from China. The key driver to growth will be the co-operation with marketing agents in late 2018 to bring medical tourists to this clinic. Some of the services offered include health screening, vaccination and medical consultation. The clinic is also collaborating with insurance companies such as Prudential and Tai Ping. There are currently plans to expand the premises of this clinic.

There are over 3mn outbound Chinese health tourists per year. The most frequently travelled destinations for medical tourism include Hong Kong, Macau and Taiwan (using the latest total China Outbound Tourism Research Institute (COTRI) figures of 145mn in 2017). The report (as per link below) highlighted that both the number and percentage of Chinese health tourists are expected to rise in 2018.

https://www.imtj.com/news/health-tourism-flows-and-out-china/

Figure 22: Hong Kong clinic

Source: CBH

MALAYSIA

CBH expanded its presence into Malaysia with the opening of a paediatric cum family clinic in Kuala Lumpur. The commencement of the clinic is dependent on a pending license from the Ministry of Health. CBH will also work with several other GP clinics in KlangVallent to provide their Hereditary Cancer Gene Test.

Figure 23: New clinic in Desa Park, KL

Source: CBH

STRATEGIC INVESTMENT

Biolidics Ltd (24.8% stake, with Jan2020 call option for SEEDS Capital 10.67% stake)

(i) Collaboration with Sysmex. Sysmex is a US$13bn market cap leader in haematology and coagulation instrumentation worldwide. It is a Japanese company. Biolidics can tap on Sysmex’s immense distribution network to sell the FX1 system as part of a complete oncology test kit for clinical labs globally.

(ii) Lab-developed tests in China. In China, Biolidics is working with labs in Hunan and Hangzhou to gain such validation and thereafter to offer cancer diagnostic services (with these lab-developed tests) to patients. Professor Xie Tian is a shareholder and winner of the Wu Jieping Medical Innovation Award. He is considered a key opinion leader in the field of oncology in China.

(iii) China FDA Class 3 registration. The FX1 system currently has a Class 1 registration. A Class 3 registration will allow the product to be used nationwide.

Figure 24: ClearCell®FX1 System machine

Source: CBH

Figure 25: CTChip® FR1 biochip

Source: CBH

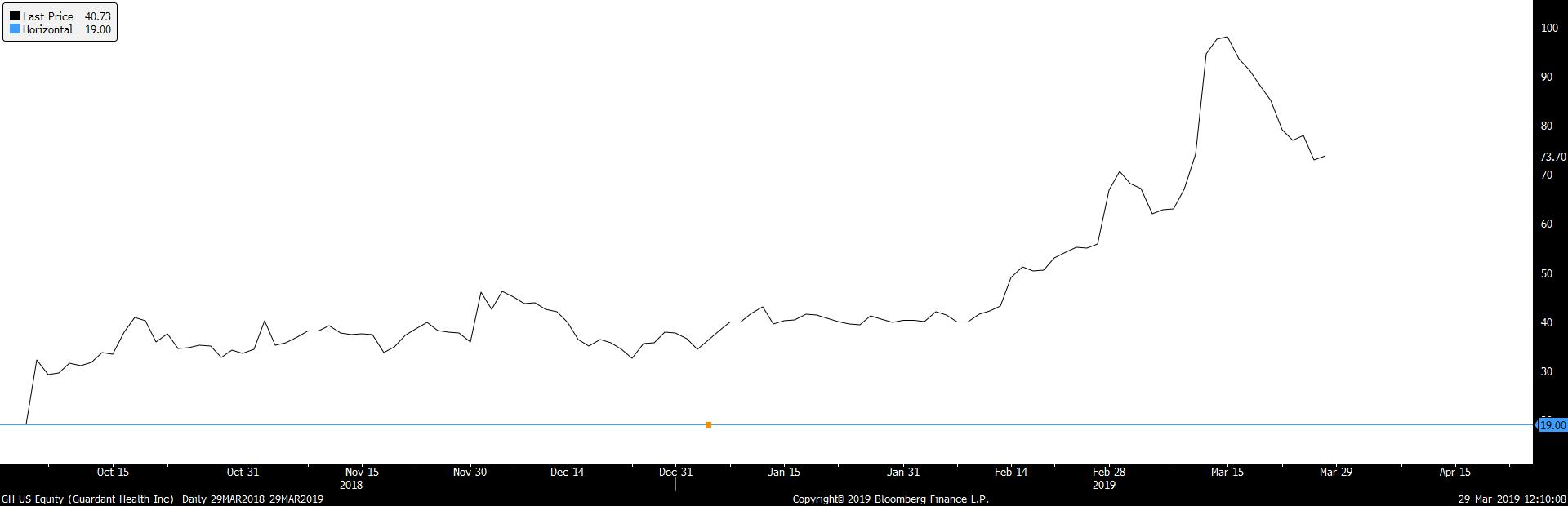

A leader in liquid biopsy is Nasdaq listed Guardant Health (GH). However, the model is different because blood samples need to be sent to Guardant labs in the U.S. to be tested. However, unlike GH, Biolidics’ ClearCell® FX1 System is a fully automated and portable CE-IVD medical device. The device uses a label-free approach to enrich circulating tumour cells (“CTCs”), which helps to maintain the CTCs in their original state and preserve their viability for further use in diagnostic tests and downstream applications.

The portability of ClearCell® FX1 System enables swift deployment and commercial scalability as compared to lab-based systems such as GH.

In addition, leveraging on its ClearCell® FX1 System, Biolidics is developing a range of laboratory developed tests for the cancer diagnostics market in China and Japan. Biolidics will be ideally positioned to increase the sales potential of its ClearCell® FX1 System and CTChip® FR1 biochips once these blood-based lab-developed tests are approved clinically.

Figure 26: Guardant share price has surged from $19 at IPO to $73.

Source: Bloomberg, PSR

OUTLOOK – Macro Tailwind + Good execution

We believe the two primary growth drivers for CBH is the healthy underlying demand for healthcare services in the three key countries that it is operating in – Indonesia, Philippines, Singapore, and it’s aggressive and strong execution to grow the various businesses acquired.

A) MULTI-YEAR MACRO TAILWIND

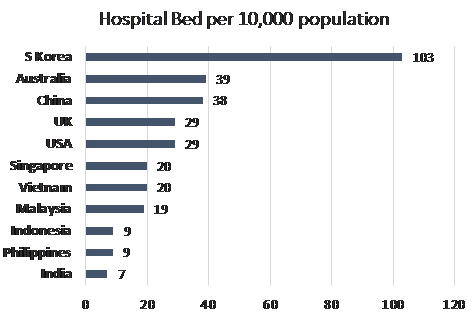

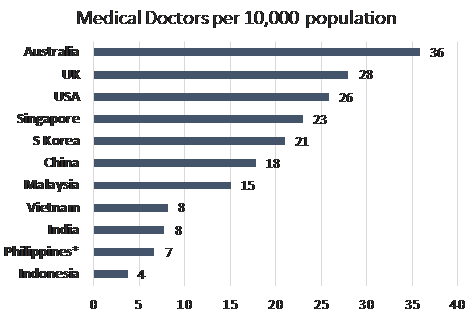

There is low penetration of healthcare in key markets – Indonesia and the Philippines. As Figure 27 and 28 suggest, the penetration of facilities or hospital beds and medical professionals are some of the lowest in the region.

Figure 27: Low penetration of medical facilities

Source: CEIC, Media, PSR, Siloam Hospitals

Figure 28: Lack of medical professionals

Source: CEIC, Media, PSR, Siloam Hospitals

* Philippines based on 70,000 active physicians out of 130,000 registered

In Singapore, the demand for healthcare is ever growing. Over the past three years, healthcare expenditure has been rising at almost 8% CAGR. As highlighted, there are three major drivers to the rise of healthcare demand in Singapore. Firstly, Singapore population is ageing fast (Figure 16). By 2035, our number of old age to working age will be similar to current levels in Japan. Secondly, Singaporean life expectancy is rising (Figure 17), and for every ten years extra we live, more than one year is spent in illness. Thirdly, less healthy lifestyles have seen the rise of chronic diseases such as diabetes, hypertension and hyperlipidaemia (Figure 18).

Figure 29: The rise and rise of healthcare expenditure in Singapore

Source: CEIC, PSR

B) STRONG EXECUTION POST ACQUISITION

Secondly, after taking over the new acquisition, CBH has undertaken initiatives to expand the original business at a much faster pace.

(i) TMJ: When acquired, it only operated renal dialysis in 15 hospitals. After taking control in April 2018, CBH has secured contracts to expand the network to 34 hospitals. All this was completed within 12 months.

(ii) Philippines: After acquiring the four-storey medical centre, CBH undertook a renovation of the facility, introduced new services and expanded their footprint.

(iii) Hong Kong: Refocus strategy to target medical tourist from China.

(iv) Indo Genesis Medika (Proposed): Introduce more innovative clinical lab tests into Indonesia, attract more hospitals to tap on their facilities and support from Singapore on the more complex tests.

With the S$11mn raised from convertible bonds, we expect more acquisition to be undertaken by CBH. Around 70% of the proceeds will be earmarked for expansion of the business plus merger and acquisitions. The convertible bonds bear an interest of 7% p.a. and repayable at 120% of principal by January 2022. Up to 39.28mn new shares can be issued upon full conversion. Worth noting that the accounting treatment of the convertible bond is to recognize the value of the embedded option at fair value in the income statement.

INVESTMENT THESIS

Penetrating high-growth healthcare markets in Indonesia and the Philippines. CBH has entered the fast-growing healthcare markets in Indonesia and the Philippines through two acquisitions. Both countries rank among the lowest in Asia in the number of hospital beds and health professionals per capita. Healthcare spending in both countries has been growing at around 9 – 10% p.a.

Creating a recurrent revenue stream in healthcare. A key feature of its new Indonesian business is recurring revenue. Renal dialysis is a lifetime treatment, and CBH is expanding from 15 hospitals at the time of its acquisition to 21 currently and another 13 under renovation.

Targeting and revitalise profitable segments. CBH acquires asset-light, fast-growing healthcare segments. After the acquisitions, it will generally streamline operations, enhance costs efficiencies and grow revenue to maximize the business potential of the healthcare segments. After which, CBH will expand the businesses through expansion in capacity, network and capabilities.

VALUATION

Initiate coverage with a BUY and TP of S$0.28. Initiate with a BUY recommendation and target price of S$0.28. We used DCF valuation to capture the full benefit of CBH impressive growth over the next five years. Our assumptions are as follows:

A. Financial assumptions

Cost of equity = 10%; WACC = 8%; terminal growth rate = 3%

B. Operating assumptions

Indonesia

Philippines: Introduction of new services in the medical centre will be the growth driver. New services include more pharmacy sales, health screening for overseas foreign workers, renal care and new aesthetics centres.

Hong Kong: Medical tourism will be the key driver. Limitations are space and medical doctors.

Singapore

(i) Sam Lab: Introduce more high value-added esoteric tests, especially focused on oncology.

(ii) Medic Laser: With only one doctor and several therapists, growth will be driven by mid-to-high single digit volume growth.

(iii)GP clinic: Only one doctor and growth is driven by volume.

(iv) Product distribution: Distribution into the region (Singapore, Hong Kong, Malaysia, Indonesia) of esoteric tests for principals such as Biolidics ClearCell® FX1 System, CELLSEARCH® Circulating Tumor Cell Test, Prosigna® Breast Cancer Prognostic Signature Assay and MILS International diagnostics test.

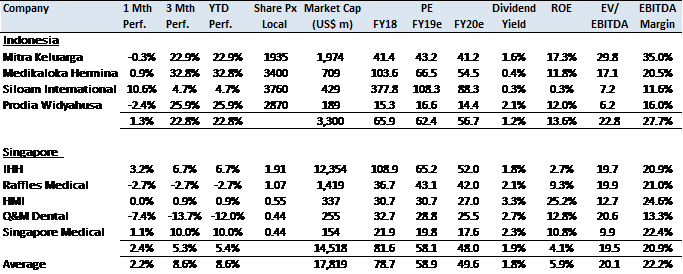

Figure 30: Healthcare comparables trade at 20x EV/EBITDA but with a slower growth profile

Source: Bloomberg, PSR

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: