The positive

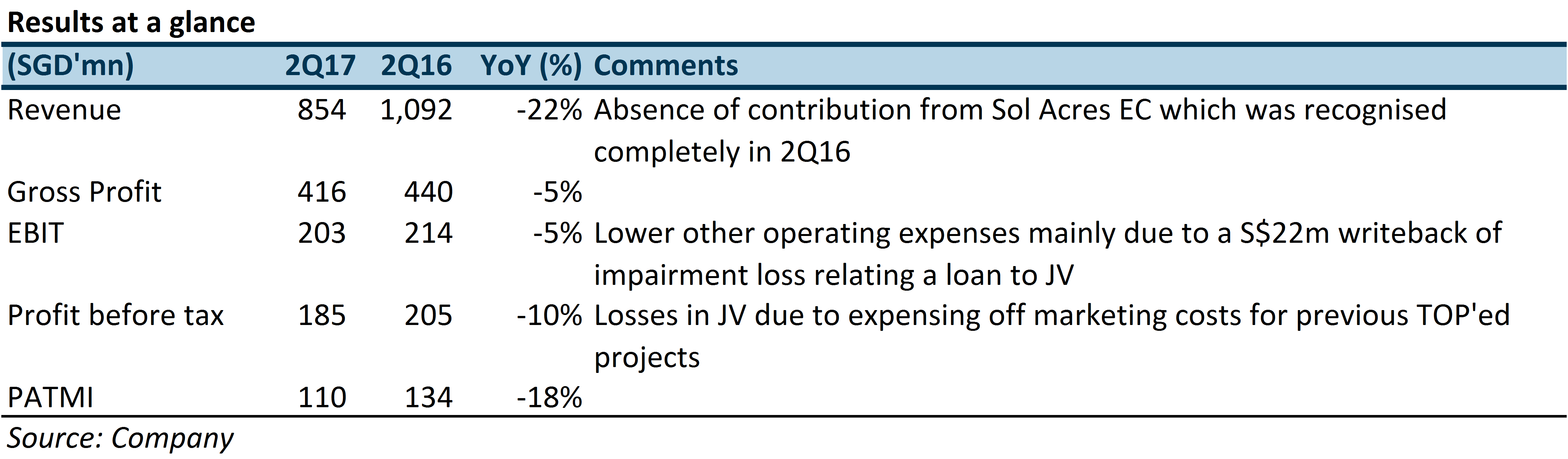

+ Buoyant performance in Singapore Property segment amid improvement in the sector: Sales value for Singapore Property segment close to tripled in 1H17 to S$1.1bn driven by higher sales volume (1H17: 691 units vs 1H16: 324 units) of completed projects, in particular, Gramercy Park and The Venue Residences. Excluding the contribution from Lush Acres EC which was recognized entirely in 2Q16, revenue and PATMI in 2Q17 would have grown 15.7% and 43.4% YoY to S$1,263mn and S$192.2mn respectively.

+ Growth across the board for Hotel Operations: Revenue and PBT for Hotel Operations via the Group’s 65%-owned subsidiary, Millennium & Copthorne Hotels PLC (M&C), grew 4.3% and 1.6% YoY to GBP46mn and GBP42mn respectively. While the bulk of PATMI gains was mainly attributed to one off items amounting to GBP12mn, hotel performance also came in stronger driven by higher RevPAR growth across three of M&C’s key markets (US, London and Australia).

The negative

– Ongoing sluggishness in China: Out of three launched projects in China, the Group has moved two out of 126 units in Eling Residences (8% sold) for a sales value of RMB12.8mn in 2Q17. The Group also sold another 65 out of 1,804 units in Hong Leong City Center (73% sold) during the quarter. This was primarily due to effect of a slew of restrictive property cooling measures implemented across China.

Outlook

Rapid absorption of units in Venue Residences and Commonwealth Towers have significantly diminished ABSD woes: The Group’s two development projects, Commonwealth Towers and The Venue Residences which we previously perceived to have the highest probability of suffering from an ABSD clawback have registered stronger take up rates in 1H17. In 2Q17, the Group has successfully offloaded the remaining 32 unsold units (12% of total units) in The Venue Residences. It has also sold another 184 out of 845 units in Commonwealth Towers during the quarter, meaning that the development is 92% sold. The group has another eight months till April 2018 to sell the remaining units in Commonwealth Towers before the ABSD clawback deadline.

Strong recovery in the high-end segment sets the stage for New Futura launch: The Group’s 174-unit condo project, Gramercy Park, located in the CCR market segment registered keen interest. ASP gained 2.9% QoQ to S$2,880 following the sale of 25 units after the soft launch of Phase two of the development. Among the sales, a 5-bedroom penthouse unit was sold for S$17 million, translating to a transacted ASP of S$3,072 PSF. We view that the strong demand for the recently launched Martin Modern and Gramercy Park as an advance indication to the demand of a nearby upcoming new 124-unit freehold condominium project, New Futura. Additionally, with the selling out of most nearby developments, Cairnhill Nine and OUE Twin Peaks, we expect the thinning supply of high-end projects to benefit both ASPs and take up rates when launched.

Near term plan is to replenish land bank for development but still has three unlaunched projects for sale: Including New Futura, CDL has two other development projects that are yet to be launched, the land site at Tampines and South Beach Residences. While we view that the Group is committed to replenishing its landbank for future development, the Group has lesser urgency since they still have three unlaunched development projects and 428 unsold units (attributable to CDL) in its inventory. Out of the seven developers, we have coverage on, CDL has the most number of unlaunched projects and existing inventory of unsold units in Singapore.

S$60mn AEI at Republic Plaza expected to generate a 10% ROI: CDL intends to commence AEI works at Republic Plaza in 1Q18 for 12 to 15 months, which is expected to generate an ROI of 10%. The AEI works will involve the creation of 5,000 sqft new retail GFA (21,000 sqft existing) via the conversion of some existing car park lots, and rejuvenation works in the development. CDL will also relocate into Republic Plaza by taking up 42,000 sqft. CDL will free up 60,000 sqft spanning across nine floors at City House, where ~50% of the space has already been pre-committed.

Outlook for China Property development segment still bright in the longer term: While we opine that China property development in China is likely to remain weak in the short term. This will be cushioned by the Group’s relatively limited exposure to the country (value of unsold units amounted to ~4% of our RNAV estimates). We are of the view that some of the Group’s development is likely to benefit in the longer term. For instance, the Group’s 48%-sold Hongqiao Royal Lake villa project in Shanghai will enjoy some scarcity value as Villa development is no longer permitted in China in a move to intensify land use.

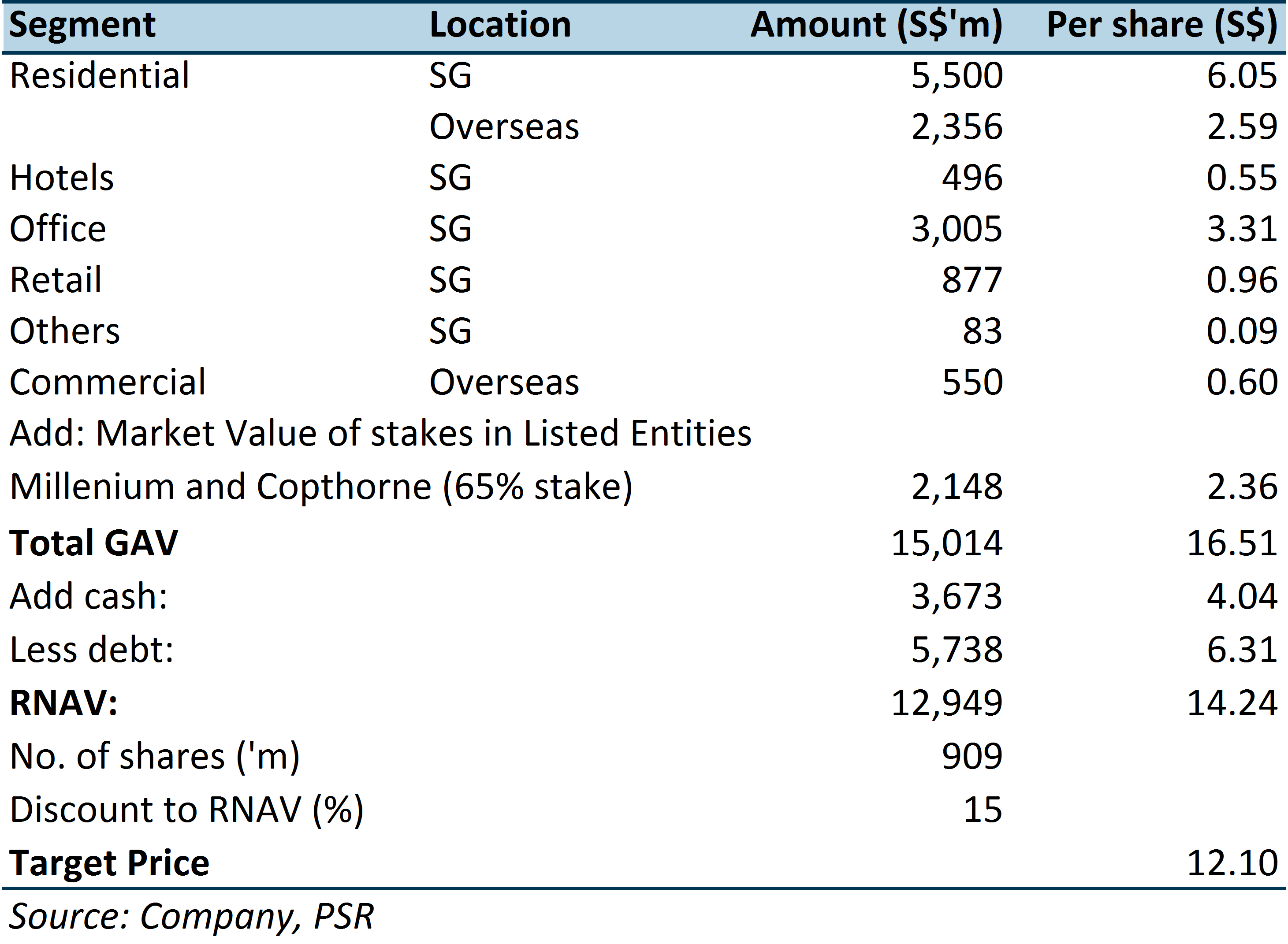

Maintained a rating of “Accumulate” with higher TP of S$12.10 based on our revised FY17 RNAV estimates

We continue to favour CDL for its large Singapore development exposure of unlaunched and available for sale inventory. While there are near term challenges in the China development segment, the longer-term outlook remains bright. We have revised our RNAV per share estimates upwards by 9.3% to S$12.10 particularly, to take into account of higher ASPs in both existing and new development projects. We continue to adopt a 15% discount to RNAV estimates.

Valuations

Figure 1: RNAV Table

Figure 2: Historical P/B Table

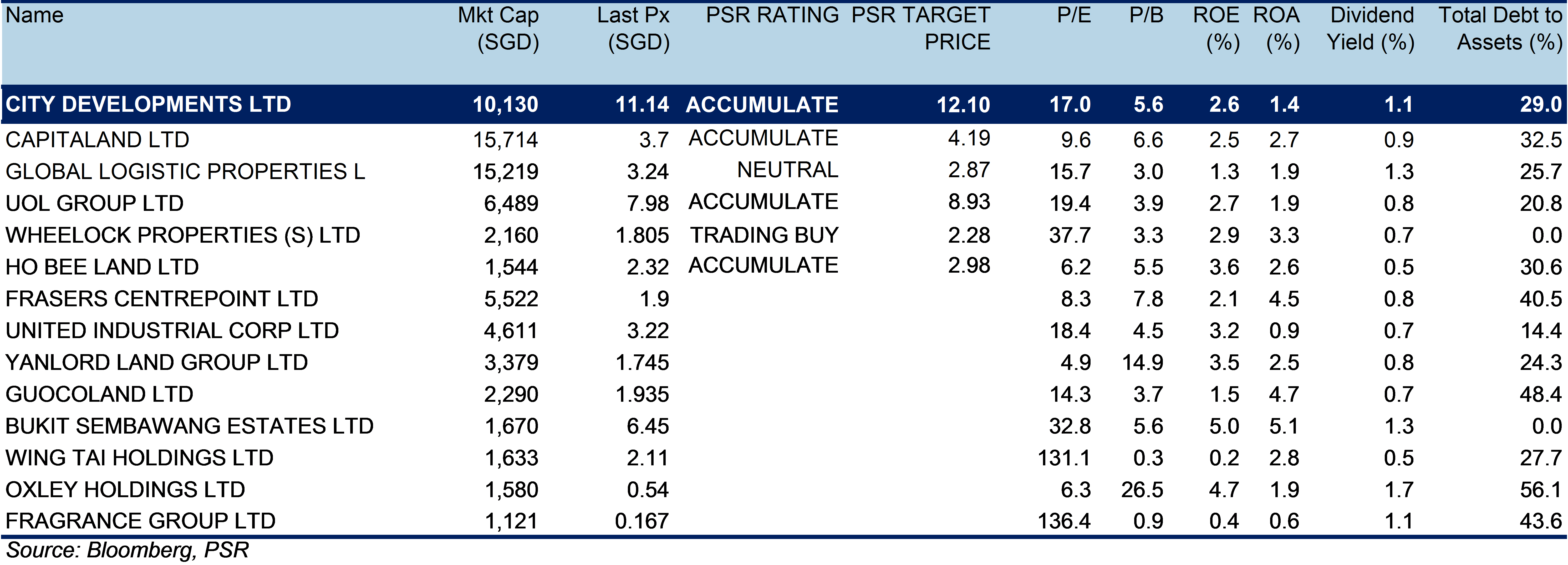

Figure 3: Peer Comparison Table

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: