The positive

+ Strong momentum in Singapore Property segment amid improvement in sentiment. Continuing the sales momentum from 1H17, sales value for Singapore Property segment close to tripled YTD17 to S$1.76bn. Number of units sold YTD was double YoY, implying an increased proportion of higher-end units sold. Going forward, 3 projects are due for launches in 1H18 at New Futura (124-units at Leonie Hill), Tampines Ave 10 (861 units), and South Beach Residences (190 units).

+ Broad-based recovery for Hotel Operations as global sentiment and tourism improves. On a like-for-like basis, Millennium & Copthorne (M&C)’s global RevPAR improved 1.4%, led by strong growth in Australasia, London and New York. These 3 markets make up close to 40% of M&C FY16 revenue. Including the impact of acquisitions, closures and refurbishments, global RevPar improved 4% in constant currency, an improvement in the -2.3% drop for FY16.

+ Strategic partnership with Vanke in China likely to boost asset sales for partnered assets: CDL’s strategic partnership with China Vanke sets the stage for future collaborations which would enable CDL to tap on the local expertise and business networks of Vanke. The partnership which was achieved through the partial divestment of two properties in Chongqing, namely 70% of Chongqing Huang Huayuan and 50% of Eling Residences allows for 1) partial monetization (c.RMB1bn) of assets for capital recycling 2) access to Vanke’s extensive local networks and development expertise which we believe could lead to increased future saleability for the two projects.

The negatives

– Slower residential sales in UK, China. Uncertainties over Brexit and government cooling measures in UK and China led to slower sales of residential projects in these countries. The Group soft-launched 240-unit Teddington Riverside in late October, but opined that transactions could take time to gain traction as local buyers typically prefer to buy finished products.

Sales at the other major China project, HLCCC in Suzhou, continued at roughly the same slow pace as the previous quarter, with 25 (Phase 1) and 17 units (Phase 2) sold in the quarter. (2Q17: 56units and 9 units respectively)

– Drop in office occupancy to 92.5% (from 95.9% at FY16), but likely to improve going in to FY18. Tapering new supply and improved corporate demand as noticed across most office S-REITs leads us to believe the blip in occupancy will likely improve going into FY18.

Outlook

Main catalysts to come from successful launches of 4 residential projects in Singapore, mostly in 1H18: CDL remains one of the most well-stocked developer under our coverage to benefit from the upcycle in the Singapore residential and commercial property market. Healthy demand and a recent pickup in interest in high end developments such as newly launched Martin Modern and CDL’s Gramercy Park suggests healthy saleability for New Futura with new limited new supply in Core Central Region. We are similarly confident of take-up rates and ASPs for South Beach and Tampines Ave 10 site given 1) exclusivity of South Beach site with unblocked panoramic views of Marina Bay and the city 2) smaller units at Tampines site with affordable quantum – we have seen similar suburban projects sell well at psfs higher than the forecasted c.S$1100psf for Tampines, such as in the S$1300+ range in Tanah Merah precinct. We think higher execution risks exist for the Amber Park site. Healthy take-up rates and ASPs for these 4 launches next year and forward could be catalysts for share price and upward revision of target price.

Office outlook looks set to further recover in 2018: Grade A office rents appear to have bottomed with the first increase in 3Q17 after 10 quarters of decline. We believe the recovery should continue will improved corporate demand as evident across most office S-REITs and tapering new supply. This will likely mitigate the magnitude of negative reversions expected for the 27% leases (by NLA) expiring in 2018 for CDL’s office portfolio.

Hotel refurbishment programme ongoing which is likely to impact M&C earnings in the short term. Management expects M&C to progress with its capital expenditure across a number of hotels for M&C, which will likely further impact M&C’s earnings.

Outlook for China Property development segment still bright in the longer term: While we opine that China property development in China is likely to remain weak in the short term. This will be cushioned by the Group’s relatively limited exposure to the country (value of unsold units amounted to ~4% of our RNAV estimates). We are of the view that some of the Group’s development is likely to benefit in the longer term. For instance, the Group’s 58%-sold Hongqiao Royal Lake villa project in Shanghai will enjoy some scarcity value as Villa development is no longer permitted in China in a move to intensify land use.

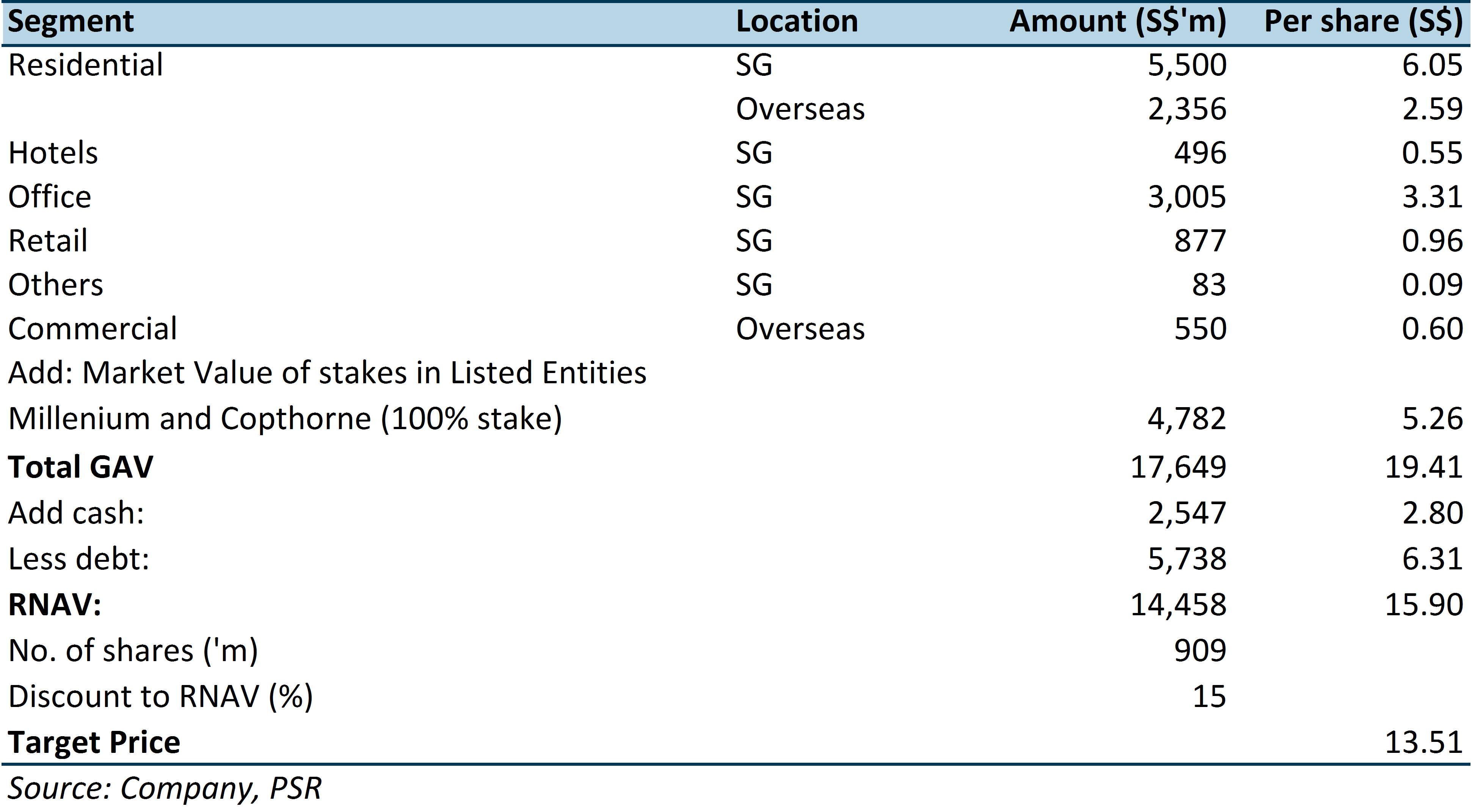

Maintained Accumulate with unchanged TP S$12.10 (successful accretive acquisition of M&C could increase our TP to S$13.50 depending on offer price)

Post-acquisition of M&C, depending on final offer price, TP could potentially increase to S$13.50. An offer, if any, would likely be at a substantial premium to the initial offer price given that current trading price is already 10% higher than the initial offer. For now, pending closure of the deal, we maintain ACCUMULATE with a TP of S$12.10. We continue to favour CDL for its large Singapore development exposure of unlaunched and available for sale inventory to capture the potential upswing in SG property prices. Post consolidation, SG residential makes up c.31% of adjusted GAV. Including properties in other sectors, SG exposure stands at c.56% of adjusted GAV.

Figure 1: Revised RNAV Table (assuming acquisition at current offer price)

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Dehong covers primarily the REITs and property developer sector. He has close to 7 years experience in equities related dealing and research roles.

He graduated with a Masters of Science in Applied Finance from SMU and Bachelors of Accountancy from NTU.